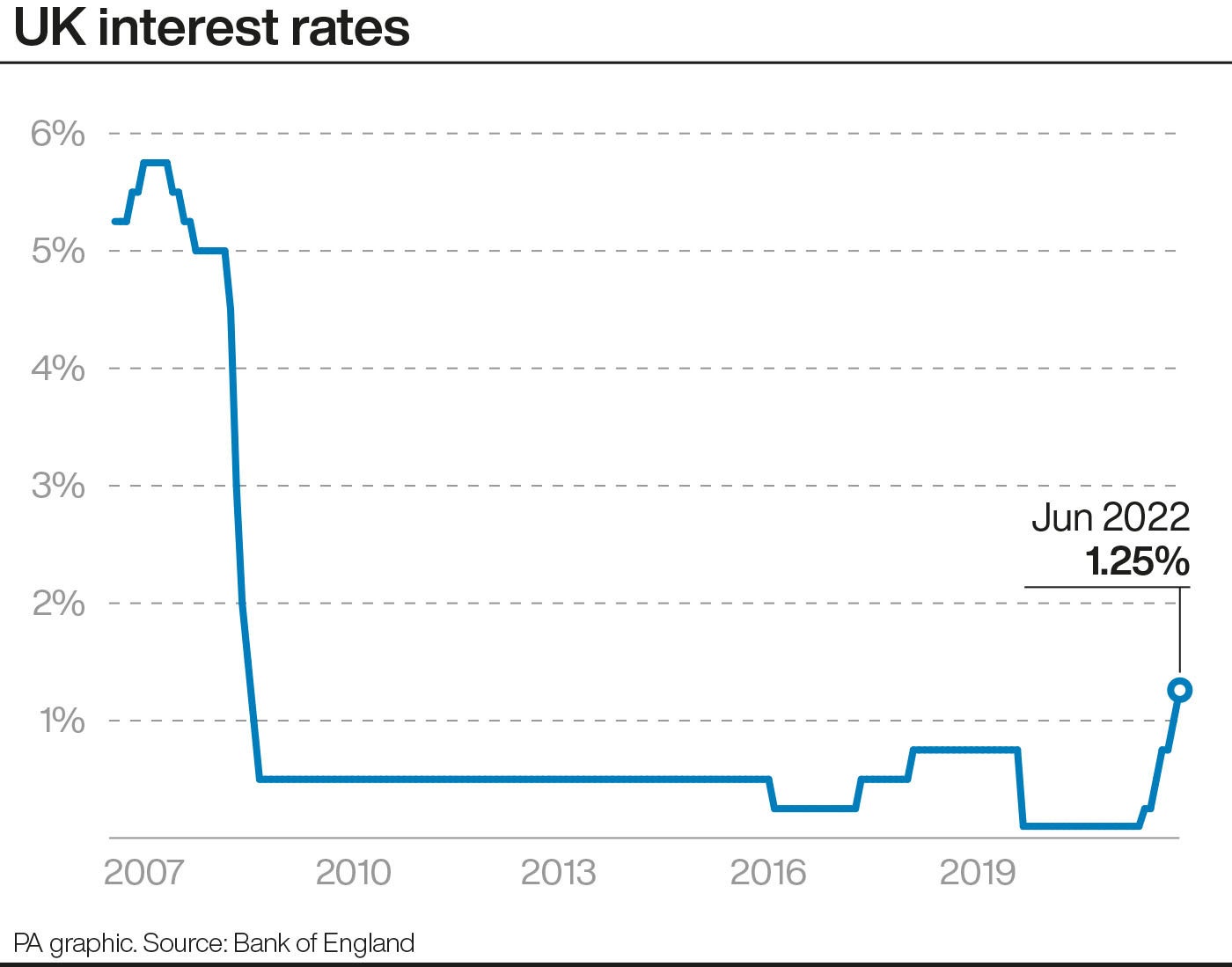

The latest Bank of England base rate rise will place a further squeeze on mortgage borrowers, while savers are yet to feel much benefit from the recent rate hikes, according to experts.

The rate edged up to 1.25% on Thursday, up from 1% previously, and is the latest in a string of hikes.

Krishnapriya Banerjee, a managing director in Accenture’s UK banking practice, said: “While the cost-of-living squeeze is undoubtedly hitting consumers hard, we’re now also seeing the rate rises taking their toll.

“A number of the major banks have raised fixed mortgage rates, forcing homeowners to pay hundreds of pounds more for new mortgages.

A number of the major banks have raised fixed mortgage rates, forcing homeowners to pay hundreds of pounds more for new mortgages. However, few are seeing this reflected in savings accounts— Krishnapriya Banerjee, Accenture

“However, few are seeing this reflected in savings accounts, as banks are yet to pass on higher interest rates to savers.”

