PNC Financial Services Group (PNC) is sending a clear message to investors who care about steady income. In early July, the bank lifted its quarterly dividend by 17.6%, pushing the stock’s forward yield into more appealing territory for dividend buyers.

This move didn’t come out of nowhere. The increase follows a strong start to 2026, with revenue of $6.17 billion and a solid 12.5% year‑over‑year (YOY) gain in the first quarter, pointing to growing business momentum.

The announcement also lands after a reassuring regulatory checkup. All 32 of the nation’s biggest banks, including PNC, passed the Federal Reserve’s annual “stress test,” showing they have the capital strength to handle a severe downturn.

PNC’s decision naturally prompts a key question for investors: Is this just a one‑off headline move, or the beginning of a more durable high‑yield story that is truly backed by earnings and a strong balance sheet? Let’s dive in.

The Numbers Behind PNC's 17.6% Dividend Jump

PNC is a diversified bank based in Pittsburgh, Pennsylvania. It runs retail, commercial, and wealth‑management operations across the United States and has a market capitalization of about $101.5 billion.

Recently, PNC backed up its story with a big change to its dividend. The board approved a new quarterly cash dividend of $2 per share, up $0.30 from the prior $1.70. The raise marks a roughly 18% increase, with the new dividend to be paid on Aug. 5, 2026 to shareholders of record at the close of July 20, 2026.

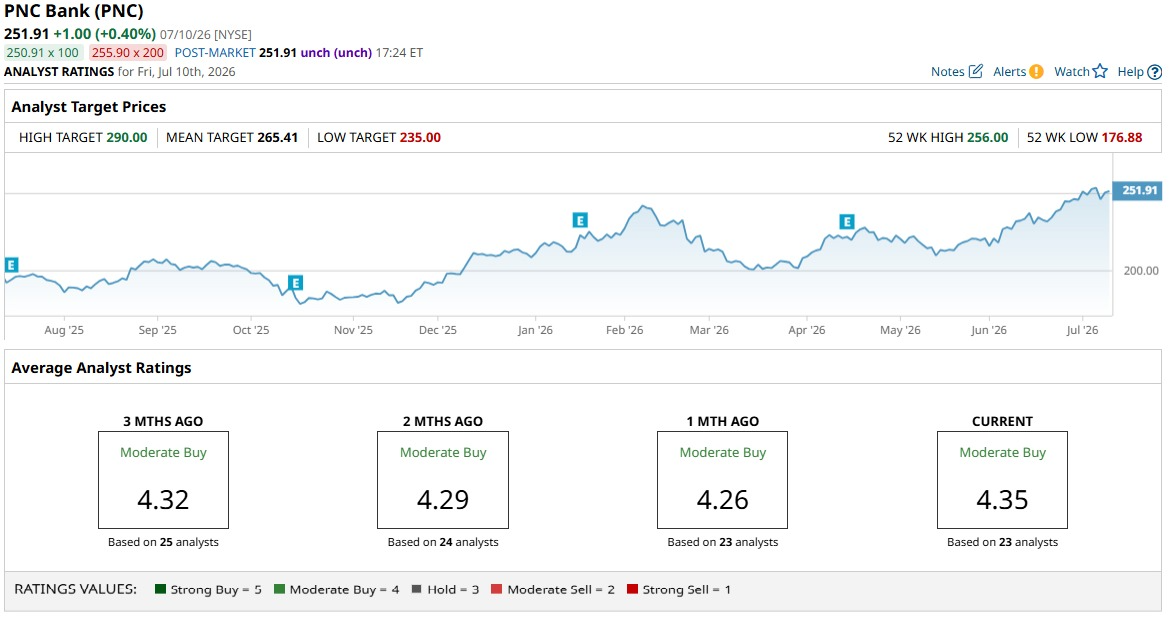

PNC stock trades near $252 as of July 14, with a year‑to‑date (YTD) gain of 21% and a return of almost 28% for the past 52 weeks.

Investors are paying up for those numbers, but not wildly so. Shares of PNC trade at 14.4 times trailing earnings and a price‑to‑cash flow (P/CF) ratio of 13.5 times, versus sector medians of 12.2 times and 10.4 times. That points to a reasonable premium.

The earnings release on April 15 helps show why management is comfortable raising the dividend. PNC posted adjusted EPS of $4.32 in Q1 2026 compared with estimates of $4.12, a nearly 4% beat that translated into a roughly 5% earnings surprise.

