Often, one of a client’s biggest goals is making sure their spouse is protected if they pass away. Choosing the best distribution option for your pension when you retire is an important decision.

Many people think they should take the survivor option to make sure their spouse is left in the best financial position. However, if you get creative with your planning, you may be able to create a better outcome than just taking the survivor option.

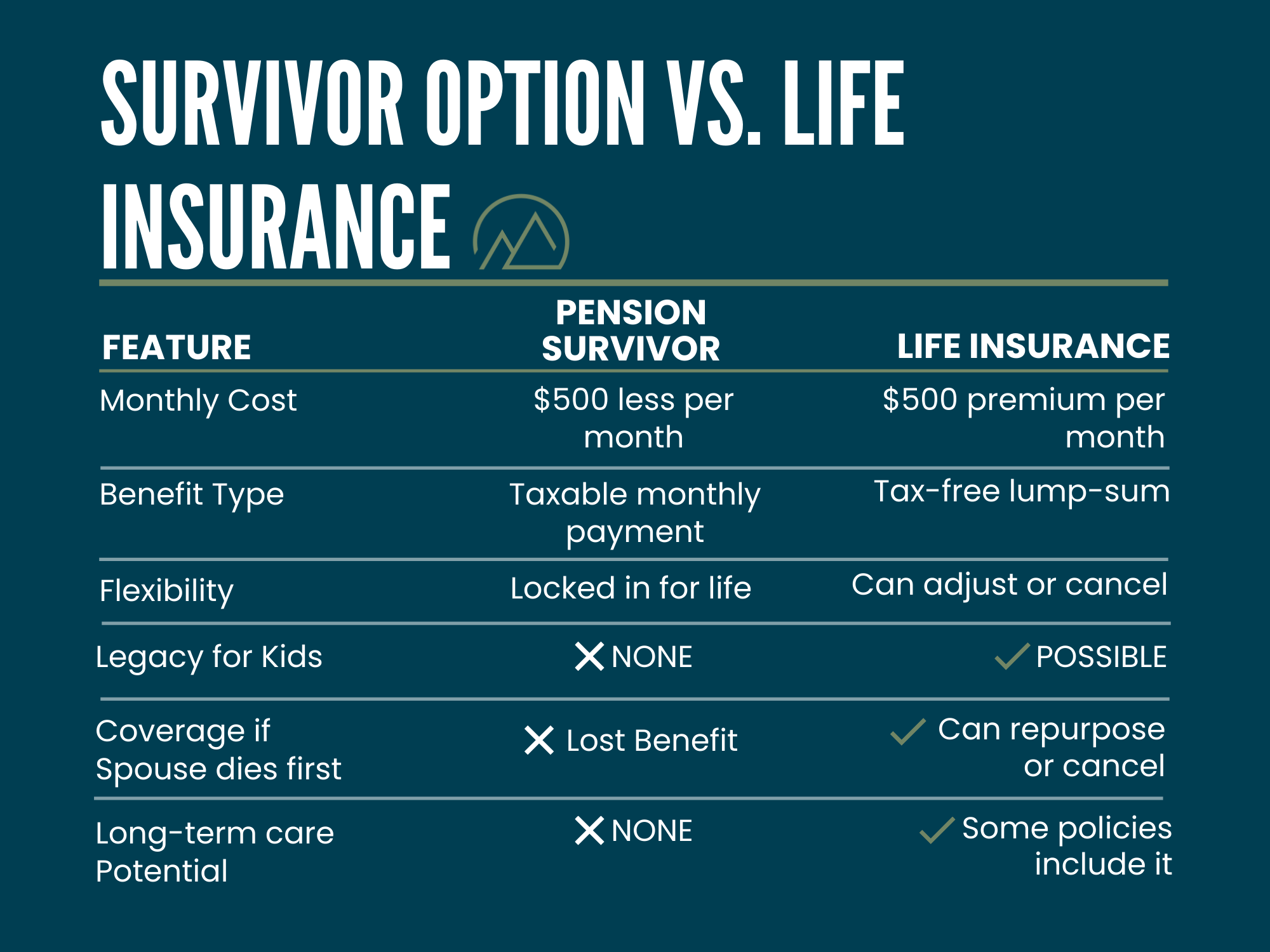

Taking the survivor option means you have to pay for that benefit, which in turn means that you don’t get as much money from your pension while you are alive.

