Universal Health Services, Inc. (UHS) is a large healthcare management company operating acute care hospitals, behavioral health facilities, freestanding emergency departments and outpatient centers. Through its subsidiaries, it delivers inpatient and outpatient services across diverse communities. The company is headquartered in King of Prussia, Pennsylvania, and has a market capitalization of $9.59 billion.

UHS is expected to report its second-quarter results for fiscal 2026 soon. Ahead of the release, Wall Street analysts are optimistic about the company’s bottom-line trajectory.

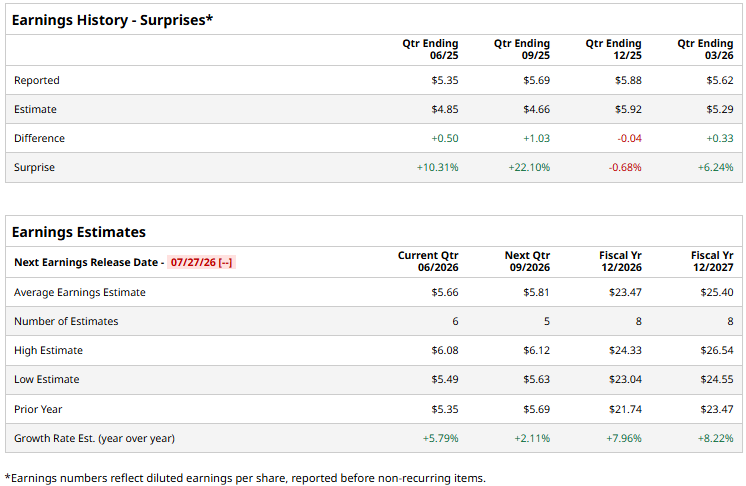

Analysts expect UHS to report a profit of $5.66 per share on a diluted basis for Q2, up 5.8% year-over-year (YOY). The company has a solid history of surpassing consensus estimates, topping them in three of the four trailing quarters. For the full fiscal year 2026, Wall Street analysts expect UHS’ diluted EPS to grow by 8% annually to $23.47, followed by an 8.2% improvement to $25.40 in fiscal 2027.

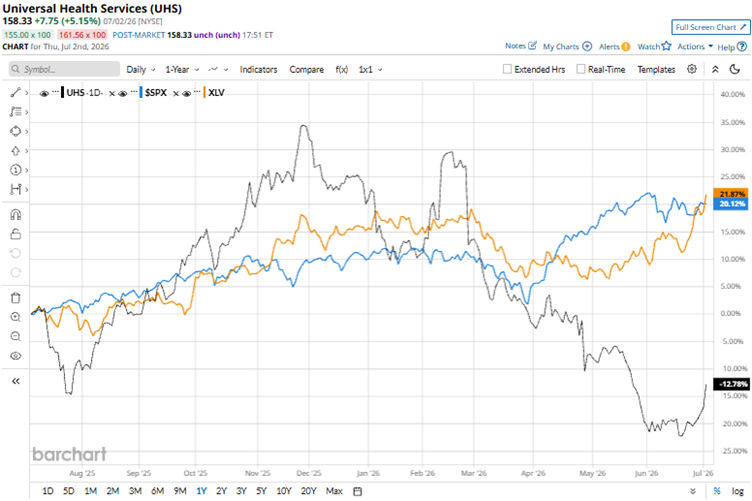

Ongoing adjustments to Medicaid and other public reimbursement programs, which have increased uncertainty about the future revenue mix, have led to declines over the past year. Over the past 52 weeks, UHS’ stock has declined 14.2% and by 27.4% year-to-date (YTD). On the other hand, the broader S&P 500 Index ($SPX) has increased by 20.2% and 9.3% over the same periods, respectively. Therefore, the stock has underperformed the broader market.

We now compare UHS’s performance with that of its sector. The State Street Health Care Select Sector SPDR ETF (XLV) has increased 21% over the past 52 weeks and 5.8% YTD. Therefore, the stock has also underperformed the sector over these periods.

For the first quarter of fiscal 2026, UHS reported $4.50 billion in revenue (up 9.6% YOY), as the company reported growth across its acute care services and behavioural health care services segment, both in terms of net revenue per adjusted admission and net revenue per adjusted patient day. The company’s adjusted EPS increased 16.1% YOY to $5.62. Despite UHS reporting better-than-expected Q1 results, the stock dropped by 9.5% intraday on Apr. 28.

Wall Street analysts have been bullish about UHS’ future. Among the 20 analysts covering the stock, the consensus rating is “Moderate Buy.” The rating configuration has remained roughly the same over the past two months. UHS has seven “Strong Buy” ratings, 12 “Holds,” and one “Moderate Sell.” The mean price target of $210.12 implies a 32.7% upside from current levels, while the Street-high price target of $310 implies 95.8% upside.