/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

Canaccord Genuity’s senior analyst George Gianarikas upgraded FuelCell Energy (FCEL) on June 9 from “Hold” to “Buy,” and more than doubled his price target to $30 per share.

The upgrade represents about 100% potential upside from FCEL’s prior closing price and reflects growing conviction that the company is on the verge of securing a transformative data center deal before the end of its current fiscal year.

Despite recent gains, FuelCell stock is currently down more than 30% versus its year-to-date high.

FuelCell Energy Had a Disappointing Q2

In his research note, Gianarikas cited accumulating evidence that FCEL’s clean power technology is positioned to serve the rapidly expanding AI data center market, drawing parallels to commercial success already achieved by industry leader Bloom Energy (BE).

The timing of the upgrade coincided with FuelCell’s fiscal second-quarter (Q2) earnings report, which on its face was disappointing.

The company posted an adjusted loss of $0.53 on a per-share basis and $35.6 million in revenue, missing consensus estimates as a $42.6 million non-cash impairment charge related to its “Groton Navy” project ballooned the net loss to nearly $79 million.

In Q2, FCEL’s revenue declined 5% year-over-year due to lower service and generation income while its backlog also slipped some 10% from the year-ago period.

Why Canaccord Is Still Bullish on FCEL Shares

Despite a muted quarter, FuelCell’s forward-looking narrative proved compelling enough for the Canaccord analyst to act.

In the earnings report, management said the submitted proposal timeline surged 267% sequentially to 4 gigawatts, with data center customers accounting for about 89% of that total.

The average proposal size doubled to 130 megawatts, indicating engagement at hyperscale levels.

FCEL has introduced a standardized 12.5 megawatt modular power block designed specifically to accelerate time-to-power for AI-driven compute facilities in grid-constrained environments.

To support anticipated demand, FCEL raised its Torrington manufacturing expansion target from 350 megawatts to 500 megawatts of annual capacity, with an estimated capital cost of at least $200 million over two years.

The company ended its fiscal Q2 with $373 million in unrestricted cash and remained debt-free, providing a meaningful runway to fund the expansion without near-term liquidity concerns.

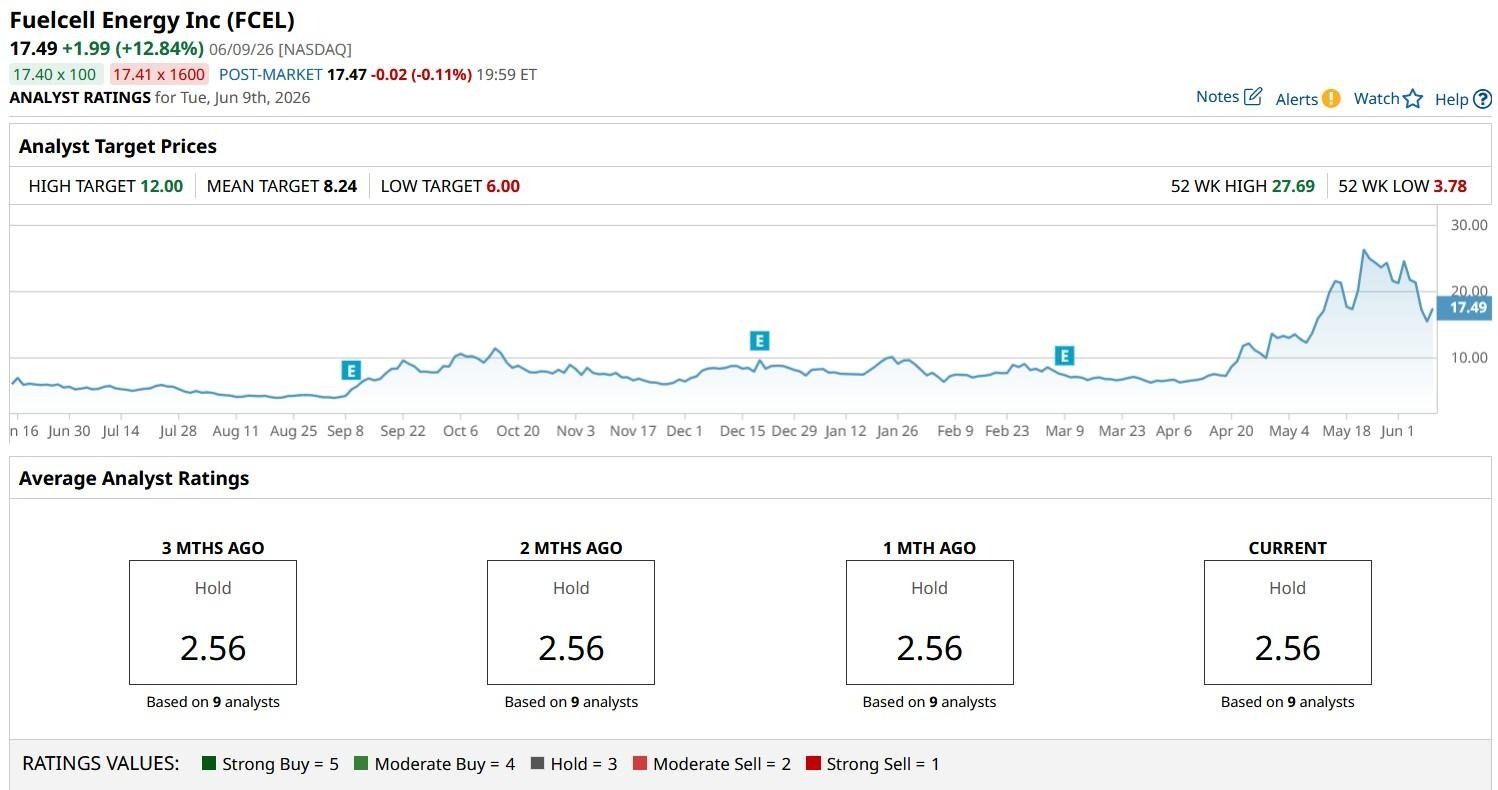

What’s the Consensus Rating on FuelCell Stock?

Investors should note, however, that other Wall Street analysts disagree with Gianarikas on FCEL stock.

The consensus rating on FuelCell Energy sits at “Hold” only, with the mean price target of just over $8 signaling potential downside of more than 50% from here.

Short interest also stands at more than 10% of the float, the highest level year to date, indicating significant skepticism remains about FCEL’s ability to convert pipeline into contracted revenue.

All in all, the investment case hinges entirely on whether management can translate proposals into binding contracts and achieve the production scale needed to reach positive adjusted EBITDA, a threshold the company itself ties to consistent annualized volumes at or above 100 megawatts.

Disclaimer: This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.