For example, at Peak Retirement Planning, where I am the CEO, we had a client whose pension paid $5,000 a month for their lifetime. If they selected the survivor option (which would pay the spouse 50% of their pension for life), they would give up 10% of their pension going forward.

This means $500 per month would be deducted from their benefit, and they would receive $4,500 per month. When they pass away, the spouse will receive $2,500 a month for the rest of their life.

It may not be obvious whether this is a good or bad option without digging into the numbers. I don’t know about you, but $500 a month seems very expensive. Just think what you could do with an extra $500 a month in retirement.

Since the No. 1 goal of many people reading this article is for their spouse to be taken care of, let’s see what other protection options there may be for that $500 a month.

Consider life insurance

Some clients we work with consider replacing this survivor option with life insurance. What type of life insurance could you get for $500 a month? Someone who is 60 years old, depending on health, could get a permanent life insurance policy with a death benefit of about $350,000.

This means that if you passed away, $350,000 would go to your spouse at any time as long as you continued to pay on the policy. Or you could get around $1 million of death benefit with a 20-year term life insurance policy. This would last for 20 years, then go away, which is why you get more benefit for what you pay.

Typically, we would look at utilizing a combination of both to ensure the spouse has enough to live on if something were to happen.

How much does your spouse need to live the retirement they want? That is a determination you would need to make for yourself, but I can tell you that, typically, the life insurance benefit could be nearly as much as, if not more than, the $2,500 a month benefit they could have gotten by taking the pension by finding the right combination of term/permanent life insurance coverage.

The life insurance benefit would also be tax-free, while the pension payment would be taxable each year — and it could be taxed at the single rate vs the married rate, which is less advantageous for your spouse. (This is known as the “widow’s penalty.”)

An additional benefit is that if your spouse passes away first, you could now leave this insurance money to your kids tax-free. Also, many life insurance policies have a long-term care option that allows you to accelerate the death benefit if you were to need that care.

If you purchase a permanent life insurance policy, many have a cash value buildup that you could access and then cancel the policy if your spouse passes away first — meaning that what you paid into the policy is not wasted.

Keep in mind that you must be insurable to take advantage of this option, and the cost will depend on how healthy you are. For those who are younger and healthier, this can be a viable option.

I would suggest working with a financial planner who specializes in comprehensive planning — including pension and life insurance planning — to help you run the numbers to see if this is a good option for you.

If it is, they can help you find the best vehicle to fit your situation and goals. (I wrote a book for those with pensions, The 2% Club, that you can request for free here.)

Another concern to keep in mind

This type of planning can also be beneficial for those who may be concerned about the long-term viability of their pension. In recent years, pensions have shown signs of stress as people are living longer and there are fewer people paying into them. As a result, many pensions are underfunded.

Exploring options beyond your pension could mean more control for your retirement.

It could also be beneficial not to choose the pension survivor option if your spouse is older than you or is not expected to live as long as you. The bottom line: You don’t want to pay for something you may never benefit from.

If you decide not to take the pension survivor option, it’s very important that you have a plan in place to make sure your spouse is taken care of in the event that you pass away first.

If you’re not eligible for life insurance, or you don’t have enough investments to self-insure, then in some cases, I would counsel you to take the pension survivor option to ensure your spouse is covered, even if that means not maximizing your pension benefit. In this case, the risks outweigh the potential benefits.

Related Content

- This Changes Your Social Security Decision (Especially if You're in the 2% Club)

- Many Retirees With a Pension and $1 Million-Plus Do These 7 Things (and Regret It Later)

- 7 Times to Dip Into Your Roth IRA if You Have a Pension (and When to Leave It Alone)

- If You Have a Pension, Smart Tax Planning Should Start Now

- Will You Pay Higher Taxes in Retirement?

This article was written by and presents the views of our contributing adviser, not the Kiplinger editorial staff. You can check adviser records with the SEC or with FINRA.