/Marriott%20International%2C%20Inc_%20hotel%20by-%20yujie%20chen%20via%20iStock.jpg)

Marriott International, Inc. (MAR), headquartered in Bethesda, Maryland, has grown into one of the world’s largest hospitality giants, with a market capitalization of around $93.1 billion. The company operates and franchises more than 9,900 hotels and lodging properties across 143 countries and territories, giving it one of the broadest global footprints in the travel industry.

Marriott’s strength comes from the sheer breadth of its portfolio. The company spans everything from luxury brands like The Ritz-Carlton, JW Marriott, and Bulgari Hotels & Resorts to more affordable and business-focused names such as Courtyard by Marriott and Fairfield Inn & Suites. Beyond hotels, Marriott also has a growing presence in extended-stay, residential, and timeshare properties, helping the company serve travelers across nearly every category of the global lodging market.

Shares of the hotel giant have outperformed the broader market over the past year. MAR stock has returned 31.5% over the past 52 weeks, beating the broader S&P 500 Index ($SPX), which has gained 24.3% over the same period. Moreover, MAR’s momentum also stayed strong in 2026, climbing 15.8% on a year-to-date (YTD) basis compared to the SPX’s 8.1% surge.

The outperformance looks even stronger against the AdvisorShares Hotel ETF (BEDZ). While the hotel-focused ETF is up 8.4% over the past year and only marginally higher in 2026, Marriott has continued pulling ahead as investors keep favoring global travel and premium hospitality names.

A big reason behind Marriott International’s outperformance is that the company sits right in the sweet spot of today’s travel market. Global travel demand remains strong, but luxury and premium travelers are really driving the industry right now, and those customers are still spending even as broader consumer budgets tighten. That trend has helped Marriott pull ahead of both the broader market and many hotel peers, recently sending the stock to an all-time high of $380 on April.

The momentum became even clearer after Marriott’s stronger-than-expected Q1 2026 results on May 6. Worldwide RevPAR rose 4.2%, showing broad-based demand across the company’s portfolio. Revenue climbed 6.2% year over year (YOY) to $6.65 billion, while adjusted EPS reached $2.72. CEO Anthony Capuano also pointed to continued strength in luxury properties and improving trends in select-service hotels.

Growth is not just coming from existing hotels either. Marriott added nearly 15,900 net rooms during the quarter, growing total rooms 4.5% annually. Its development pipeline also hit a record, reaching more than 4,100 properties and nearly 618,000 rooms worldwide, with 43% already under construction.

For the fiscal year ending in December 2026, analysts expect Marriott International’s adjusted EPS to grow 16.3% YOY to $11.65, and then rise by another 13.7% annually to $13.25 in fiscal 2027. The company’s earnings surprise history is mixed. It beat the consensus estimates in three of the last four quarters while missing on one other occasion.

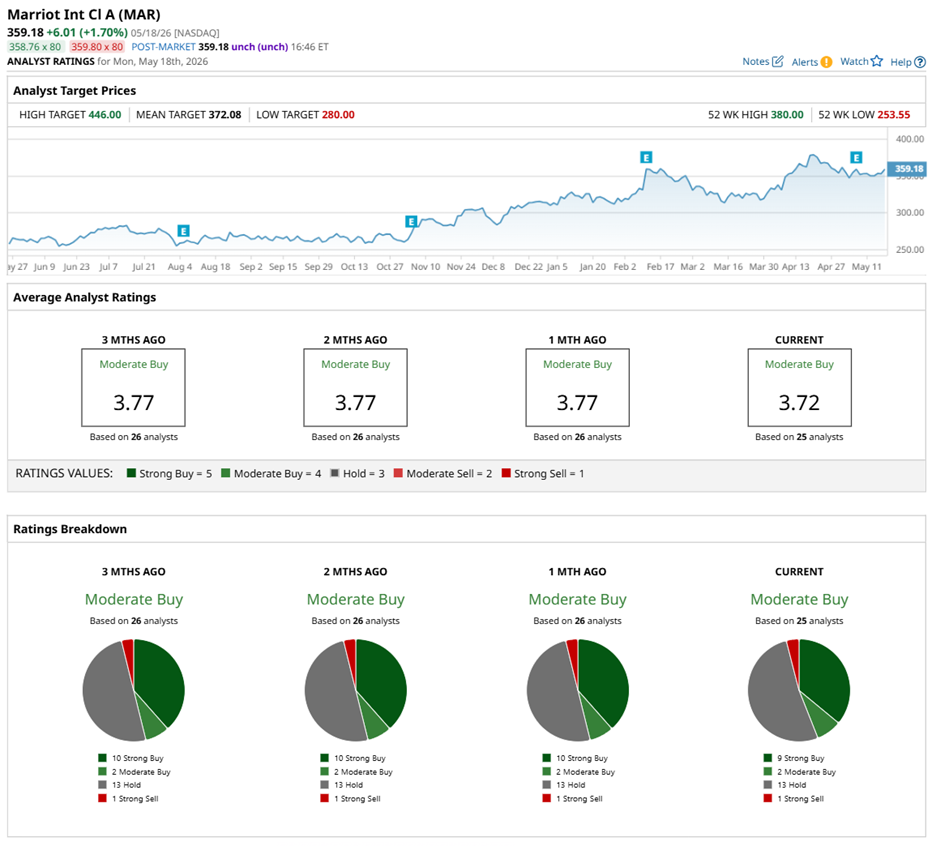

Wall Street still leans bullish on MAR stock, although there’s a little hesitation creeping in. The overall consensus rating on the stock stands at a “Moderate Buy” based on coverage from 25 analysts. That includes nine “Strong Buy” ratings, two “Moderate Buys,” 13 “Holds,” and one “Strong Sell.”

The configuration still looks pretty steady overall, though optimism cooled just a bit after the number of “Strong Buy” ratings slipped from 10 to 9.

Most recently, Bernstein slightly lifted its price target on MAR to $402 from $400 while keeping an “Outperform” rating. The firm said the bigger story for hotel stocks right now is not Middle East tensions, but the uneven shape of the U.S. economy. Bernstein believes the so-called “K-shaped” economy – where higher-income consumers keep spending while lower-income consumers feel pressure – still favors premium hotel operators like Marriott heading into 2026 and 2027.

As of writing, MAR stock’s mean price target of $372.08 implies an upside potential of 3.6%. The Street-high price target of $446, set by Wells Fargo earlier this month, suggests the stock could rise as much as 24.2% from the current price levels.