/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)

SoFi Technologies (SOFI) shares plunged as much as 13% on Wednesday, April 29, despite the fintech bank delivering record first-quarter revenue of $1.1 billion, representing a 43% year-over-year increase that comfortably surpassed the consensus estimate of $1.05 billion. Non-adjusted earnings per share of $0.12 came in precisely in line with Wall Street expectations, doubling from $0.06 in the year-ago quarter. Net income more than doubled to $166.7 million, while adjusted EBITDA surged 62% to $340 million, yielding a 31% margin.

The selloff was driven primarily by management’s decision not to raise full-year 2026 guidance despite the first-quarter beat, a move one analyst described as “uncharacteristic” for a company that has historically flowed upside through to its annual outlook. SoFi maintained its full-year adjusted net revenue target of approximately $4.655 billion, adjusted EBITDA of roughly $1.6 billion, and adjusted EPS of about $0.60. The full-year revenue target barely exceeded the analyst consensus of $4.651 billion, providing no meaningful upside catalyst. CEO Anthony Noto acknowledged that the lack of a guidance raise was likely the primary driver of the stock’s decline, noting that markets tend to reward acceleration rather than mere reaffirmation.

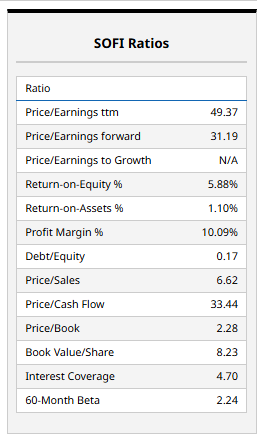

Compounding investor unease, second-quarter guidance pointed to revenue growth of approximately 30%, a notable deceleration from the 41% adjusted growth posted in Q1. For a stock that has been valued on a high-growth trajectory, this moderation effectively functions as a de-rating signal. The forward P/E ratio near 49x prior to earnings left no margin for execution shortfalls, and even a perception of slowing momentum was enough to trigger aggressive selling.

Beneath the headline numbers, specific business segments revealed concerning divergences. The Technology Platform segment, which houses the Galileo banking-as-a-service infrastructure, saw revenue decline 27% year-over-year to $75.1 million following the full departure of key client Chime before the end of 2025. The financial services segment generated $428.5 million, up 41% but missing consensus expectations of approximately $474 million. Total fee-based revenue of $387 million also fell short of the $405 million analysts had anticipated.

The Loan Platform Business, which has become an increasingly important capital-light revenue stream, showed notable weakness. LPB originations of roughly $3 billion fell well short of consensus estimates near $3.7 billion, and LPB fees of approximately $141 million missed one analyst’s estimate of $189 million. Management stated this was a deliberate decision to retain more originations on the balance sheet, which boosted net interest income but raised fresh concerns about credit exposure. The LPB take rate, including referral fees, declined from 5.16% in the prior quarter to 4.61%, adding to skepticism about the sustainability of this revenue source through an entire credit cycle.

On the positive side, SoFi’s core growth metrics remained impressive. The company added a record 1.1 million new members during the quarter, bringing total membership to 14.7 million, up 35% year-over-year. Total products climbed 39% to 22.2 million, with 43% of new product additions coming from existing members, demonstrating effective cross-selling. Loan originations hit an all-time high of $12.2 billion, with personal loans at $8.3 billion, student loans more than doubling to $2.6 billion, and home loan originations reaching $1.2 billion. Total deposits expanded by $2.7 billion during the quarter to $40.2 billion.

Credit quality presented a mixed picture. The overall net charge-off ratio improved to 2.07% from 2.37% a year ago, but personal loan charge-offs ticked higher sequentially and student loan charge-offs rose 18 basis points year-over-year. With personal loan balances expanding at a 51% clip, bears worry that SoFi is extending credit aggressively into a potentially softening consumer environment. The March short report from Muddy Waters, which alleged aggressive accounting and off-balance-sheet structures to mask credit risk, continues to hang over investor sentiment despite SoFi’s denial.

The broader market context amplified the negative reaction. SoFi shares had already fallen approximately 30% year-to-date heading into the report, and options pricing had implied a roughly 10% post-earnings move in either direction, suggesting the market was braced for volatility. The stock’s beta of 2.24 means macroeconomic uncertainty, including rising oil prices above $100 per barrel and the Federal Reserve’s rate decision later today, weighs disproportionately on shares. Noto noted that original full-year guidance assumed two Fed rate cuts, whereas the maintained guidance now assumes zero cuts, effectively absorbing a meaningful headwind without reducing targets.

SoFi is increasingly caught between two narratives: a high-growth fintech story that commands premium multiples and an evolving financial institution entering a more mature phase where growth rates naturally moderate. The market’s violent reaction to in-line earnings and unchanged guidance underscores that investors priced in continued acceleration, not stabilization, and the transition from hyper-growth to durable profitability remains a painful repricing process.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.