/Synopsys%2C%20Inc_%20HQ%20sign-by%20Sundry%20Photography%20via%20Shutterstock.jpg)

Valued at a market cap of $94.3 billion, Synopsys, Inc. (SNPS) is a leader in Electronic Design Automation (EDA) and semiconductor intellectual property (IP). The Sunnyvale, California-based company provides the advanced software tools, silicon IP blocks, and verification systems essential for designing, simulating, and manufacturing complex integrated circuits and artificial intelligence (AI) chips.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and Synopsys fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the software - infrastructure industry. The company's premier strength is its pioneering Synopsys.ai suite, the industry's first full-stack, AI-driven EDA deployment, which utilizes machine learning to autonomously optimize "Power, Performance, and Area" (PPA) and dramatically compress chip tape-out timelines.

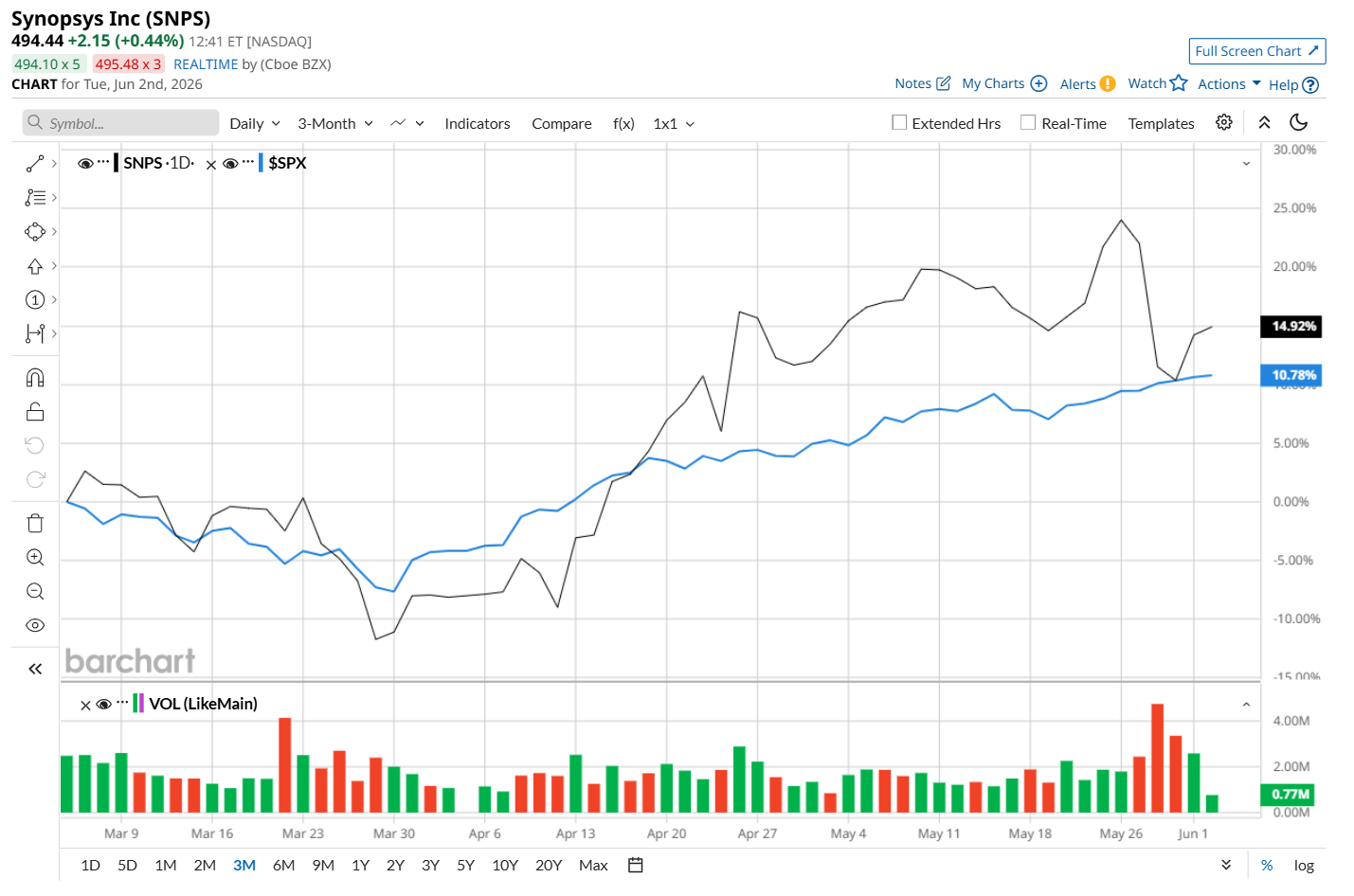

This tech company is currently trading 24% below its 52-week high of $651.73, reached on Jul. 30, 2025. Shares of SNPS have soared 17.3% over the past three months, outperforming the S&P 500 Index’s ($SPX) 10.6% rise during the same time frame.

However, in the longer term, SNPS has gained 6.9% over the past 52 weeks, lagging SPX's 28.3% uptick over the same time period. Additionally, on a YTD basis, shares of Synopsys are up 6%, compared to SPX’s 11.2% increase.

To confirm its recent bullish trend, SNPS has been trading above its 200-day moving average since late April, and has remained above its 50-day moving average since mid-April.

On May 27, SNPS posted better-than-expected Q2 results, yet its shares plunged 8.6% in the following trading session. The company’s total quarterly revenue surged 41.9% year over year to $2.3 billion, exceeding analyst estimates by 1.3%, driven primarily by a 62.3% increase in its Design Automation segment following the consolidation of Ansys. Additionally, its adjusted EPS came in at $3.35, comfortably ahead of the consensus estimate of $3.17. Despite the strong performance, investor sentiment was weighed down by concerns over near-term growth deceleration and management’s cautious commentary on the early-stage monetization of its AI initiatives. Looking ahead, the company raised its fiscal 2026 guidance, projecting full-year revenue of $9.665 billion and adjusted EPS of $14.76 at the midpoint.

SNPS has outpaced its rival, Microsoft Corporation (MSFT), which dropped 3.9% over the past 52 weeks and 8.2% on a YTD basis.

Looking at SNPS’ recent outperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 21 analysts covering it, and the mean price target of $566.95 suggests a 14.8% premium to its current price levels.