If you like to oversee your own retirement planning, you have to do some homework. Most of you have gotten used to that and spend time on researching, sorting opinions and putting together the best approach for you and your family. Complicating the process is your need to address three key retirement objectives — lifetime income, liquidity for unplanned expenses and legacy for kids and grandkids. And, of course, you want to lower your taxes and have less market risk.

The product-by-product approach

Choosing among financial product options is sometimes fairly easy and is sometimes more challenging. When you’re comparing, for example, investments against guaranteed lifetime annuities, it’s not that difficult to measure market risk, tax effects and liquidity. It’s rarely an either/or decision, but rather a “how much.”

An advantage of this DIY approach is that you are in control of the decisions. The way to have confidence in your decisions, however, is to look at a plan with the options built in and then exclude those that don’t feel comfortable.

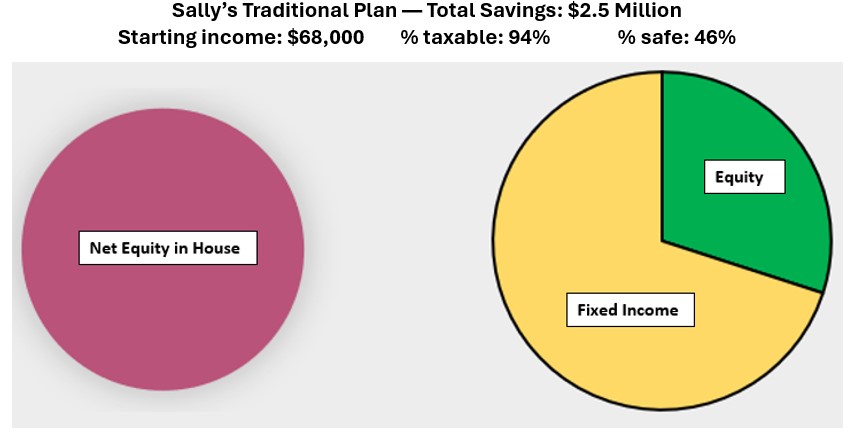

A traditional plan is a start for most retirees

Here’s an example for Sally, the sample investor we often refer to, who at 70 years old looks at her financial situation in two distinct buckets:

- Retirement savings that total $1.5 million, with half in her rollover IRA and half in her personal (after-tax) accounts

- Her home, worth $1 million with no mortgage

She may have another bucket for short-term cash needs or higher-risk investments. These are excluded for this exercise when planning for the three key objectives.

As she developed her traditional plan below, Sally has followed conventional wisdom in at least two other respects:

- She invests her retirement savings 30% (100 less her age) in equities and 70% in fixed income

- She plans to own her home without any mortgage in retirement

That’s about as simple as you can get. However, Sally realized it produces too little starting income ($68,000) vs. her 6% income goal — or $90,000 per year from her savings. (This doesn’t consider Social Security payments or any pension.) Drawing down another $22,000 to start, and increasing that annually to account for inflation, creates the risk of her running out of savings. And the $90,000 income goal doesn’t even consider the costs of long-term care and other unplanned expenses. (For more on this, see my article How ‘Home-Based Planning’ Can Address Long-Term Care Costs.)

Sally’s DIY starter plan is easy to understand, but if spending down your savings is not the answer, then how do you find the right plan design for you?

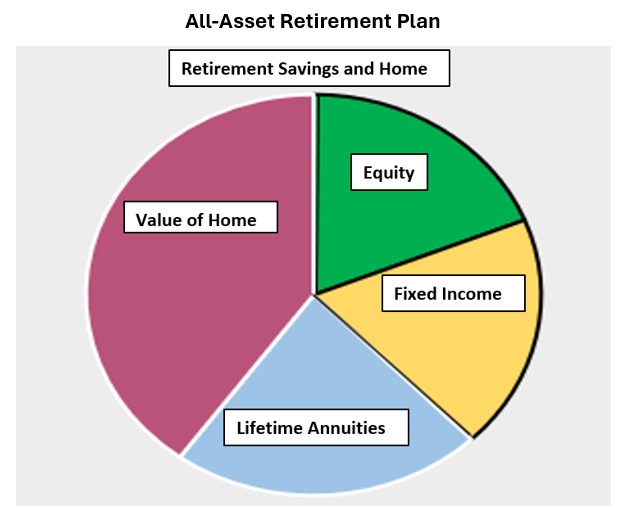

Start with a plan with the three L’s, then find the products

Begin with your goals, which for most retirees include lifetime income, liquidity for unplanned expenses and a legacy for heirs. To achieve those three L’s, your savings — including equity in your home — can be put to work in ways that Sally ignored in her plan above. Another part of the plan involves deciding which of your savings accounts you want to buy products from: tax-qualified or personal (after-tax) savings. Then, select single-purpose financial products that can be put together or eliminated to best serve your purposes.

