Intel Corporation (INTC) has staged one of the market’s most remarkable turnarounds, with its stock surging on growing optimism surrounding its artificial intelligence (AI) ambitions, foundry expansion, and a string of high-profile customer wins. But according to a new report from SemiAnalysis, the company should raise capital while investor enthusiasm remains strong.

On June 11, the firm noted that Intel’s valuation is at its highest level since the dot-com era and said the company will need substantial funding to scale its foundry business, advance projects such as Terafab, and meet growing AI-driven demand for CPUs. SemiAnalysis urged Intel to “issue equity now,” estimating that the chipmaker could potentially raise $25 billion.

Rather than viewing equity issuance as a sign of weakness, SemiAnalysis sees it as a rare opportunity for Intel to strengthen its balance sheet, accelerate its foundry buildout, and position itself for the next phase of growth before capital needs become more urgent.

While a stock offering would likely dilute existing shareholders in the near term, proponents argue that additional capital could help Intel fund new fabs, secure future customer commitments, and reduce financial strain as it pursues one of the most ambitious transformations in the semiconductor industry. With Intel still requiring substantial investment to execute its foundry strategy and compete against industry leaders, the debate now centers on whether issuing shares at today’s higher valuation could ultimately create more long-term value.

About Intel Corporation Stock

Intel is a leading technology company specializing in the design, development, manufacture and marketing of semiconductor products, including microprocessors, chipsets, graphics processing units (GPUs), memory and related hardware for consumer, enterprise and industrial markets. Headquartered in Santa Clara, California, Intel remains a key player in data center, PC and emerging AI and networking segments. Intel’s market cap is $626.1 billion, reflecting its valuation among the world’s largest semiconductor companies.

Intel has delivered one of the most extraordinary rallies in the market over the past year. The semiconductor giant’s stock has surged 533.1% over the past 52 weeks and is up 245.5% year-to-date (YTD), dramatically outperforming both the broader market and most of its semiconductor peers.

The rally has been fueled by growing investor confidence in Intel’s AI strategy, foundry expansion, and a series of major customer and partnership announcements that have reshaped Wall Street’s outlook on the company.

Momentum has accelerated sharply in recent trading sessions. Intel stock has climbed 15.6% over the past five trading days, including a 9.3% surge on June 11, and another 6.5% gain on June 12.

The June 11 rally was sparked by an upgrade from Bank of America, which raised its rating on Intel to “Buy” and lifted its price target to $135, citing stronger confidence in the company’s AI and foundry growth prospects. Plus, the momentum was fueled as research firm SemiAnalysis argued that the company should take advantage of its soaring stock price and raise additional capital to support its ambitious turnaround and expansion plans.

The following day, investors continued piling into the stock as optimism surrounding Intel’s manufacturing business and AI opportunities remained strong.

Despite some volatility along the way, Intel’s remarkable run has transformed it from one of the market’s laggards into one of 2026’s best-performing large-cap technology stocks.

The stock is currently trading at a premium to its sector median at 177.96 times forward earnings.

Outstanding Financial Growth

Intel’s first-quarter 2026 earnings were released on April 23. The company reported revenue of $13.6 billion, up 7% year-over-year (YOY), while non-GAAP earnings per share (EPS) reached $0.29 versus $0.13 in the prior-year period, representing a 123% YOY increase and exceeding expectations. On a non-GAAP basis, net income rose to $1.5 billion, up 156% YOY.

The most important feature of the quarter was the acceleration in Intel’s data center and AI business, which is increasingly defined by CPU demand tied to AI workloads. Segment revenue reached $5.1 billion, up 22% YOY, materially outpacing the rest of the portfolio and well ahead of expectations. This growth was driven primarily by server CPUs, particularly Xeon processors, as hyperscalers and enterprises scale infrastructure for inference and emerging agentic AI systems. Management explicitly framed CPUs as the “essential role” in the AI era, reflecting a shift from GPU-centric training workloads toward CPU-heavy orchestration, inference, and real-time processing.

This CPU-led demand is not merely cyclical but structural. Industry data indicates that AI server architectures are evolving toward significantly higher CPU-to-GPU ratios, which is materially increasing unit demand and pricing power for server-grade processors. As a result, Intel is actively prioritizing production capacity toward data center CPUs, underscoring the centrality of this segment to near-term growth.

Outside of the data center, performance was more mixed but still constructive. The Client Computing Group generated $7.7 billion in revenue, up about 1% YOY, while the foundry business experienced around 16% growth.

