Western Digital Corporation (WDC) is a San Jose, California-based data storage specialist that, following the landmark February 2025 spin-off of its flash memory business into the independent SanDisk Corporation (SNDK), now operates as a pure-play, laser-focused hard disk drive (HDD) company. Post-split, the company serves clients like Amazon (AMZN), Alphabet (GOOG) (GOOGL), and Microsoft (MSFT), making it one of the most direct beneficiaries of the global AI infrastructure buildout.

By shedding the volatile flash business and doubling down on HDD expertise, WDC has transformed from a debt-laden conglomerate into a high-margin leader of the AI data economy, with a product roadmap extending beyond 100-terabyte drives and a strategic presence at COMPUTEX 2026 reinforcing its message that AI infrastructure is fundamentally a data system, not just a computing system.

Western Digital on a Bull Run

WDC has delivered a staggering 795% total return over the past 12 months, with a year-to-date (YTD) total return of approximately 190% in 2026, making it one of the two best-performing stocks in the entire S&P 500 ($SPX), trailing only its own spinoff, SanDisk. The stock surged from an April 2025 low of $28.83 to an all-time high of $602, a 1,550% gain fueled by AI storage demand, margin expansion, and spinoff value unlock.

Against the S&P 500 Information Technology Index ($SRIT), WDC has dramatically outpaced the Technology Select Sector SPDR Fund's returns over both a 52-week and YTD basis, cementing its status as the defining AI storage momentum trade of the current market cycle.

Western Digital Posts Strong Results

Western Digital reported Q3 FY2026 revenue of $3.34 billion, up 45% year-over-year (YoY), beating the analyst consensus estimate of $3.23 billion, while non-GAAP diluted EPS of $2.72 surpassed the Street estimate of $2.34 by approximately 16%, with revenue, gross margin, and EPS all coming in above the high end of guidance. Cloud segment revenue drove the outperformance, with 222 exabytes delivered to customers, up 34% YoY, including over 4.1 million drives of its latest-generation EPMR technology with capacity points up to 32 terabytes.

Non-GAAP gross margin surged to 50.5%, crossing the 50% threshold for the first time, up 1,040 basis points YoY and 440 basis points sequentially, while operating income jumped 106% YoY to $1.3 billion at a 38.6% operating margin. Free cash flow reached $978 million, with cash flow from operations hitting $1.12 billion. The company also raised its quarterly dividend by 20% to $0.15 per share, reflecting strong balance sheet health and management's confidence in the durability of the AI HDD supercycle.

For Q4 FY2026, management guided revenue of $3.65 billion plus or minus $100 million, implying 40% YoY growth at the midpoint, with non-GAAP gross margins guided to 51%–52% and non-GAAP EPS of $3.25 plus or minus $0.15. CEO Irving Tan stated, "As we move forward, we are encouraged by our momentum and remain confident in our ability to deliver sustainable revenue growth, expand gross and operating margins, and create long-term value for our shareholders." The company's HAMR technology is now in customer qualification with four customers, with 44-terabyte HAMR and 40-terabyte EPMR drives in the pipeline, and a product roadmap extending beyond 100 terabytes, positioning WDC at the frontier of next-generation AI storage infrastructure.

Mizuho Upgrades Western Digital

Mizuho raised its price target on Western Digital to $685 from $550, signaling an upside of 35% while maintaining its “Outperform” rating, as analyst Vijay Rakesh highlighted AI as the primary force driving a structural supply-demand imbalance across the memory and storage markets. Within the HDD segment, Mizuho sees accelerating demand from AI infrastructure buildouts, including surging Google TPU, Meta (META) MTIA, and OpenAI ASIC ramps, as directly positive for storage attach rates at Western Digital and peers.

The firm estimates total NAND demand growing 18% YoY in both 2026 and 2027, with no significant new supply coming online until 2028, a dynamic that reinforces WDC's pricing power and margin expansion runway well into the next upcycle.