For people who want to live in their own home as long as possible during retirement, access to home equity through a home equity conversion mortgage (HECM) is a consideration. And for lifetime income, which eases the fear of running out of money, converting some savings into lifetime income annuities provides a solution.

Those two (HECM and lifetime annuities) are not on every adviser or planner’s radar, but they should be on yours. Here’s a revised picture that shows how lifetime annuities and the value of the home add to a retirement plan. We call this an All-Asset Class Plan since it includes assets representing 90% of all asset classes.

Initial refinements to All-Asset Retirement Plan

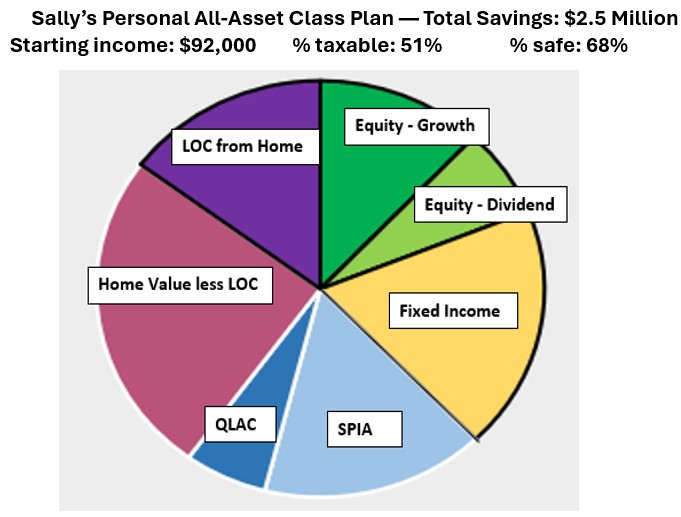

Now let’s apply these elements to Sally’s plan, which needs to be personalized for Sally’s age, gender and percentage of rollover IRA in her savings. Three important allocations are made in the refinement of this plan:

- Equity portfolios are allocated between high-dividend and growth portfolios

- The lifetime annuities are allocated between a SPIA (single premium immediate annuity) for current income and a QLAC (qualifying longevity annuity contract) for future income

- The value of the home is allocated between the HECM line of credit (with the amount determined by LOC percentages set by HUD) and the remaining equity

Sally’s personal All-Asset Retirement Plan delivers starting income of $92,000 that exceeds her objective of $90,000. She can add that extra $2,000 to her budget or reinvest it for future budgets.

Other deliverables under Sally’s personal All-Asset Class Plan

As you can see above, 68% of Sally’s income is “safe,” which means the income is not dependent on the liquidation or sale of investments. Even at a low market return, the plan will generate income from dividends, interest, annuity payments and drawdowns from HECM. (As part of the refinement process, planning software, such as that used by Go2Income, can test different investment returns and resulting plan outcomes.)

Her other objectives are also important, and the plan will help her achieve them:

- Liquidity. By adding the line of credit from HECM to her plan, more than 50% of her savings are liquid at the start, even with the addition of lifetime annuity payments.

- Legacy. Sally plans to live a long life, so the legacy, while delivered far in the future, equals or exceeds the original total value of savings.

- Lower taxes. Only 50% of her income is taxable through age 85. In turn, that will have a favorable impact on all of her taxable income, including Social Security and pension.

- Long-term care costs. Her liquidity is able to absorb, for example, substantial long-term care costs, with the impact felt on her legacy, not on income.

- Inflation protection. Under the starter plan with conservative return assumptions, her income grows by 1.4% per year until age 85. If inflation protection is a key objective, she can address it during the refinement process.

Of course, in order to achieve the best outcomes for Sally, she will need to speak with a financial adviser well-versed in all the elements of a diverse retirement plan. During that process, the plan can be attuned to Sally’s personal needs and desires.

You can order a Go2Income plan today based on the answers to three or four questions about your goals. Get started here with no obligation. Consult with your own qualified adviser, find an analytical tool to provide some guidance, or talk to a Go2Specialist.

.png?w=600)