Net interest income came in at $3.96 billion, just below analyst estimates of $3.97 billion but still a strong 14% YOY increase. The Q1 report also showed a net interest margin of 3%, in line with forecasts.

PNC delivered total revenue of $6.17 billion versus expectations of $6.26 billion. That was a small 1.6% miss, yet still meant 12.5% YOY growth. The efficiency ratio came in at 61% against an expected 60.8%, a modest 22.7 basis‑point difference.

Finally, the bank reported operating cash flow of about $1.93 billion in March 2026, down 56% sequentially. Net cash flow of roughly ‑$8.01 billion also widened almost 23% sequentially from -$6.53 billion.

PNC’s Moves Funding the Raise

PNC Financial’s completion of the FirstBank customer conversion is central to its dividend raise. This shift brought about 780,000 customers, more than 1,620 employees, and 95 branches in Colorado and Arizona onto PNC’s systems. The move has given former FirstBank clients access to a full product set, digital banking tools, treasury‑management solutions, and wealth‑management services, as well as access to a branch and ATM network of roughly 2,400 locations and 58,000 machines.

That expansion is paired with targeted wealth‑management initiatives. PNC Wealth Management recently launched Premier Client, an integrated banking and investing service for emerging and “mass affluent” customers, combining everyday banking with tailored investment and advisory solutions in one relationship. PNC Wealth Management has also introduced online brokerage account opening, giving clients a streamlined digital way into self‑directed investing and portfolio building while staying within the PNC ecosystem. This feature reduces friction for customers managing their own assets and adds another fee‑based revenue stream tied to trading and asset balances.

Together, these moves show a bank expanding both its geographical footprint and its wealth platform.

What Does Wall Street Think About PNC?

Earnings expectations for PNC in the near term line up well with the next earnings release scheduled for July 15 before the market opens. The current consensus estimate for the quarter ended June 2026 is for EPS of $4.51. That compares with $3.85 in the same quarter a year ago, implying 17% YOY growth.

Analysts seem comfortable with that trajectory. On May 8, Citigroup analyst Keith Horowitz kept a “Buy” rating on PNC stock and nudged his price target from $245 to $255. That implies about a 1.3% potential upside from current levels.

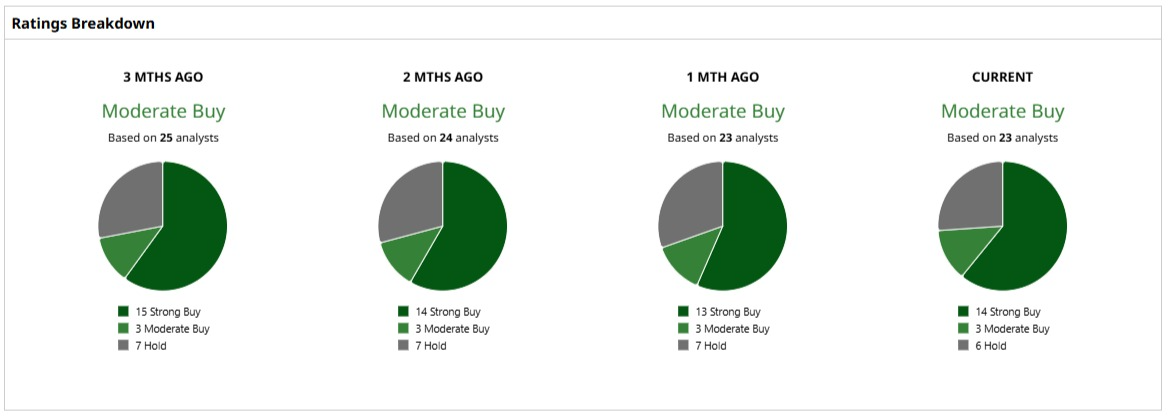

Views across the wider analyst group line up with that stance. PNC stock has a “Moderate Buy” consensus rating, based on 23 analysts with coverage. The average price target of $265.41 suggests potential upside of more than 5% from here.

Conclusion

PNC has made a pretty clear statement with this dividend hike, and the numbers mostly back it up. Earnings are growing at a healthy clip, the balance sheet is solid, and analysts see more upside than downside from here. If management keeps hitting its targets and integration stays on track, shares are more likely to drift higher than meaningfully roll over, especially for investors who value that richer income stream.