/Wynn%20Resorts%20Ltd_%20%20vegas%20hotel%20by-%20Jonathan%20Weiss%20via%20Shutterstock.jpg)

Las Vegas, Nevada-based Wynn Resorts, Limited (WYNN) designs, develops, and operates high-end integrated destination resorts that combine luxury accommodations with world-class gaming, dining, and entertainment. It is valued at a market cap of $10.4 billion.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and WYNN fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the resorts & casinos industry. The company operates through an integrated business model that targets high-net-worth travelers, leveraging premium amenities such as Michelin-starred restaurants, expansive retail galleries, and sophisticated meeting spaces to complement its casino operations.

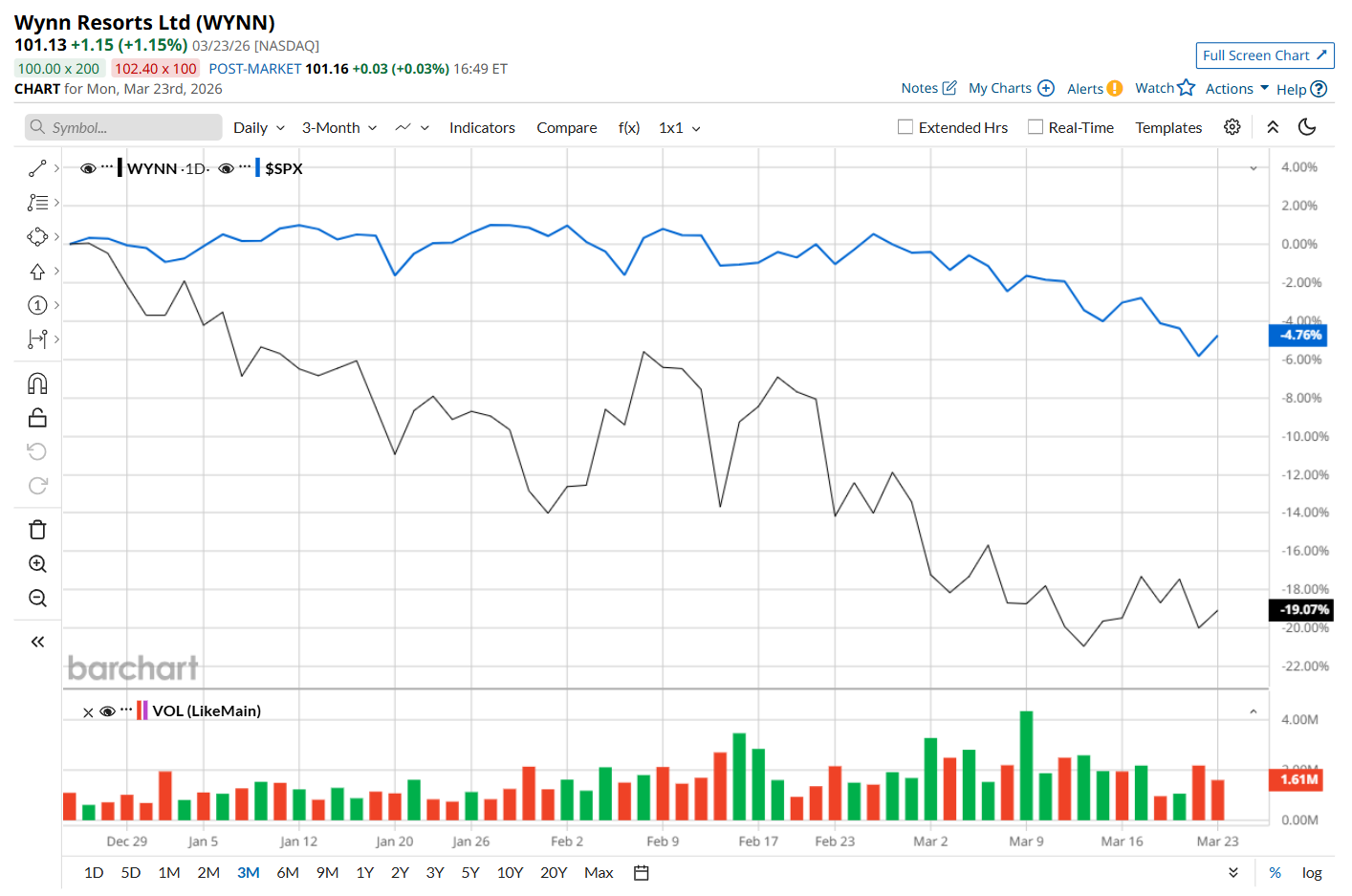

This resort and casinos company has dipped 24.9% from its 52-week high of $134.72, reached on Dec. 1, 2025. Shares of WYNN have declined 19.1% over the past three months, notably underperforming the S&P 500 Index’s ($SPX) 4.8% drop during the same time frame.

Moreover, on a YTD basis, shares of WYNN are down 16%, compared to SPX’s 3.9% loss. Nonetheless, in the longer term, WYNN has rallied 22.4% over the past 52 weeks, outpacing SPX’s 16.1% uptick over the same time frame.

To confirm its recent bearish trend, WYNN has been trading below its 200-day moving average since mid-February and has remained below its 50-day moving average since late December 2025.

On Feb. 12, WYNN shares tumbled 6.6% after posting mixed Q4 results. The company’s revenue increased 1.5% year-over-year to $1.9 billion, topping analyst estimates by 1.1%. However, due to lower-than-expected hold in both VIP and mass gaming segments, particularly in Macau, as well as increased operating expenses from payroll and ongoing renovations, its adjusted EPS of $1.17 and adjusted EBITDA of $466.9 million fell short of Wall Street expectations, which made investors jittery.

WYNN has lagged its rival, Las Vegas Sands Corp. (LVS), which rallied 28.8% over the past 52 weeks. However, it has outpaced LVS’ 17% drop.

Despite WYNN’s recent underperformance, analysts remain highly optimistic about its prospects. The stock has a consensus rating of "Strong Buy” from the 18 analysts covering it, and the mean price target of $143.50 suggests a 41.9% premium to its current price levels.