/Booking%20Holdings%20Inc%20office%20by-tupungato%20via%20iStock.jpg)

Stock splits have quietly come back into focus on Wall Street over the past year or so, as a mix of mega-cap leaders and long-term compounders use them to lower share prices on paper and attract more everyday investors. In 2024, more than a dozen brand-name companies, including Walmart (WMT) and several AI-driven names like Nvidia (NVDA) and Broadcom (AVGO), either completed or announced forward splits. 2025’s first big split was O’Reilly Automotive’s (ORLY) record 15‑for‑1 move, which was meant to make shares easier to own for employees and regular investors.

Booking (BKNG) now fits right into this stock-split story. The company has approved a 25‑for‑1 forward split, effective April 2, that will take BKNG stock’s share price from the roughly $4,000 range to a more manageable level for investors who like holding whole shares instead of fractions. With institutional buying recently topping selling by nearly 3‑to‑1 in dollar terms, the split could turn improving sentiment into higher trading activity from both big funds and individual investors.

So, with stock splits back in vogue and Booking opting for one of the market’s most dramatic forward splits in years, is this about to become one of the most compelling ways to play the travel and experiences boom? Let’s take a closer look.

Booking’s Financial Scoreboard

Booking runs a large online travel business, connecting people with hotels, homes, flights, cars, and experiences, and taking a cut of each booking that goes through its platforms.

Over the past 52 weeks, BKNG stock is down about 17%, and off by roughly 22% year-to-date (YTD). That has pulled the valuation back to more reasonable levels, with BKNG stock sporting a forward price-to-earnings multiple of about 14.4 times compared to roughly 16 times for the broader sector.

Booking has a market capitalization of roughly $128.8 billion and pays an annual dividend of $38.40 per share, which works out to a yield of about 0.94% at the current price. The company paid its most recent $9.60 quarterly dividend in December, has only one year of increases so far, and pays on a quarterly schedule, but it does so with a conservative forward payout ratio of around 16.7%. That leaves plenty of room for Booking to keep raising the dividend without holding back growth.

In the fourth quarter of 2025, revenue was $6.35 billion, up 16% year-over-year (YOY) and above the $6.13 billion analysts expected, pointing to steady travel demand and solid take rates. Adjusted EPS was $48.80, essentially in line with forecasts. Meanwhile, adjusted EBITDA of $2.2 billion beat consensus estimates by almost 4% with a 34.6% margin, showing that Booking is turning extra revenue into profit efficiently.

Operating margin stayed strong at 32%, free cash flow margin rose to 22.3% from 15.2% in the prior quarter, and room nights booked reached 285 million, up 24 million YOY. Together, these figures paint a picture of a platform still adding volume and generating cash even as the share price has cooled.

The Growth Engines Powering Booking’s Next Chapter

Booking’s deeper direct connection with Navan (NAVN) is a straightforward example of how the company is leaning into partnerships and technology to keep growth moving while BKNG stock takes a breather. By tying more closely into Navan’s all‑in‑one business travel, payments, and expense platform, Booking.com can put a much wider range of global lodging options — along with better negotiated rates — directly in front of corporate travelers and their finance teams. The upgraded API link matters most in “off‑the‑beaten‑path” locations where Booking’s coverage is strongest, helping companies keep travel policies on track while still offering more choice and lower accommodation costs.

The same basic idea is behind the partnership with Spotnana. A direct integration with Booking.com’s latest API gives Spotnana customers and TMC partners full access to Booking’s global inventory and corporate‑style rates, in a user-friendly setup that supports self-service changes and strong agent backing. That makes Booking’s content more embedded and harder to replace as the corporate travel tech stack keeps getting updated.

On top of these distribution gains, management is pushing a multi‑year plan to win more share in the U.S. and Asia by using brands like Agoda and Booking.com, building out flights, attractions, and fintech, and growing the Genius loyalty program and alternative accommodations. A Transformation Program targeting $500 million to $550 million in annual run‑rate cost savings is meant to fund these investments in AI, fintech, and international expansion from within, while still lifting adjusted EBITDA margins by about 50 basis points as Booking moves through 2026.

What Does Wall Street See for BKNG Stock?

For the current March quarter, the average EPS estimate sits at $29.50 versus $24.81 a year ago, which points to 19% YOY growth. Meanwhile, EPS for the June 2026 quarter is expected to come in at $68.43 compared to $55.40 last year, a nearly 24% increase. For the full fiscal year, analysts are modeling for EPS of $267.32, up from $228.06, which works out to 17% growth on a YOY basis.

