Chasing credit card rewards when you're in debt is surprisingly common. Two-thirds of Americans in debt try to maximize their credit card rewards, according to a new study by Bankrate. It's tempting to rack up miles or points to earn a vacation or cash back, but there's no way to win at that game if you're in debt.

"Chasing rewards while you’re in debt is a big mistake, says Ted Rossman, senior industry analyst at Bankrate. "The average credit card rate is a record-high 20.75%. The typical rewards payout is in the 1 to 5% range. It doesn’t make sense to pay 20% or more in interest just to earn 1, 2 or even 5% in cash back or airline miles."

Almost half of cardholders are succumbing to credit card debt, according to another recent Bankrate survey. Given the high average interest rates cited by Rossman, indebted cardholders can quickly find themselves unable to dig out of the debt hole.

Of course, some people turn to credit cards out of desperation when they can't make ends meet. Others slowly slide into debt before they realize they are in trouble.

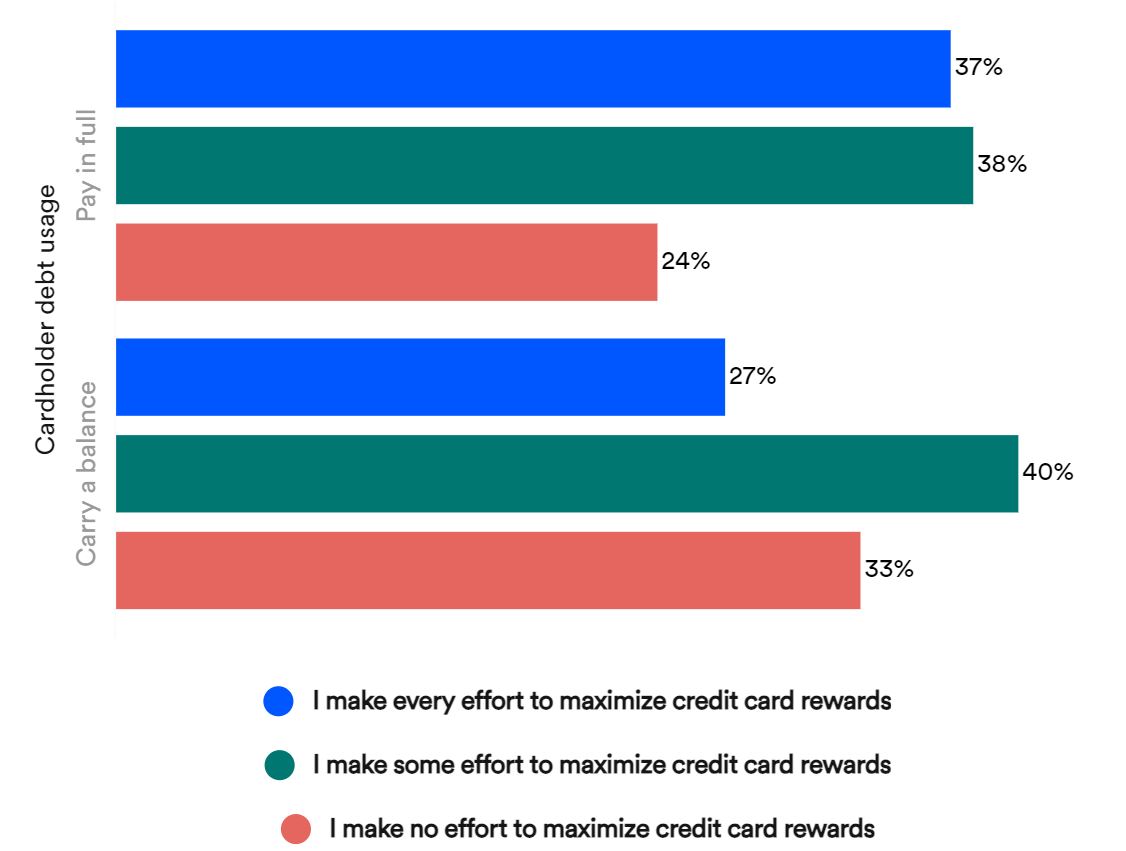

Chasing credit card rewards

Here's how cardholders responded to the Bankrate survey about their credit card rewards strategy. A staggering 67% of those who carry a balance every month say they "make every effort" or "make some effort" to maximize their credit card rewards.

This is your brain on credit cards

It's well-established that people tend to spend more money when they pay with a credit card instead of a debit card or cash — up to twice as much. The neuroscience behind this behavior was murky until a 2021 MIT study scanned subjects' brains as they used a credit card or cash. When using the credit card, the section of the brain responsible for pleasure and the anticipation of pleasure (the dopaminergic reward center) lit up.

What else has this effect on the brain? Drugs like cocaine and amphetamines. So, using your credit card essentially gives you a shopping high. Add cash back or airline miles to that effect, and it's easy to see how those in debt might be tempted to use their rewards credit cards even when it is irrational.

Paying off debt also feels good

Out-of-control debt is a burden that stresses relationships and physical and mental health. Debt can also exacerbate existing problems, such as addiction or depression. So it stands to reason that getting out of toxic debt can be a relief. But it may also boost cognitive and psychological function according to a National University of Singapore study.

Researchers worked with a non-profit group that paid off some of the debt accounts of poor, highly indebted subjects. After three months, test subjects performed significantly better on cognitive tests and decision-making. They also had less anxiety. The study also found that the number of debts was almost as stressful as the amount of debt, so reducing total indebted accounts can also benefit brain and psychological health.

For those in credit card debt, this reward is much healthier than miles or points.

Are rewards credit cards for you?

If you hear the siren song of a cash back or travel rewards card and you currently have credit card debt, just say no.

“Ideally, you'd revisit your credit card strategy every year or two to make sure that you're using the optimal products for your spending habits," said Rossman. Credit card interest rates "should be the primary consideration if you have credit card debt. If you're debt-free, then go for rewards."

While it may be tempting to turn to "debt relief" services if you carry a balance each month, there are better ways to pay off credit card debt. Although it may seem counterintuitive to turn to another credit card for help, a balance transfer credit card with a long pay-back period could be a lifesaver — if you know you can develop a payment plan and stick to it.

Don't cut up your cards to avoid temptation. You should probably first consider keeping your credit cards active to protect your credit score. And if you or a partner struggle with compulsive spending or other behaviors that keep you in debt, consider seeing a financial therapist for a healthier relationship with money.