China last year narrowly beat its economic growth target of 5 percent, one of its lowest benchmarks in decades. Looking ahead, analysts expect the economy to face stiff headwinds in the Year of the Dragon.

Against the backdrop of a crisis-stricken property market, subdued export earnings and crackdowns on private industry, international investors are pulling out of Chinese stocks at record rates.

With business sentiment faltering, economists broadly agree that Beijing needs to roll out measures to stimulate more domestic consumption.

While some analysts are calling for radical measures to jolt China’s economy, expectations are subdued owing to Beijing’s aversion to broad-based social spending.

Others see grounds for optimism beyond the current strains.

China is experiencing its longest deflationary run since the 2008 Global Financial Crisis. Consumer prices fell in January for a fourth straight month and declines look likely to extend into 2024.

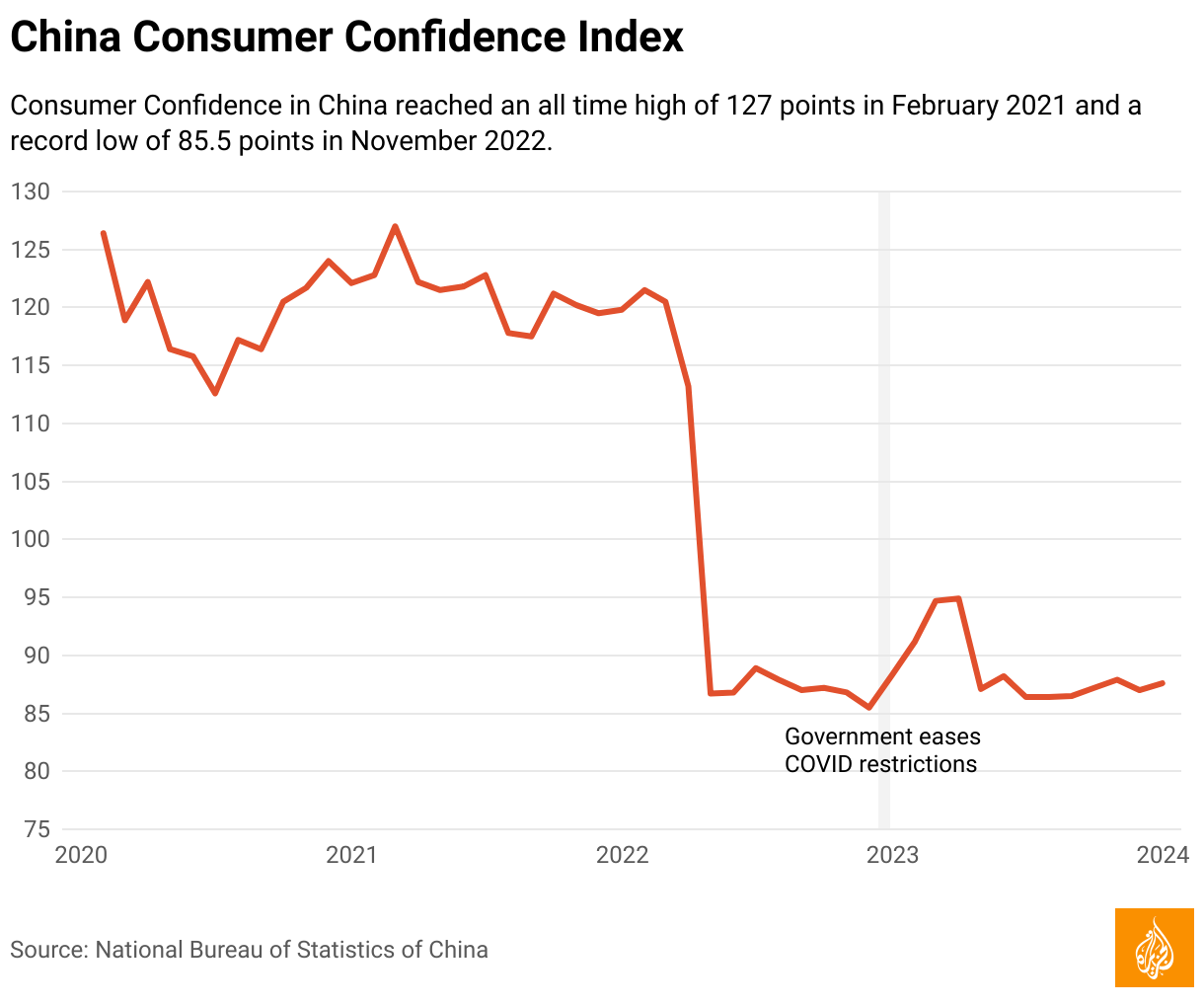

“China didn’t see the boost most people expected after COVID restrictions were removed in late 2022,” Kevin P Gallagher, the director of the Boston University Global Development Policy Centre, told Al Jazeera.

