I visited one of my oldest friends this past December. As a “geriatric” millennial pushing 40, it was jarring for me to realize I’ve known this man for 21 years, since we were freshmen in college, cheerfully predicting capitalism’s imminent demise in our dorm rooms. He was the friend who introduced me, in 2001, to the ideas of a firebrand socialist from his home state of Vermont named Bernie Sanders. He told me Bernie was going to do big things in the future.

We were, of course, wrong about capitalism. It’s going strong. But we aren’t alone, as millennials, in our ambivalence about an economic system that seems to have failed our generation at every turn, leaving us despairing about our prospects for home ownership and retirement, and facing down an increasingly undeniable environmental disaster.

Maybe we inherited some of this skepticism of capitalism from our Generation X forebears, with their slackerish anti-sellout stance. Running throughout the Gen X pop culture we grew up with was a meta-commentary about how capitalism ruined everything it touched. From watching Pee-Wee’s Playhouse as a toddler, to The Simpsons as a kid, and then Community in my 20s, I could not miss the message that capitalism was driving everything, and life was increasingly ludicrous as a result. By the time my generation took the wheel of mass entertainment, even the Marvel superheroes were endlessly self-aware, and thought it was all a big joke.

In the 2010s, that feeling had morphed into a common meme about the excesses of “late capitalism,” with my fellow millennials and our Gen Z successors going on social media to take a Karl Marx or Slavok Zizek pose—suggesting that we were living through the waning days of this corrupt economic era, before it collapsed under the weight of its own absurdity and gave way to something either much better—or much worse.

Bernie himself helped spread this idea, and one particular rant during the Vermont Senator’s star-making 2016 presidential campaign captured it perfectly: “You don't necessarily need a choice of 23 underarm spray deodorants or of 18 different pairs of sneakers when children are hungry in this country,” he thundered.

Bernie had a point, I thought at the time: Who needs more than one tube of deodorant, really? Is this, to paraphrase Voltaire’s Candide, really the best of all possible capitalisms? Or is the 400-year-old system of economic exchange finally choking on its own fumes, well-scented but powerless to deliver the world what we really need?

It may be. And I do love the meme, but at the end of 2022, I'm starting to doubt those prophesying that late capitalism will give way to a fundamentally different system. Capitalism is not about to crash and burn, and allow socialism to sprout from its rubble. If anything, this year has been a confirmation, for better or worse, of capitalism’s fundamental strength.

*

Some would say capitalism has already been superseded, and not in a good way. A few years ago, a small but influential group of academics and economists started arguing that capitalism was morphing into something darker, that we were recreating a modern version of the economic oppression of the pre-industrial middle ages.

“Technofeudalism,” they argued, was late capitalism’s dystopian and unexpected sequel. The center of economic power seemed to have moved from Wall Street to Silicon Valley, and the sexiest stocks were the big tech “FAANGs.” The billionaires in control of these firms seemed to own everything from train transportation to news organizations to the entertainment industry. What if technology’s economic and cultural dominance had perverted free-market capitalism and sent the economy from a state of progress to a regress instead? Had we all just become peasants with iPhones?

From Adam Smith through Friedrich Hayek, history’s biggest boosters of the market economy stressed its potential to liberate the individual. But in a technofeudal economy where you can’t afford a house, your every move online is being tracked and monetized, and you don’t really have the choice to opt out of the online sphere, how free can you be?

Meanwhile, the world’s richest men built rockets to shoot themselves, the highest bidders, and William Shatner into space. These are the things that lords of the manor do, not business executives. In Silicon Valley, workers were ferried by company buses to gated campuses, where they were fed and entertained and had their laundry done. These tech behemoths recall nothing so much as giant castles, with whole worlds between their walls.

Of course, capitalists have been making obscene fortunes and sinking them into eccentric projects and world domination schemes for as long as the economic system has existed. The Tesla, SpaceX, and Twitter CEO Elon Musk might be a new version of Louis XIV, but he also recalls the eccentric 20th-century billionaire Howard Hughes.

