UnitedHealth (UNH) stock is pushing higher on Tuesday after the insurance giant posted a strong Q1 and raised its full-year profit guidance to at least $18.25 per share.

The post-earnings momentum drove UNH’s relative strength index (RSI) into the 80s, indicating the stock is now overbought and may be due for a technical correction in the days ahead.

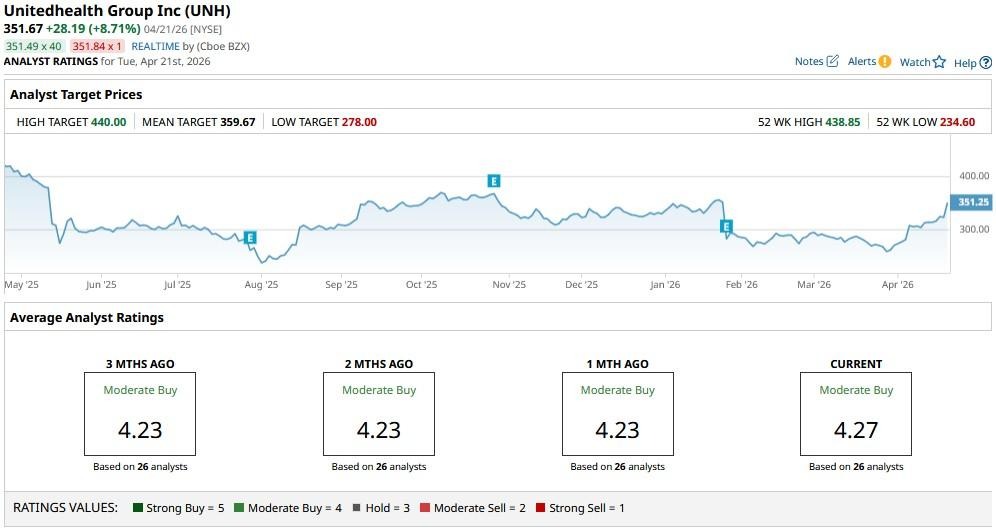

Versus its recent low, UnitedHealth stock is now up a whopping 35%.

Why Q1 Earnings Warrant Buying UnitedHealth Stock

UNH’s adjusted EPS of $7.23 was impressive, but the real victory is its medical care ratio (MCR), which dropped to 83.9% in the first quarter — significantly better than 85.5% expected.

This helps ease concerns that rising medical utilization and high Medicare Advantage costs would permanently erode margins.

By successfully repricing contracts and exiting underperforming markets, UnitedHealth Group has demonstrated that it can maintain discipline despite regulatory headwinds.

More importantly, the raised guidance suggests fallout from previous “cyberattacks” and Medicare reimbursement cuts are finally in the rearview mirror, shifting the narrative from crisis control back to operational excellence.

A healthy 2.52% dividend yield makes UNH shares even more attractive to own in 2026.

What Else Could Drive UNH Shares Higher in 2026?

Beyond earnings excitement, UnitedHealth shares remain attractive because of a strong regulatory tailwind — the finalized 2.48% Medicare Advantage reimbursement rate for 2027.

For UNH, this finalized rate means much-needed visibility into revenue growth.

Plus, at 0.66x sales, the health insurance giant is still trading at a discount to its historical averages, which — combined with strong Q1 results — reinforces that it’s a broken stock, not a broken company.

The Optum segment makes up for another strong reason to own UNH this year, with management seeing its annual operating earnings sustainably growing by 9% as vertical integration matures.

In short, with a solid $8.9 billion in quarterly operating cash flow and a fairly diversified portfolio, UnitedHealth offers a rare blend of defensive stability and high-teen earnings growth potential.

Wall Street Remains Bullish on UnitedHealth Group

Wall Street remains bullish as ever on UnitedHealth Group after its strong Q1 earnings today.

The consensus rating on UNH stock sits at a “Moderate Buy” currently, with the mean price target of about $440 indicating potential upside of another 26% from here.