/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

Intel (INTC) stock has had a wild ride this year, and Wall Street is taking notice. One of the loudest signals just came from KeyBanc Capital Markets, which made a bold call on where the chipmaker is headed next.

The firm's updated price target of $155 is well above its current trading level and suggests that INTC could gain another 45% from here. The new INTC stock price target is a notable increase, and it comes at a time when the company's turnaround story is gaining momentum.

Intel has been through a major shakeup under CEO Lip-Bu Tan, and investors are watching closely to see if it is finally paying off.

Intel's Turnaround Under Lip-Bu Tan

Lip-Bu Tan took over as Intel's chief executive in March 2025. Since then, he has trimmed management layers, cut the number of vice presidents by nearly half, and reduced headcount from more than 100,000 to under 80,000, according to comments by Intel CFO David Zinsner at the Bank of America 2026 Global Technology Conference.

Zinsner described the changes as rooted in a cultural shift, telling attendees that Tan pushed for more transparency and told staff that hiding problems, rather than the problems themselves, was what would get someone fired.

That shift, paired with a leaner org chart, helped Intel work through issues that had been quietly dragging down execution for years. Tan told the JPMorgan 54th Annual Global Technology, Media, and Communications Conference that Intel brought in outside investment from the U.S. government, Nvidia (NVDA), and SoftBank (SFTBY) to shore up its finances.

Why KeyBanc Is Bullish on INTC Stock

According to Investing.com:

- KeyBanc raised its Intel price target to $155 from $110 while maintaining an “Overweight” rating, citing strong server CPU demand tied to agentic AI trends.

- While Intel has not been profitable in recent quarters, analysts expect the company to return to profitability this year, which supports the more optimistic view.

- KeyBanc noted that Intel has expanded capacity at its Arizona facility to support server unit growth of more than 25% this year and over 50% next year.

- Yields on the 18A manufacturing process have climbed above 85%, up from 65% just one quarter earlier, per the outlet.

- KeyBanc believes Intel has landed design wins with Apple (AAPL) , AMD (AMD) , Nvidia, Marvell (MRVL) , Microsoft (MSFT) , Micron (MU) , and OpenAI, plus a second major win on its EMIB packaging technology with AWS Trainium 3 and Google's (GOOG) (GOOGL) TPU program.

- The firm also pointed to planned client CPU price increases of 6% to 15% in the third quarter of 2026 and introduced 2030 estimates of $132 billion in revenue and $7.58 in earnings per share, with the $155 target based on 20 times that 2030 earnings figure.

The yield improvement aligns with what Zinsner described at the Bank of America conference, where he said Intel is now likely to hit its manufacturing milestones a full quarter ahead of schedule, and possibly more.