The gilded-age moguls’ contributions were more tangible and easier to measure, because their products were steel and oil, products you could find on the supermarket shelves or park in your garage, rather than social networks or computing platforms. Have the barons of the modern techno age changed our lives for the better? The decline of living standards and creeping death of the middle class over the last generation argue otherwise.

Meanwhile, the liberal arts are withering away as the brightest young people pile into STEM, en route to jobs where they can code all day while wearing hoodies. Business culture lionizes the tech founder, and the most entrepreneurial move is to launch a startup that will be gobbled up by a tech behemoth with a big pay day based on potential future growth. Meanwhile, the professions that society truly depends on—teachers, nurses, civil engineers—are most prone to the labor shortage that is stretching into its third year.

Proponents of the technofeudalism thesis came from both the left and the right. “In fact, the two ideological poles have all but converged on a shared description of the new reality,” wrote Evgeny Morozov, a left-wing millennial who rose to fame as a critic of the internet’s utopian promises, in April. Morozov, who prefers the term “refeudalisation” to “technofeudalism,” worried in his essay that this reframing of the discussion would distract the left from the struggle against capitalism.

But this may soon be a moot point. In 2022 the sun began to set on technofeudalism.

This year was not only an annus horribilis for stock markets, but also for the lords of the tech world. Mark Zuckerberg lost $100 billion over 12 months (and $11 billion in a single day) en route to a stunning 66% collapse in Meta’s share price. Elon Musk, riding high in the beginning of the year, lost the title of world’s richest man after overpaying spectacularly for Twitter, and now appears to be driving the social media platform off a cliff.

View this interactive chart on Fortune.com

In technofeudalism’s place, a brand of prosaic, rocket ship-free capitalism is coming into focus. Let’s call it retro capitalism, of a type that millennials, lovers of nostalgia, have rarely experienced.

As it turns out, all the tech wealth in the world has been no match for the hoary tools of traditional capitalism, especially central banks: Labor shortages, wonky supply chains, inflation and energy crises are all distinctly retro economic problems that require retro capitalist solutions. The long dominance of risk assets has been laid low by the most aggressive worldwide hiking of interest rates in financial history. Consider the tech-heavy NASDAQ Composite Index, down more than a third after a year of carnage for risk-asset tech stocks.

View this interactive chart on Fortune.com

The end of the era of quantitative easing has exposed technofeudalism as a central banking bubble all along: Tech stocks were inflated by decades of VC speculation that gave rise to even riskier investments—most notably crypto, which shrank by more than two-thirds this year from a peak of $3 trillion-plus.

This is what economists and investors call a “regime change.” The easy money era has ended, pricking what the financial journalist Rana Foroohar has called the “everything bubble.” And with that regime change, my late-capitalism-bemoaning generation will have to pull off a mindset shift. We may not like what comes next.

*

It’s going to be weird, to wake up to a capitalism that recalls another era. We millennials and Gen Zers aren’t going to just be wearing 1990s fashion; our world is retro in more ways than we admit: The economic forces we now see playing out have reshaped society time and time again.

It was a labor shortage in the wake of a pandemic that set the stage for early modern capitalism to emerge. After Europe lost a third to half of its workers to the bubonic plague, the survivors’ ability to command higher wages was hugely unwelcome to their feudal masters. Attempts to suppress wages backfired, as in the case of England’s King Richard II, who was lucky to escape with his life when a peasant army marched all the way to London. The period after the Black Death saw the beginning of government trying to regulate prices, wages, and other aspects of economic life in England, but it would be another three centuries before the country had a central bank that could effectively tackle wage inflation.

In our retro capitalist age, the labor shortage of the last two years has been a major contributor to the inflation that has roared throughout 2022, as understaffed businesses haven’t been able to meet demand efficiently enough, and have passed on the cost of higher wages to their customers.