Furthermore, Intel’s guidance reinforced the improving trajectory. For Q2 2026, the company expects revenue of $13.8 billion to $14.8 billion and non-GAAP EPS of $0.20.

Analysts predict EPS to be $0.63 for fiscal 2026, an improvement of 625% YOY, before surging by 54% annually to an EPS of $0.97 in fiscal 2027.

What Do Analysts Expect for Intel Stock?

Apart from Bank of America, some other analysts have also shown confidence. Last month, Benchmark raised its price target on Intel to $140 from $105 and reiterated its “Buy” rating, highlighting improving execution and stronger long-term earnings potential.

However, on the other hand, Northland downgraded Intel to “Market Perform” from “Outperform,” arguing that the stock’s explosive gains over the past year has pushed its valuation too high despite acknowledging meaningful progress in the company’s turnaround.

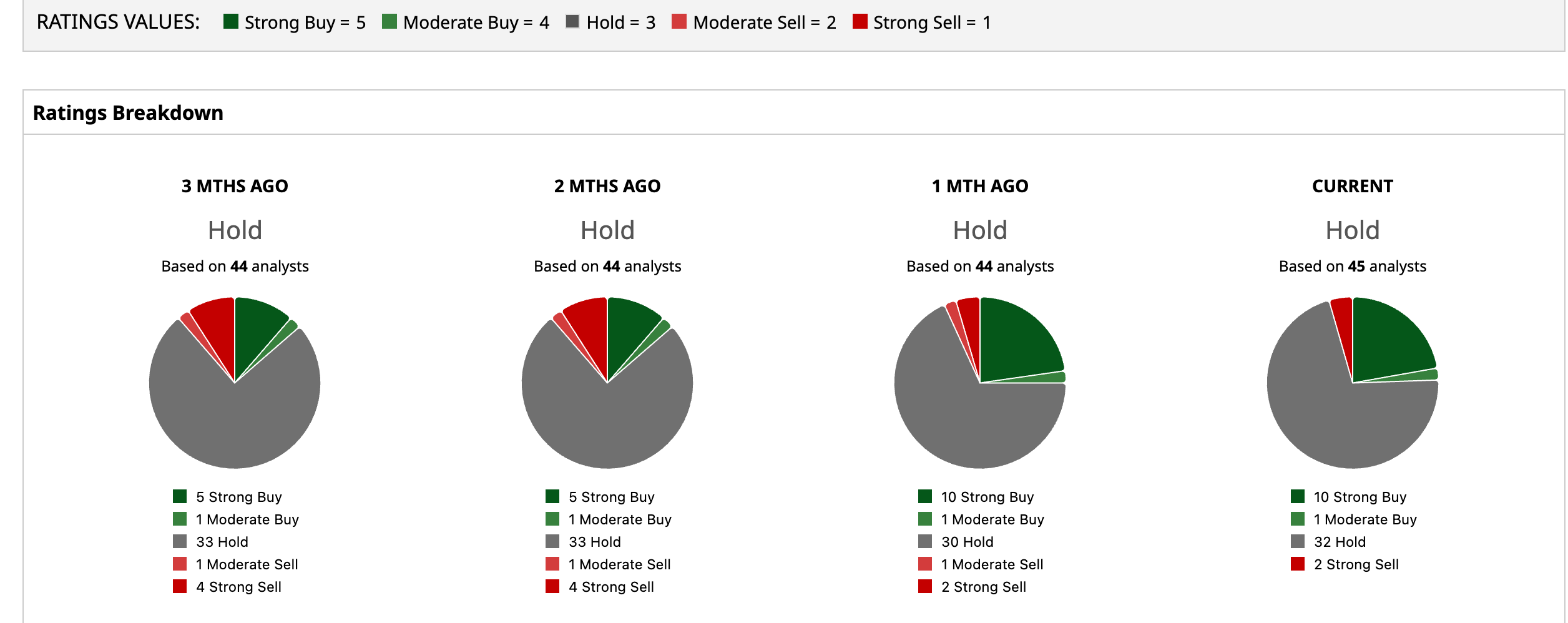

Despite the recent outperformance, INTC has a consensus “Hold” rating overall. Of the 45 analysts covering the stock, 10 advise a “Strong Buy,” one recommends a “Moderate Buy,” 32 analysts are on the sidelines, giving it a “Hold” rating, and two suggest a “Strong Sell.”

INTC has already surged past the average analyst price target of $91.86, while the Street-high target price of $150 suggests that the stock could rally 17.36%.