“Authorities are now keenly aware of the threat of falling prices.”

Falling prices risk turning into a self-reinforcing cycle if households and businesses postpone purchases in the hope that goods will keep getting cheaper.

Deflation also squeezes debtors as the real cost of borrowed money rises.

In China, where the debt-to-GDP (gross domestic product) ratio, including local government liabilities, reached 110 percent in 2022, that poses a growing headache for policymakers.

In recent months, authorities have ramped up support measures to try and stem falling prices – mortgage rates on home purchases have been lowered and banks have been allowed to hold smaller cash reserves to spur increased lending.

Much of China’s deflationary woes can be traced back to its beleaguered real-estate sector, which accounts for 20-30 percent of GDP.

After the 2008 Global Financial Crisis, local governments encouraged a debt-fuelled construction boom to boost growth. But after decades of rapid urbanisation, housing supply has run ahead of demand.

Amid several high-profile developer defaults, including the failure of Evergrande Group, new home sales fell by 10-15 percent in China last year, according to the Fitch Ratings agency.

In turn, Chinese households have become cautious about spending money, especially on property, while a weak social safety net encourages families to save for emergencies.

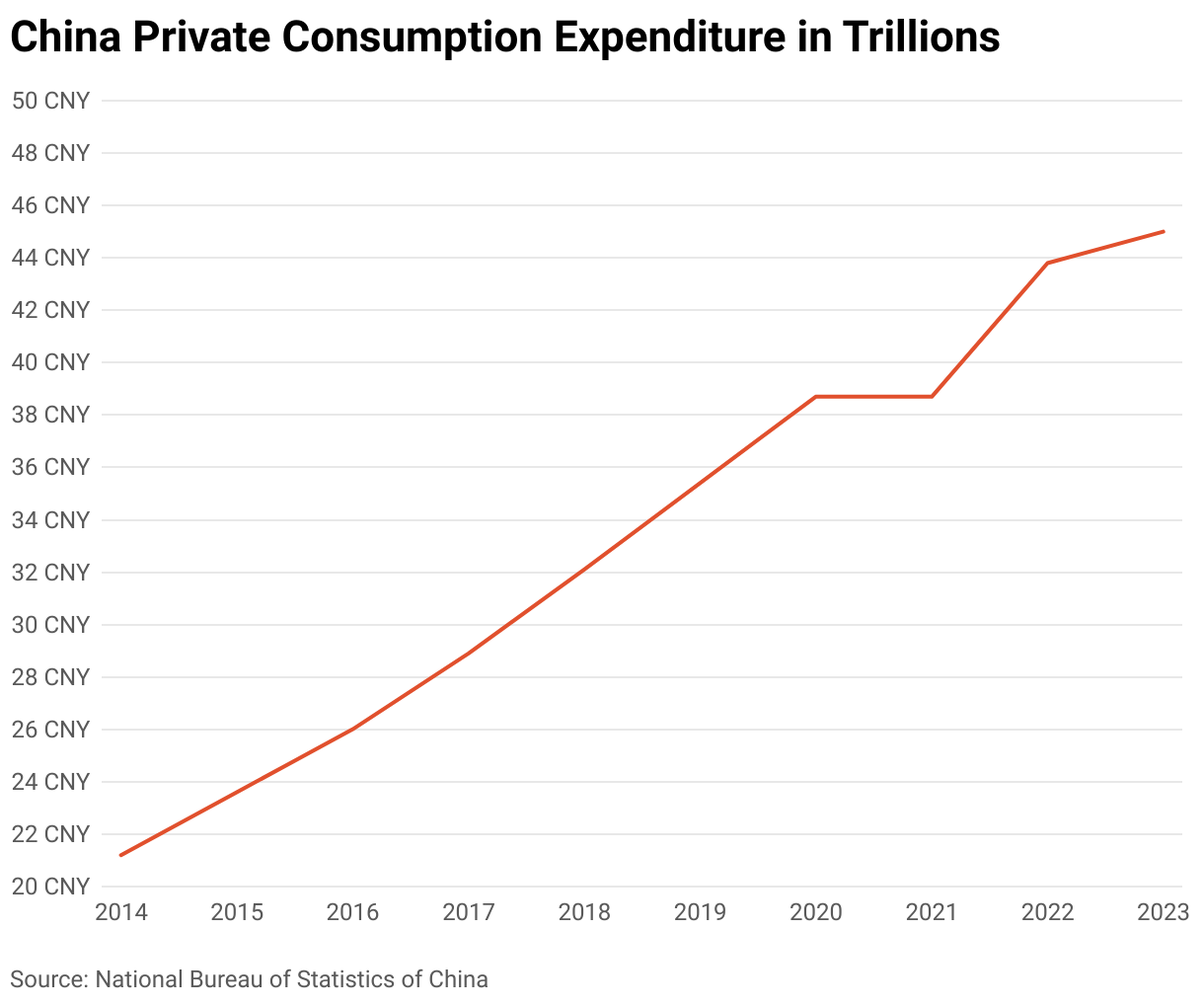

In 2022, household consumption accounted for just 38 percent of China’s GDP.