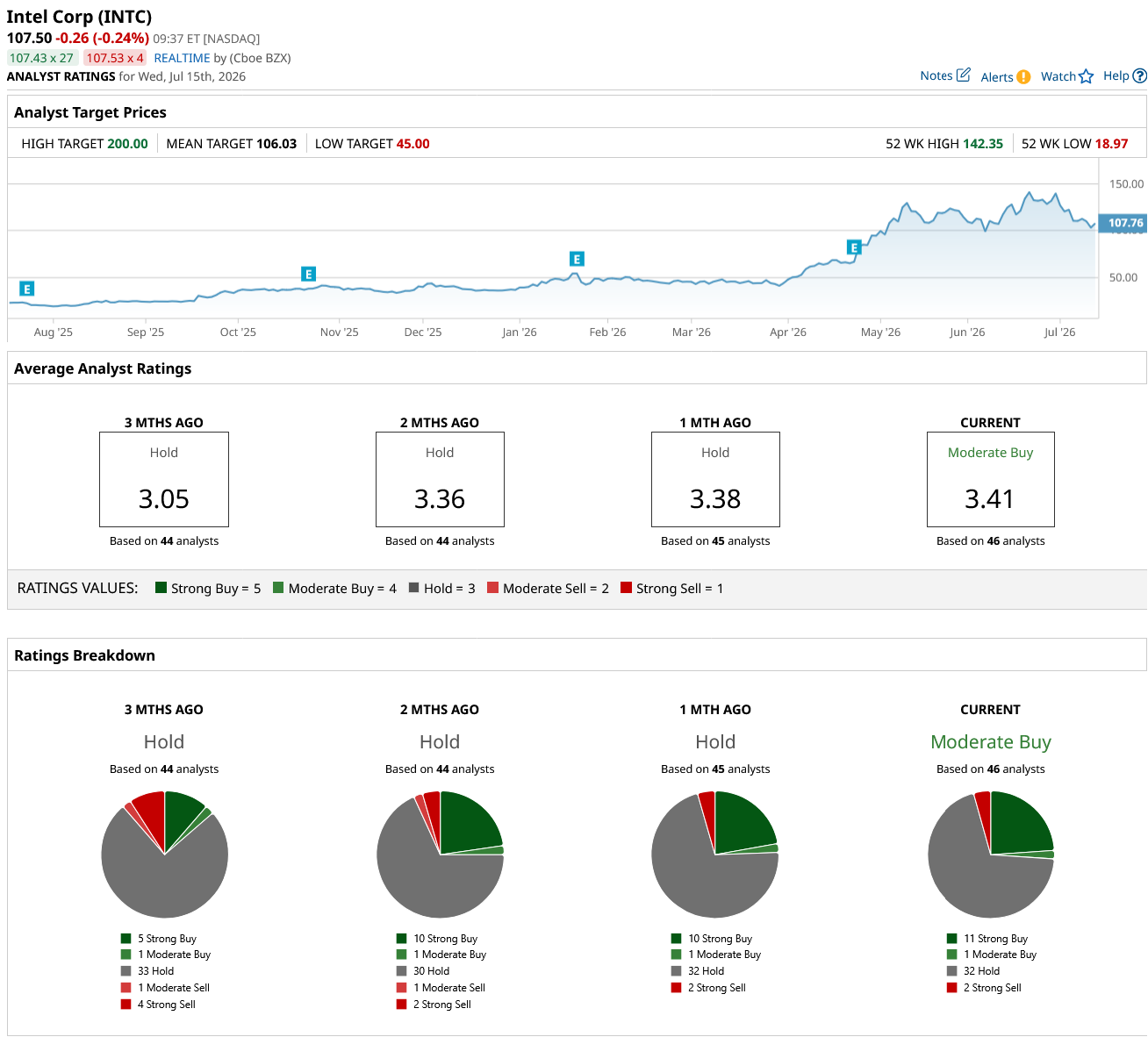

At the time of writing, INTC stock is trading at about $107, valuing the chipmaker at a market cap of $518 billion. The tech stock has risen close to 380% over the last 12 months. Out of the 46 analysts covering INTC stock, 11 recommend “Strong Buy,” one recommends “Moderate Buy,” 32 recommend “Hold,” and two recommend “Strong Sell.” The average Intel stock price target is $106.03, which is similar to the current price.

What This Means for the CPU Market

The bullish case rests on demand for server chips tied to artificial intelligence. At Intel's Computex keynote in Taipei, executive Kevork Kechichian explained that agentic AI workloads rely much more heavily on CPUs than traditional AI training did, since agents need to plan, use tools, and manage tasks in ways that suit the strengths of processors rather than graphics chips.

Tan echoed this at the JPMorgan conference, saying customers have told him the ratio of CPUs to GPUs needed for these workloads is shifting quickly, from the old model of one CPU for every eight GPUs toward something closer to one-to-one, and in some cases even four CPUs for every GPU.

Zinsner was more cautious about pinning down an exact number for the total addressable market but agreed the opportunity is large enough that execution, not demand, is now the main thing standing in Intel's way.

For investors watching the stock, KeyBanc's new target reflects a bet that Intel's manufacturing recovery and the AI-driven CPU boom are both real and durable, not just a short-term bounce.