SUMMARY

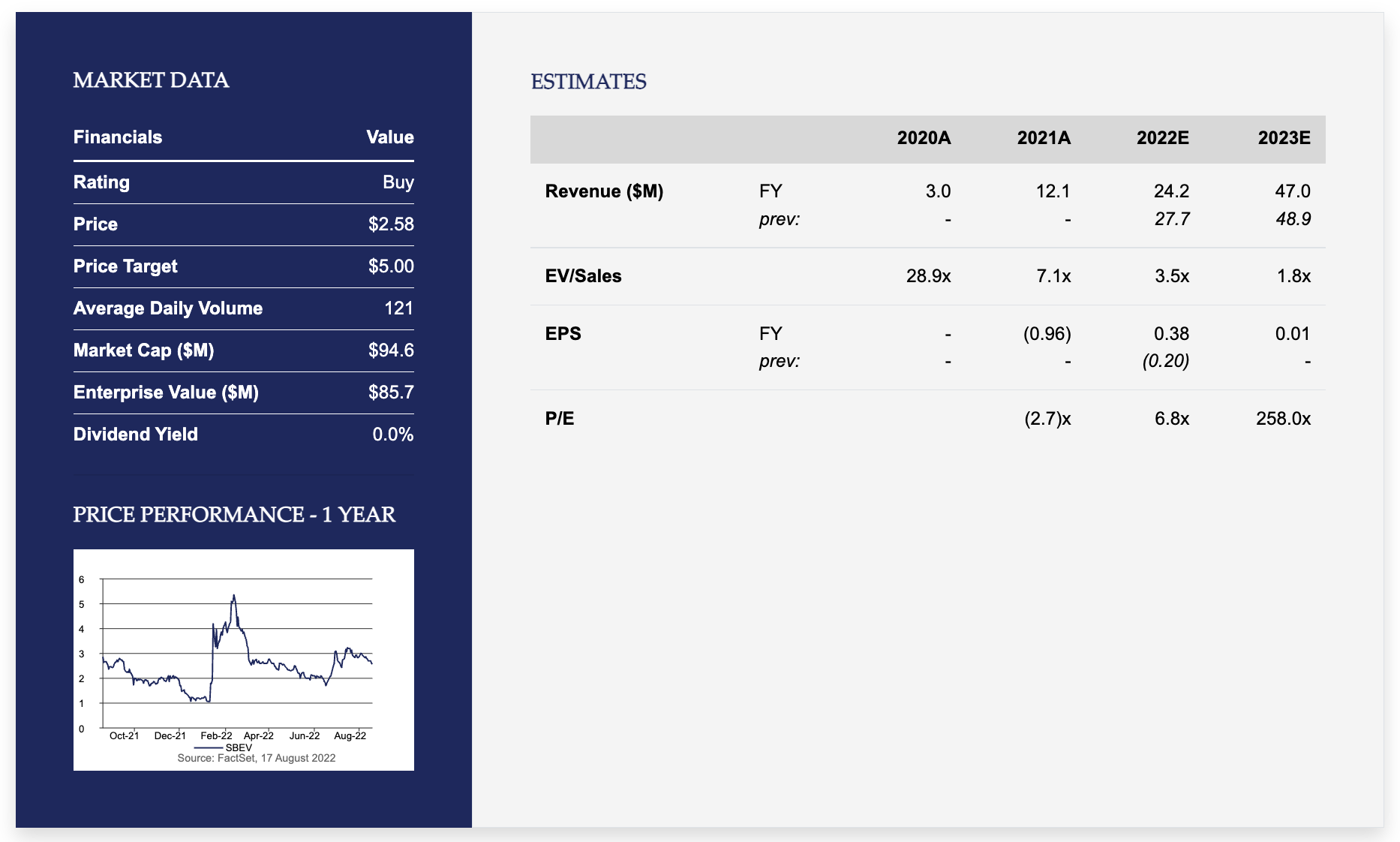

2Q Results. Splash delivered solid results, with net revenue of $4.5M up 36.8% y/y and 14.6% sequentially. This was driven by its online platform, Qplash as well as the continued rollout of TapOut. Gross margins of 15% contracted 610 bps from a quarter ago due to a handful of one-time items. However, we would expect margin to meaningfully rebounded through the remainder of the year. Earnings per share came in at a loss of $0.15 and the company ended the quarter with $4.2M of cash. During the quarter, Splash brought on Ron Wall as CFO, who we believe is an important strategic hire. Mr. Wall brings extensive expertise as a spirits executive, having spent the prior 13 years at privately held William Grant and Sons as CFO.

Outlook. Management is continuing its aggressive expansion into wholesale, having recently announced a plethora of new relationships, including 7-11 and Circle-K. We believe that the push into the convenience-store chains is a natural evolution of the strategy and bodes well across the Splash portfolio.

Additionally, the company recently announced that it will be acquiring an 80% stake in Pulpoloco, which historically it merely had the distribution rights for. We believe that this is an import piece of the puzzle for the Splash portfolio given the dramatic increase in the demand for single-serve cocktails, coupled with the highly unique and innovative CartoCan format.

We have made modest tweaks to our estimates in the back half of this year and leave 2023 largely unchanged. We continue to be bullish on the asset light, portfolio approach that Splash is executing on and believe that they are on the precipice of material acceleration in sales as wholesale wins begin to bare fruit. Our price target of $5, which is based on 4x 2023 ev/sales remains unchanged.