Labor shortages have spurred widespread social change more recently than the 1300s, too. During World War II, Rosie the Riveter became an iconic stand-in for the American women who entered the workforce, depleted by so many men drafted for the war effort across the Atlantic or Pacific. Rosie and her ilk set the stage for the women’s liberation movement of a generation later and women entering the workforce in huge numbers in the 1970s.

Another modern problem recalls the 1970s: Energy crises and their tendency to upend norms. The last famous energy crisis before Vladimir Putin invaded Ukraine was the 1970s oil crisis, when emboldened Middle Eastern countries clamped down on exports to the U.S., shocking an America that had grown used to a culture built around the automobile. OPEC was responding in part to President Richard Nixon abandoning the gold standard two years earlier, a decision that devalued the dollar and slammed Middle Eastern economies. A decade of “stagflation” ensued, as out-of-control inflation jockeyed with a stagnating economy, immiserating a generation’s prospects. Many experts feel we’re in just such a moment now, again attributable to monetary and fiscal policy, with President Biden coming under criticism for excessive stimulus and Fed Chair Jerome Powell for his perceived lateness on hiking interest rates.

It’s early, but President Biden’s major legislative efforts so far have been, at heart, an old-fashioned jobs program—and a very retro solution to all these problems. Along with the biggest commitment to rebuilding roads and bridges in a generation, efforts to reverse decades of offshoring are gaining steam: The era that saw China become “the world’s factory” is winding down as turmoil in Chinese factories threatens Apple’s “iPhone City.” “Nearshoring” and “friendshoring” are on the rise, in the place of the last several decades’ offshoring, and Biden is doing all he can to hasten it. The economic historian Adam Tooze argued recently that Biden’s trade policy could represent “a profound shift in the positioning of US power towards the world economy”—a pivot away from the trade order in place since the 1990s. The Biden White House argues that its legislation so far will be key to creating a "soft landing" for the economy and avoiding a recession.

