/Broadridge%20Financial%20Solutions%2C%20Inc_%20logo%20on%20laptop-by%20monticello%20via%20Shutterstock.jpg)

Broadridge Financial Solutions, Inc. (BR) is a New York-based financial technology and corporate services company that provides mission-critical infrastructure, communications, and processing services to the global financial services industry. With a market cap of $20.8 billion, Broadridge operates through Investor Communication Solutions, Global Technology and Operations, and other segments.

Broadridge shares have observed a 26.3% downtick over the past 52 weeks and 21% drop on a YTD basis. In contrast, the S&P 500 Index ($SPX) has gained 11.7% over the past year and has posted marginal returns in 2025.

Narrowing the focus, Broadridge has also underperformed the sector-focused State Street Technology Select Sector SPDR Fund’s (XLK) 15.8% surge over the past 52 weeks and 2.6% dip on a YTD basis.

On Feb. 3, Broadridge released its Q2 2026 earnings, triggering a sharp 6.3% selloff before shares clawed back 2.2% the next session. Revenue climbed 8% year over year to $1.71 billion, powered by a 9% gain in high-quality recurring revenue, while adjusted EPS edged up 2% to $1.59 and topped expectations. Profitability was held back by a 27% slump in event-driven revenue, largely tied to softer mutual-fund proxy activity, nudging operating income slightly lower. Still, management struck an upbeat tone, lifting full-year adjusted EPS growth guidance to 9–12% and reaffirming other targets, underscoring confidence in durable platform demand and recurring-revenue momentum.

For fiscal 2026, ending in June, analysts expect BR to deliver an adjusted EPS of $9.51, up 11.2% year-over-year. Further, the company has a robust earnings surprise history. It has surpassed the Street’s bottom-line projections in each of the past four quarters.

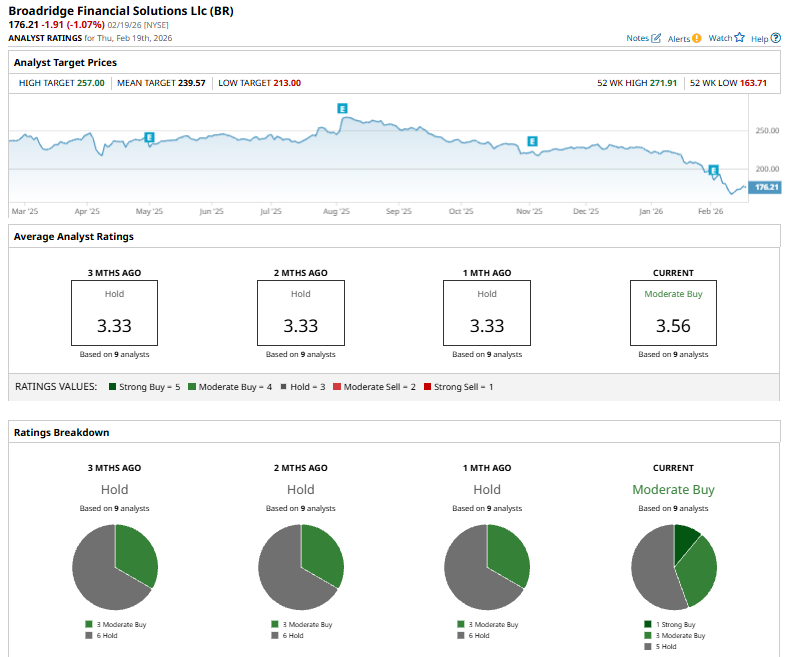

Among the nine analysts covering the BR stock, the consensus rating is a “Moderate Buy.” That’s based on one “Strong Buy,” three “Moderate Buys,” and five “Holds.”

The current consensus is bullish than a month ago, when the stock had an overall “Hold” rating.

On Feb. 10, DA Davidson reiterated its “Buy” rating and $228 price target on Broadridge Financial after the company agreed to acquire CQG’s core trading technology business, a futures and options execution and connectivity platform. CEO Tim Gokey said the deal will cost about $170 million and add roughly $55–58 million in annual revenue. The analyst views the acquisition as strategically aligned with Broadridge’s approach of buying complementary capital-markets technology assets, while noting the firm maintains moderate leverage.

Broadridge’s mean price target of $239.57 represents a 36% premium to current price levels. Meanwhile, the street-high target of $257 suggests a robust 45.8% upside potential.