Three-quarters (75%) of the just under nine million residential mortgages outstanding are fixed rates, according to trade association UK Finance. These borrowers will not immediately see the impact of the base rate increase on their mortgage payments.

Homeowners on variable deals tracking the base rate will see an impact. Some lenders may also decide to put up their SVRs (standard variable rates), which they set themselves.

The average SVR has already increased from 4.40% in December 2021 to 4.91% in June 2022, according to Moneyfacts.co.uk.

According to UK Finance, 1.3 million fixed mortgages are ending at some point this year – meaning many homeowners will be looking for a new deal.

David Hollingworth, associate director at mortgage adviser L&C Mortgages said: “We’ve seen more borrowers looking to secure a rate further ahead of the end of their current deal, in an effort to get ahead of the increases.”

Homeowners looking to fix into a new mortgage deal may find that their choice has shrunk.

According to financial information business Defaqto, the number of fixed-rate mortgages on the market has decreased recently.

It counted 1,953 fixed-rate mortgage deals available, down from 2,086 deals two months ago.

Speaking about the potential impacts on the housing market, Jason Tebb, chief executive officer of property search website OnTheMarket.com said: “As long as buyers remain confident about obtaining the mortgages they need and being able to afford them, modest increments in rates, while unwelcome, are unlikely to result in a slamming on of the brakes.”

Mark Manning, managing director at Leeds-based Northern Estate Agencies Group, whose brands cover areas including Manchester, Lancashire and Yorkshire, said: “It’s my view that the market will become more sensitive to prices being pushed too far, and sellers will need to be more realistic when deciding what price to sell for.”

Struggling first-time buyers, who already face the greatest hurdles in the housing market, may find themselves trapped in expensive rentals for even longer— Simon Leadbetter, Fine & Country

Simon Leadbetter, Global CEO of Fine & Country said: “Existing homeowners remain in a strong position to trade up given the gains they have made in the boom.

“Meanwhile struggling first-time buyers, who already face the greatest hurdles in the housing market, may find themselves trapped in expensive rentals for even longer.”

Rachel Springall, a finance expert at Moneyfacts.co.uk, said: “Borrowers who lock into a fixed deal can protect themselves from future rate rises, but those building a deposit may not be able to afford a mortgage as interest rates and living costs continue to climb.

“Fixed rates are on the rise, with the average two-year fixed-rate rising by almost one percentage point since December 2021.

“As the rate gap between the average two-year and five-year fixed-rate has narrowed, fixing for longer may be a sensible choice.

“Borrowers could even lock into a fixed mortgage for a decade if they are prepared to commit to such a lengthy fixed term.

“Seeking advice is sensible to assess the abundance of deals out there to ensure borrowers find the most appropriate choice based on the overall true cost.”

Ms Springall said switching from an SVR, which borrowers often end up on when their initial deal comes to an end, to a fixed rate could significantly reduce someone’s mortgage repayments.

She said: “The difference between the average two-year fixed mortgage rate and SVR stands at 1.66 percentage points, and the cost savings to switch from 4.91% to 3.25% is a difference of approximately £4,418 over two years (based on someone with a £200,000 mortgage over a 25-year term on a repayment basis).

SVRs are set by individual lenders, and Ms Springall said a rise of 0.25% on the current average SVR of 4.91% could add around £700 onto someone’s total repayments over two years, a calculation which was also based on having a £200,000 repayment mortgage.

Every penny in additional interest is a bonus when high inflation is eating away at the purchasing power of incomes— Alice Haine, Bestinvest

Ms Springall said for savers it can take a few months for the effects of rate rises to be seen.

She said the average easy access savings rate has crept up from 0.20% in December 2021 to 0.46% in June 2022.

Ms Springall said: “There is no guarantee savers will benefit at all but should they see 0.25% passed onto them, it would mean receiving £50 more a year in interest based on a £20,000 investment.

“Savers would be wise to review the top rate tables as there have been notable improvements over the past few months.

“The best deals today may not have a very long shelf life and some may require certain eligibility criteria to be met.”

Alice Haine, personal finance analyst at investment platform Bestinvest said: “Every penny in additional interest is a bonus when high inflation is eating away at the purchasing power of incomes. With many households dipping into emergency pots to meet rising food, fuel and energy bills, you need to make sure your money is working as hard as it can.

“Those with longer term horizons – more than five years and ideally at least 10 – might want to consider investing it in the markets – taking advantage of lower asset values in these volatile times.

“While higher returns from the markets is never guaranteed, a long-term approach means your investment portfolio can absorb the highs as well as the lows and deliver better growth over the long term.”