Valued at a market cap of $26.2 billion, Constellation Brands, Inc. (STZ) produces, imports, markets, and sells beer, wine, and spirits. The Rochester, New York-based company owns and markets several well-known brands such as Corona, Modelo Especial, Pacifico, Robert Mondavi, Kim Crawford, Casa Noble Tequila, and High West Whiskey.

Companies valued at $10 billion or more are typically classified as “large-cap stocks,” and STZ fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the beverages-brewers industry. The company benefits from strong brand recognition, extensive distribution networks, and a strategic focus on premiumization, allowing it to capture higher margins and maintain a strong competitive position in the industry.

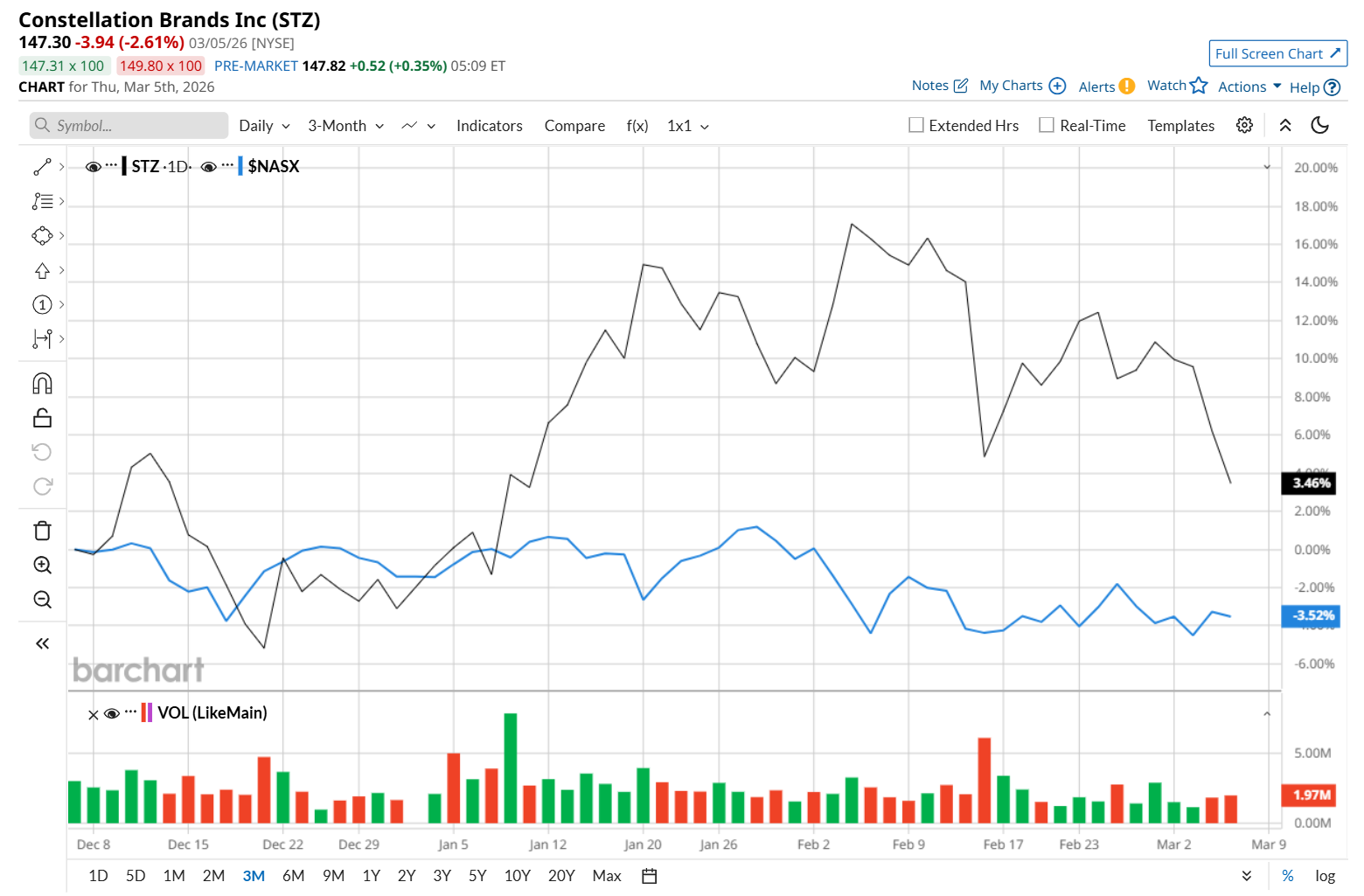

This alcohol company is currently trading 25.2% below its 52-week high of $196.91, reached on May 16, 2025. Shares of STZ have gained 3.5% over the past three months, outperforming the Nasdaq Composite’s ($NASX) 3.5% drop during the same time frame.

Moreover, on a YTD basis, shares of STZ are up 6.8%, compared to NASX’s 2.1% decline. However, in the longer term, STZ has decreased 15.4% over the past 52 weeks, considerably trailing behind NASX’s 22.6% uptick over the same time frame.

STZ has recently started trading below its 200-day and 50-day moving averages since early March.

On Jan. 7, STZ delivered stronger-than-expected Q3 earnings results, and its shares surged 5.3% in the following trading session. Due to lower shipment volumes, the company’s net sales declined 9.8% year-over-year to $2.2 billion, but topped analyst estimates by 1.8%. Meanwhile, its adjusted EPS of $3.06 fell 5.8% from the year-ago quarter, handily topping consensus expectations of $2.65.

STZ has underperformed its rival, Anheuser-Busch InBev SA/NV (BUD), which soared 18.5% over the past 52 weeks and 15.1% on a YTD basis.

Looking at STZ’s recent outperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 24 analysts covering it, and the mean price target of $170.54 suggests a 15.8% premium to its current price levels.