By comparison, private spending made up 68 percent of the GDP in the United States that same year.

“Households ran down savings during the pandemic,” Sheana Yue, a China economist at Capital Economics, told Al Jazeera. “The real-estate crash undermined consumer confidence even further. China also has an ageing population and, typically, spending declines with age.”

The upshot is that gross national savings exceeded 40 percent in 2023, more than double the US level.

“Looking ahead, getting people to spend their savings won’t be easy. For decades, economists have encouraged the government to rebalance the economy away from investment in favour of consumption,” Yue said.

At 42 percent of GDP, China’s rate of investment dwarfs that of other emerging economies, let alone advanced economies – which average 18-20 percent. In addition to housing stock, Beijing has invested heavily in roads, bridges and train lines.

As with housing, however, years of over-investment have resulted in spare capacity. Revenues at China Railway, for instance, regularly fall short of costs. At the end of 2022, the state-backed agency was 6.11 trillion yuan ($886bn) in debt.

“We’re seeing the limitations of China’s capital-intensive infrastructure model,” Yue said.

“And given that interest rates are already quite low, Beijing will need to start stimulating consumption to generate high and stable growth.”

Yue said policymakers should remove incentives to hoard savings by spending more on education, healthcare and pension provisions.

Analysts expect the National People’s Congress, China’s rubber-stamp parliament, to again set an annual growth target of about 5 percent when it meets in March.

While many economists have exhorted Beijing to stimulate growth through household transfers, Victor Shih, an expert on the Chinese economy at the University of California, San Diego, expects investment-driven growth to continue to hold sway.

“Marxist ideology, which valorises industrial production, remains the fundamental basis for policymaking in Beijing,” Shih told Al Jazeera.

“In all likelihood, the government will continue to subsidise manufacturing. Consumption, by contrast, is viewed as indulgent.”

Shih added: “There are 1.4 billion people in China, so comprehensive social assistance would be extremely expensive, especially in a deflationary context.”

Shih said Beijing could raise household consumption by urging companies to pay higher wages but that “China’s manufacturing edge is partly based on subdued worker income”.

As such, “higher wages would undermine Chinese exports, which is an important source of output”, he said.

“I don’t think the government will shift budgetary priorities in favour of the Chinese people… which will likely result in a period of economic weakness.”

Separately, Beijing has other strategic priorities, said Gary Ng, a senior Asia Pacific economist at Natixis in Hong Kong.

“President Xi [Jinping] appears less keen on stimulating rapid growth than he is on optimising the economy for security and resilience,” Ng told Al Jazeera.

In recent years, Beijing has invested heavily in strategic industries like artificial intelligence and advanced computer chips.

By moulding industrial policy on the basis of national security, Beijing has set its sights on reducing its reliance on foreign technology and supporting its long-term geopolitical ambitions.

At the same time, Ng said, “Beijing has shown a new willingness to invest in more consumer-facing tech sectors, like renewable energy and electric vehicles.”

“Unlike property, these industries have the capacity to create jobs and promote economic self-sufficiency,” he said.

Ng also stressed that economic transformation takes time and that “there’s no magic pill for lightning-quick growth”.

“Investment in high-tech sectors should, slowly, reform China’s economic base,” he said. “Incidentally, private consumption is already on an upward trend.”

Gallagher, of Boston University, said China’s economic growth trajectory is healthier than sometimes portrayed.

“It’s easy to forget about China’s economic development since the 1990s. Growth has slowed from high levels lately but it still tallied at 5.2 percent last year,” Gallagher said. “Forecasts are equally solid for this year.”

“Hawks have been predicting the demise of China’s growth model for decades,” Gallagher added. “It is true, however, that to build on China’s remarkable success, Beijing has to shake off its timidity about the investment-consumption pivot.”

Gallagher said 2024 is likely to underscore the urgency of reform.

“If [US presidential candidate] Donald Trump is re-elected and chooses to engage in a new trade war, Beijing will want to be more self-reliant. The Year of the Dragon could be ideal for China to step up its efforts to unleash domestic consumption.”