Investment bank JPMorgan just published its highly anticipated list of 47 top stock picks for 2026, a carefully curated selection of companies the firm believes will deliver outsized returns over the coming year. The list spans a wide range of industries, from technology and healthcare to financials, energy, and consumer discretionary. Yet only one name from the telecommunications sector made the cut: AT&T (T).

JPMorgan assigns AT&T an “Overweight” rating and sets a one-year price target of $33 per share, implying approximately 35% upside from recent trading levels. The stock currently offers a forward dividend yield of around 4.5%, making it one of the highest-yielding large-cap names in the market. Despite rising 8% over the past year and having an attractive income stream, AT&T shares have fallen 18% from their September high of $29.79 per share.

This recent weakness has raised questions among investors over whether the pullback is a buying opportunity, or a sign of deeper challenges. With JPMorgan’s bullish endorsement and a generous dividend, does AT&T deserve a place in a long-term portfolio?

About AT&T Stock

AT&T is one of America’s largest telecommunications providers, delivering wireless, broadband, and fiber-optic services to more than 100 million customers. Headquartered in Dallas, Texas, at the iconic Whitacre Tower, the company operates the nation’s largest wireless network by coverage and continues to aggressively expand its fiber-to-the-home footprint through its ongoing fiber deployment program.

Over the past 12 months, AT&T stock is up 8%, reflecting steady execution and subscriber growth in both wireless and broadband segments. However, the shares experienced a sharp decline from their recent peak after a strong run-up through much of the year.

Several factors contributed to the selloff: intensified promotional activity in the wireless industry, which pressured average revenue per user (ARPU); investor concerns about potential subscriber churn amid economic uncertainty; and broader market rotation away from high-yield dividend stocks as interest rates remained elevated.

Despite these headwinds, AT&T has continued to demonstrate operational strength, generating consistent free cash flow and advancing its strategic shift toward higher-margin fiber and 5G services.

What JPMorgan Sees in AT&T

JPMorgan analyst Sebastiano Petti, who covers the telecommunications sector for the firm, has been consistently upbeat about AT&T. In recent investor notes, Petti has highlighted several key drivers behind his “Overweight” rating and $33 price target. He points to AT&T’s strong competitive position in postpaid wireless, where the company has been gaining market share through improved customer experience and network quality.

Petti also emphasizes the accelerating momentum in AT&T’s fiber business, which is benefiting from increasing penetration rates and robust demand for high-speed internet. The analyst has underscored the company’s convergence strategy – integrating wireless and wireline services – as a critical differentiator that should help AT&T capture more wallet share from customers.

Additionally, Petti notes that AT&T’s capital spending is expected to moderate in coming years, freeing up more free cash flow for debt reduction and dividend support. These factors, combined with a disciplined approach to promotions and cost management, underscore JPMorgan’s confidence that AT&T can deliver solid EBITDA growth and sustained shareholder returns through 2026 and beyond.

What Do Other Analysts Expect for AT&T Stock?

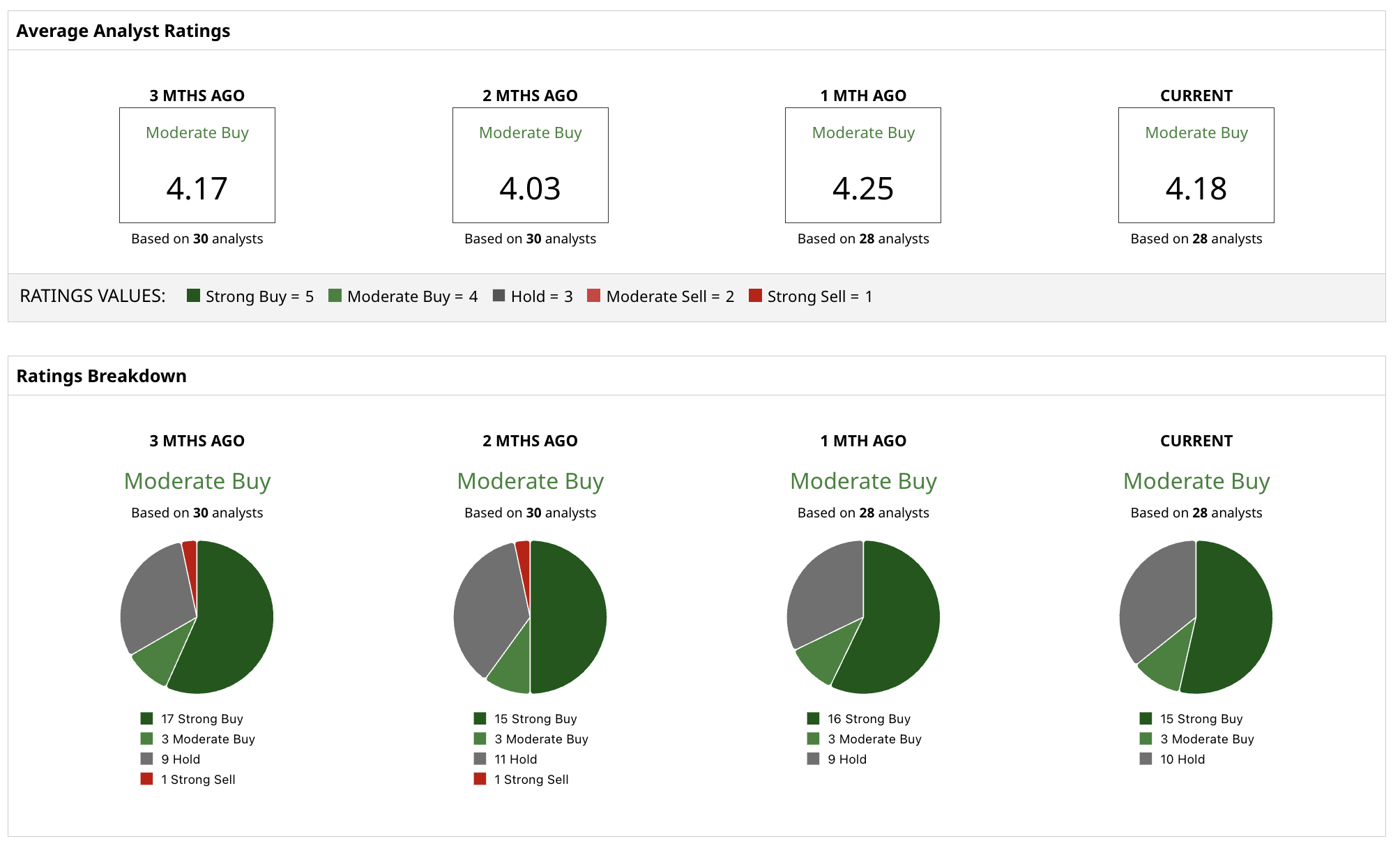

Wall Street’s broader view of AT&T is also positive with a consensus “Moderate Buy” rating. Of the 28 analysts currently covering the stock,15 have a “Strong Buy” rating, 3 see it as a “Buy,” and 10 assign a “Hold” rating. There have been no significant downgrades and only modest adjustments to price targets following quarterly earnings reports.

Analysts have a mean price target of $29.68 per share, implying 20% upside from its current level of $24.60 per share. While this is slightly below JPMorgan’s more bullish $33 call, it still reflects meaningful appreciation potential.

The broad agreement on Wall Street is that AT&T’s current valuation, coupled with its high dividend yield and strategic progress, offers patient investors an attractive risk-reward profile.