/Micron%20Technology%20Inc_logo%20and%20website-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)

Micron (MU) stock continues its upward trajectory, driven by strong demand drivers and favorable industry dynamics. The company is witnessing strong demand for its high-capacity memory solutions driven by the rapid buildout of AI infrastructure.

Beyond demand strength, supply-side constraints across the memory industry have amplified Micron’s earnings potential. Tight supply conditions are driving prices higher and translating into expanding margins and earnings.

Looking ahead, elevated demand for memory chips will benefit advanced memory and storage solutions providers for AI infrastructure buildout, including Micron. This will likely support the ongoing rally in MU stock.

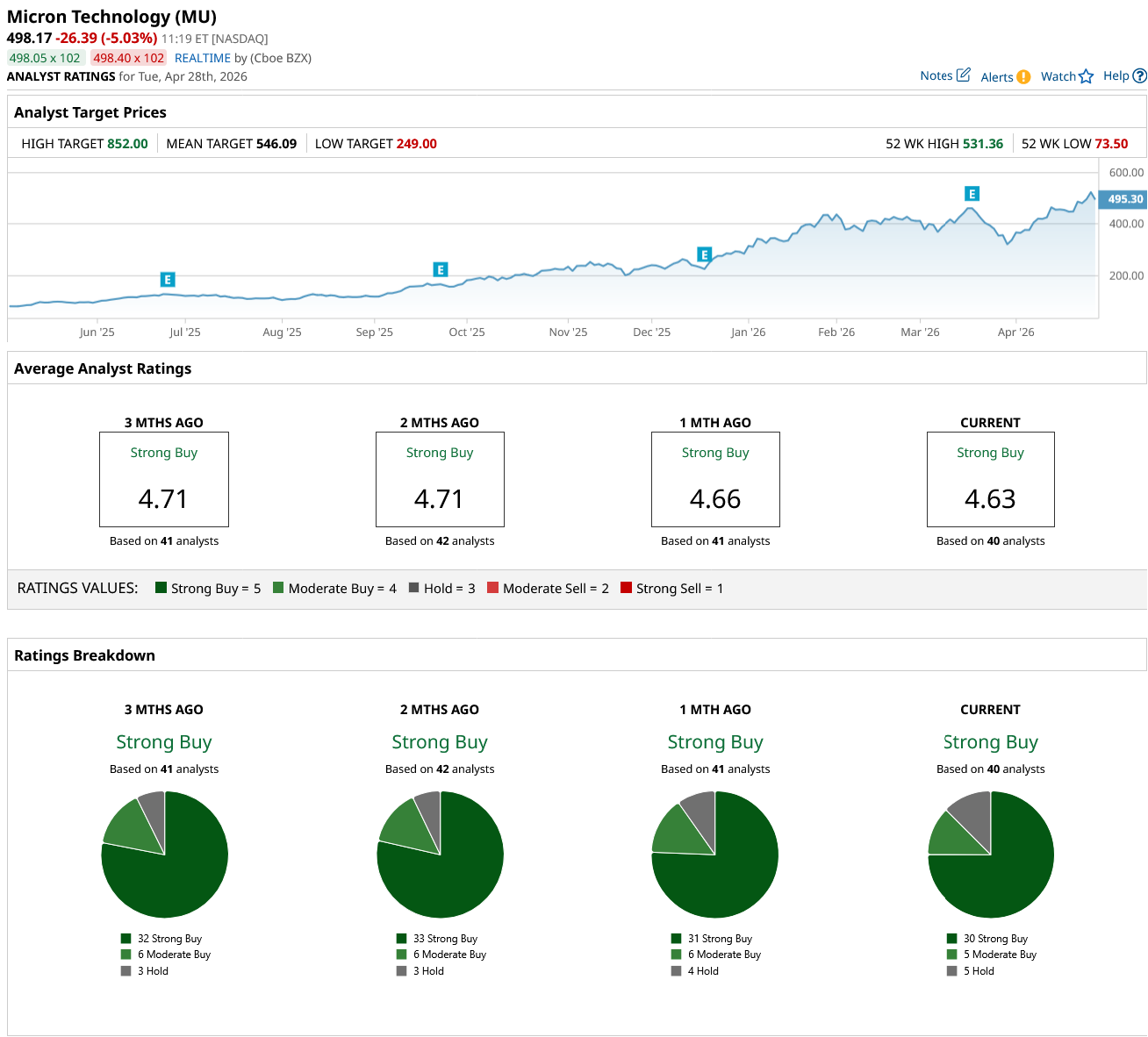

Notably, MU stock has rallied more than 530% over the past year. The current average price target of $546.09 appears conservative, given the expected upward revision to analysts’ earnings forecasts driven by strong pricing and demand trends. This implies that the stock has more room to run.

At least one analyst projects that Micron stock could reach $852 within the next 12 months, implying significant upside potential of about 62% from its recent closing price of $524.56.

Micron to Deliver Massive Growth in Q3

Micron is well-positioned to sustain the exceptional momentum in its business in Q3. Notably, in fiscal Q2, the company delivered revenue of $23.9 billion, which nearly tripled year-over-year (YoY). Moreover, the company witnessed strong performance across DRAM, NAND, and high-bandwidth memory (HBM) products.

Management’s guidance for Q3 suggests continued acceleration in its revenue, margins, and EPS growth rate. Revenue is projected to reach $33.5 billion in Q3, implying a sequential increase of around 40% and a YoY surge of roughly 260%. Micron’s management highlighted that the single-quarter revenue forecast is expected to exceed Micron’s full-year revenue in any fiscal year before 2025.

The robust end-market demand and persistent industry supply constraints, both of which are sustaining elevated pricing across memory products, are likely to support Micron’s growth.

Micron’s data center segment will likely deliver solid growth, supported by strong demand for server deployments and a favorable product mix weighted toward high-value solutions such as HBM, high-capacity server DRAM modules, and enterprise-grade SSDs.

Its profitability is also set to expand meaningfully. Micron expects gross margins to hit 81% in Q3, a sharp increase from 39% in the year-ago period and an improvement over the already strong 74.9% reported in Q2. This margin expansion will continue to be driven by higher average selling prices, ongoing cost efficiencies, and improved product mix. As a result, Micron’s earnings are expected to mark significant growth. Micron projects Q3 earnings of $19.15 per share, compared to $1.91 a year earlier.

Looking beyond the near term, Micron’s outlook remains strong and will likely benefit from sustained demand growth, an expanding total addressable market, supportive pricing conditions, and continued investment in advanced memory technologies.

Micron Stock’s Valuation Supports Further Upside

While MU stock has gained significantly in value, its valuation still looks compelling, leaving room for further upside. The stock currently trades at 8.4 times forward earnings, which appears attractive relative to its projected earnings trajectory. Moreover, Micron’s valuation is appealing compared to the broader semiconductor peer group, benefiting from elevated memory demand.

Analysts’ consensus estimates indicate that Micron’s earnings could surge by more than 651% in 2026, followed by an additional 69.4% increase in fiscal 2027. The rapid earnings expansion and a relatively low valuation multiple suggest the MU stock uptrend will likely sustain.

Wall Street analysts maintain a “Strong Buy” consensus on the stock, reflecting confidence in Micron’s ability to capitalize on sustained demand for memory products.

Will MU Stock Hit $852?

With accelerating revenue, expanding margins, and a compelling valuation, MU stock has further upside potential. Moreover, if Micron can sustain its impressive growth and continue to improve profitability, investor confidence could strengthen significantly, and the stock could hit $852.