*

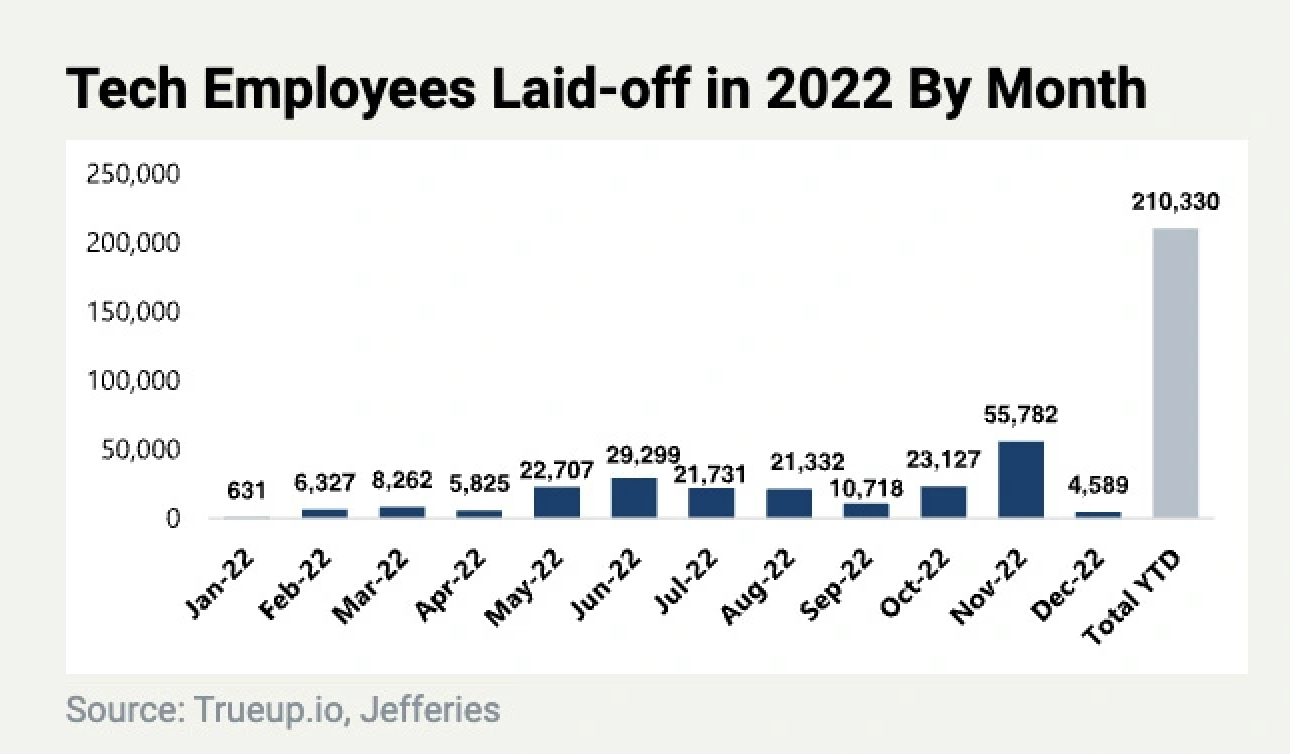

As for those technofeudalists, it’s already becoming clear how painful the fall will be for those who forgot the gravity of capitalism. Massive layoffs are sweeping the tech sector as executives acknowledge they misdiagnosed customer demand, three years into the pandemic.

More proof of the rise of retro capitalism comes from where the layoffs aren’t happening. Other than tech (and a sector that has become overly reliant on it, the media), other sectors are holding up relatively well. Though continued inflation and monetary tightening could inflict wider pain, the less bubbly parts of the economy are proving resilient as the combination of a years-long labor shortage and a continued surge in demand for material goods fuels consistently strong hiring.

The FAANGs are losing ground to good old-fashioned value stocks in the industrial and energy sectors, and investors are being advised to go back to pre-internet strategies. Jon Hirtle, executive chairman of Hirtle Callaghan & Co., an outsourced chief investment officer firm, told my colleague Will Daniel this week that it used to be a good investment strategy to “just buy tech stocks and go on vacation, [but] that’s unlikely to be what we have going forward.” It turns out that stuff, real and tangible stuff, matters in the modern economy, just like in the old one.

To be sure, the tension between a retro style of capitalism and the 21st-century gilded age’s tendency to create medieval levels of wealth disparity likely hasn’t been resolved. The rise of artificial intelligence such as ChatGPT, a bot that answers any question you ask in amusing, often incorrect fashion, is just getting started. And tech companies still control many aspects of our lives, from office communication to dating.

It’s becoming clear that the 2020s aren’t roaring—but they also aren’t a road to serfdom. It’s a rude awakening for my generation, and for anyone who made their living off late capitalism-adjacent sectors for the last two decades. How will we replace the “good jobs” of the 2000s—computer engineer, product manager, VC partner, even crypto trader—in the era of retro capitalism? Former techies used to doubling their salary with equity compensation will have to accept a lower standard of living. We might have to make do with one or two pairs of sneakers, instead of 18.

When I saw my college buddy this month, we digested the World Cup over a few beers and he teased me that I had ended up working at Fortune, brainchild of one of the staunchest pro-business Republicans in history, the magazine mogul Henry Luce. Life is funny, I agreed.

My friend was right about Bernie. He went on to do big things, but the socialist state he helped my generation to imagine is still far off. And what about those feudal lords of the rapidly declining tech era? As long as the Fed is determined to force markets to be rational, they’ll have to live with just being really rich guys. This is not late capitalism or technofeudalism. It’s just life, increasingly looking the way it used to.

Nick Lichtenberg is Fortune's executive editor of news. He was previously deputy editor at Insider and breaking news editor at Bloomberg. He studied drama and Russian history at Syracuse University, but has somehow worked in financial news for over a decade.

The opinions expressed in Fortune.com commentary pieces are solely the views of their authors and do not necessarily reflect the opinions and beliefs of Fortune.