Key Risks. Splash is still in the early innings of its wholesale rollout strategy, and is attempting to take share in a highly competitive field against incumbents who have far more resources than it does. Historically the company has relied on the capital markets to fund losses and may need to continue doing so in the future. We encourage investors to review the company's filings with the SEC in conjunction with this report.

DISCLOSURES

Analyst Certification

I, Ben Piggott, certify that all of the views expressed in this research report accurately reflect my personal views about the subject security(ies) and subject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in this research report.

Company-Specific Disclosures

EF Hutton, division of Benchmark Investments, LLC managed or co-managed a public offering of securities for Splash Beverage Group, Inc. during the past 12 months.

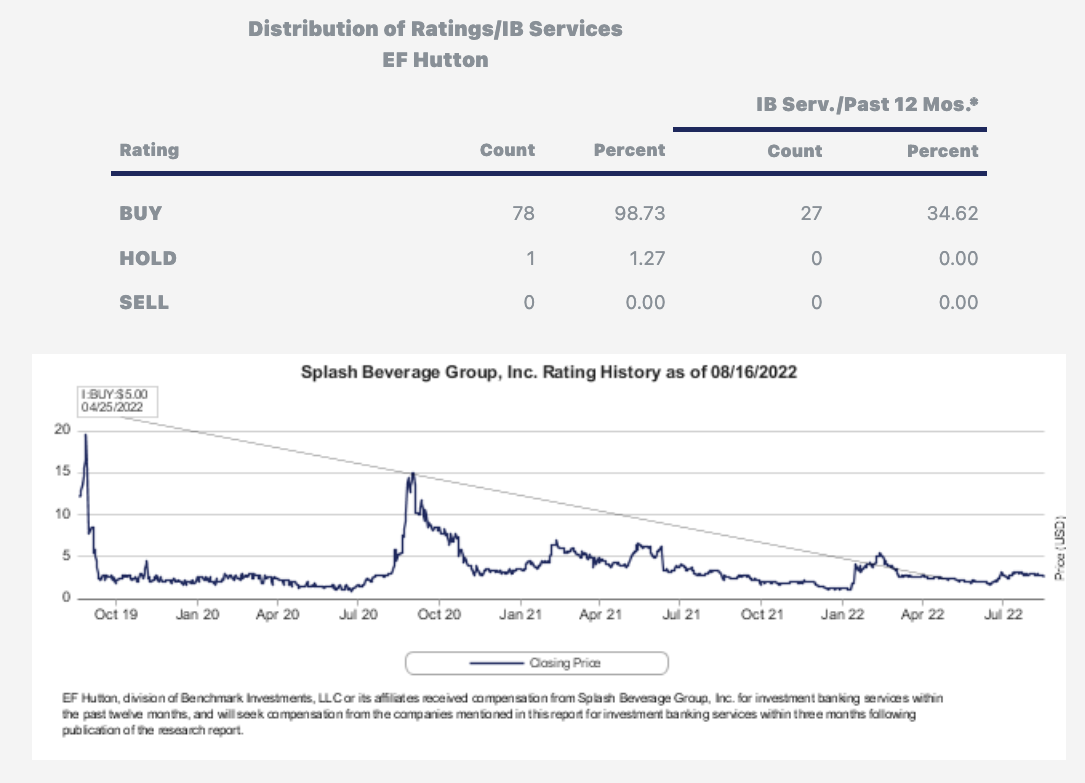

EF Hutton, division of Benchmark Investments, LLC or its affiliates received compensation from Splash Beverage Group, Inc. for investment banking services within the past twelve months, and will seek compensation from the companies mentioned in this report for investment banking services within three months following publication of the research report.

General Disclosure

This report has been produced by EF Hutton, division of Benchmark Investments, LLC and is for informational purposes only. It does not constitute solicitation of the sale or purchase of securities or other investments. The information contained herein is derived from sources that are believed to be reliable. Prices, numbers, and similar data contained herein include past results, estimates, and forecasts, all of which may differ from actual data. These prices, numbers, and similar data may also change without prior notification. This research report does not guarantee future performance, and the information contained herein should be used solely at the discretion and responsibility of the client. Neither EF Hutton nor its affiliates accept any liability or responsibility for any results in connection with the use of such information. This research report does not consider specific financial situations, needs, or investment objectives of any client, and it is not intended to provide tax, legal, or investment advice. Clients are responsible for making final investment decisions and should do so after a careful examination of all documentation delivered prior to execution, explanatory documents pertaining to listed securities, etc., prospectuses, and other relevant documents. EF Hutton and its affiliates may make investment decisions based on this research report. In addition, EF Hutton and its affiliates, as well as employees, may trade in the securities mentioned in this research report, their derivatives, or other securities issued by the same issuing companies in this research report. This research report is distributed by EF Hutton and/or its affiliates. The information contained herein is for client use only.

EF Hutton holds the copyright on this research report. Any unauthorized use or transmission of any part of this research report for any reason, whether by digital, mechanical, or any other means, is prohibited. If you have any questions, please contact your sales representative. Additional information is available upon request.

Certain company names, product and/or service names that appear in this research report are trademarks or registered trademarks of EF Hutton or other companies mentioned in the report.

Copyright 2022 EF HUTTON, division of Benchmark Investments, LLC.