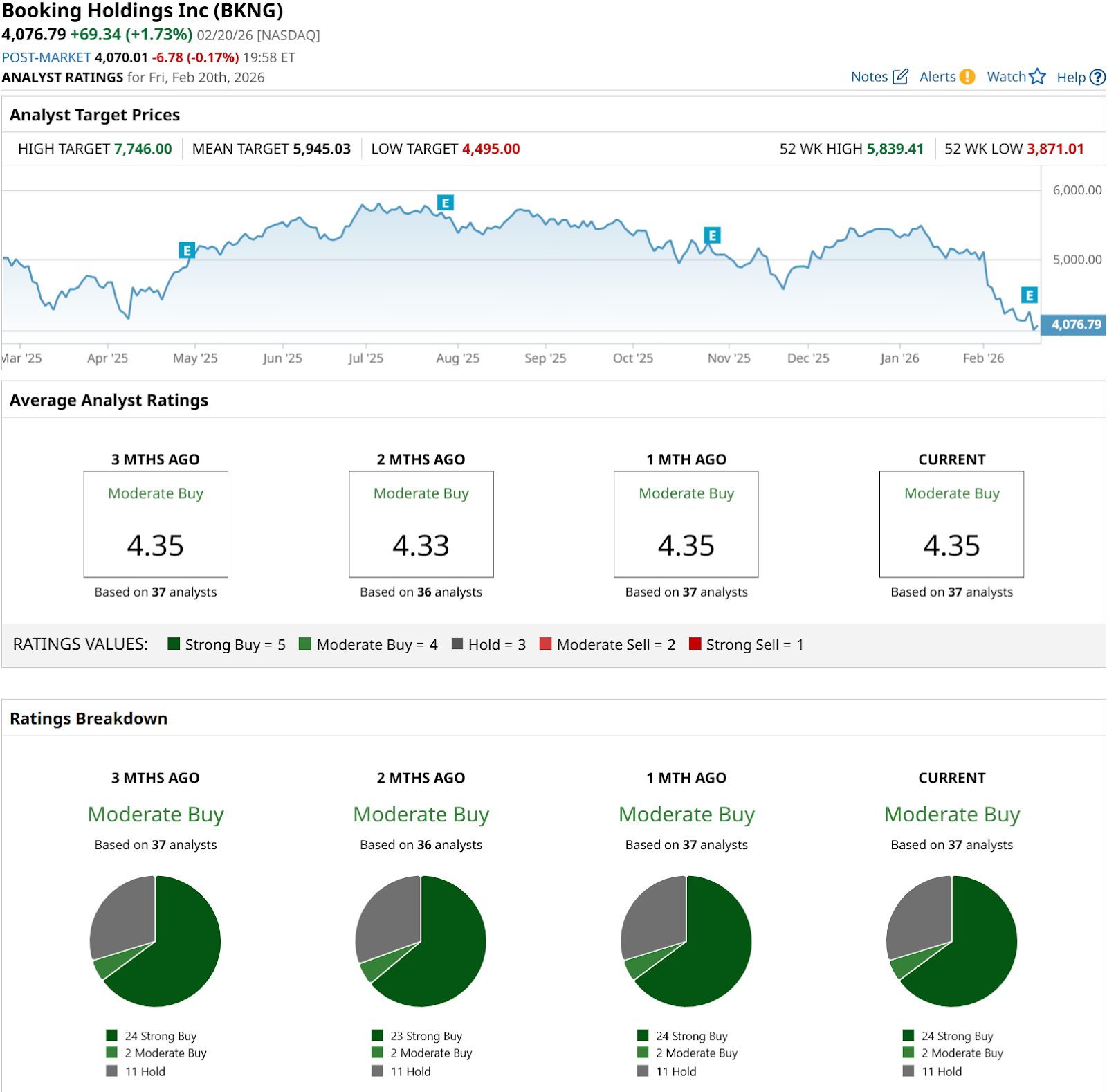

Looking at individual calls, the tone is similar. On Feb. 19, Wedbush analyst Scott Devitt kept his “Buy” rating and $5,300 target, implying roughly 27% potential upside. Back in October, BTIG analyst Jake Fuller also stuck with a “Buy” and held his $6,250 target, signaling confidence that Booking’s work in AI, cost efficiency, and operating leverage can keep driving value well beyond the split.

All of this feeds into the broader view. Analysts rate BKNG stock as a consensus “Strong Buy.” The average price target of $5,781.58 suggests about 39% potential upside from here.

Conclusion

If you’re looking for a clean answer, Booking looks like a “yes, but know what you’re signing up for” ahead of the 25‑for‑1 split. BKNG stock has already reset hard, the business is still compounding double‑digit earnings, and Wall Street’s average target implies roughly 39% possible upside from here. That's not the profile of a mature name just using a split as a gimmick. In the near term, expect volatility around macro headlines and travel sentiment, but directionally, the setup favors a grind higher over the next 12 to 24 months as institutional demand, improving fundamentals, and new retail access all intersect on the other side of April 2.