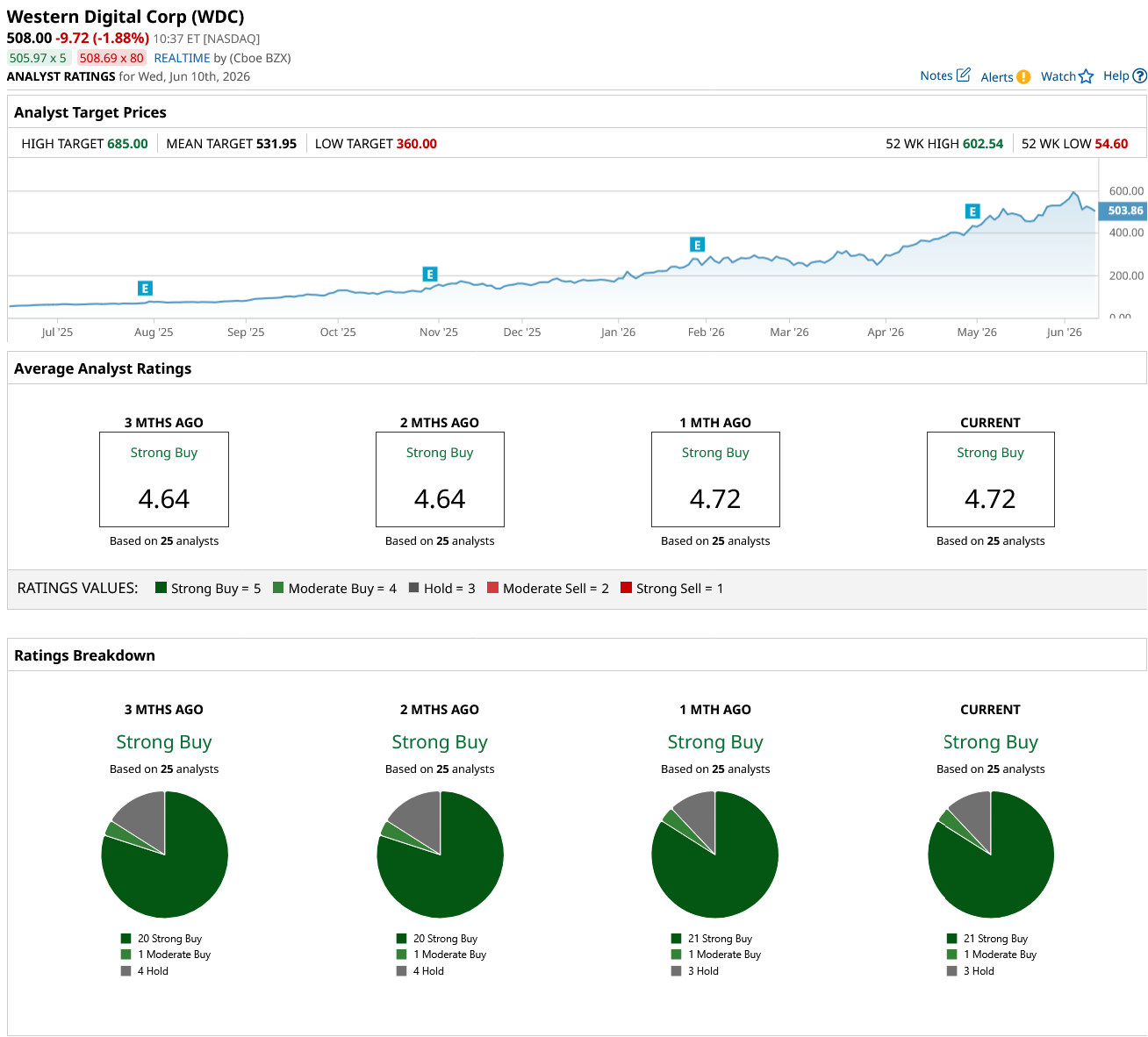

Should You Get WDC Stock?

With Mizuho's $685 price target and a structural AI storage supply-demand imbalance expected to persist well into 2028, Western Digital's earnings runway remains compelling. Wall Street's consensus is firmly bullish. WDC carries a "Strong Buy" rating across 25 analyst ratings, comprising 21 "Strong Buy," one "Moderate Buy," and three "Hold," with a mean price target of $531.95, implying approximately 5% upside from current levels.

The modest consensus upside reflects a stock that has already delivered extraordinary returns, but for investors with conviction in the AI HDD supercycle, WDC's expanding margins, record free cash flow, and HAMR technology roadmap make it a high-quality hold at current levels.