With more retirees than ever choosing to age in place, the idea of selling your home to downsize may no longer be part of your plans.

That’s smart, because you don’t have to sell the homestead to produce retirement income and help cover the costs associated with a critical health crisis, or just the effects of aging that require outside care.

In the New York Times article The High-Class Problem That Comes With Home Equity, author Ron Lieber, the NYT’s Your Money columnist, suggests that reverse mortgages could be a good product for some retirees who want to tap the equity in their home without selling. We agree, and the Go2Income planning method can now incorporate a reverse mortgage.

I have found that lifetime income, liquidity for unplanned expenses, lower taxes and a financial legacy are the objectives most retirees seek. When they also want to stay in their homes or age in place, I propose that annuities and home equity, added to traditional savings and investments, will best meet their retirement goals.

In our previous article, The (R)evolution of Retirement Income Planning, we presented the advantages of a plan based on investments, annuities and a home equity conversion mortgage, or HECM. Let’s dig deeper into that plan for our sample investor. You’ll see the key elements and how they can be customized to your personal objectives.

Sally’s case

Sally, 70, is focused on starting income. She has $1.5 million in savings (50% in a rollover IRA account) and $1 million in the value of her house (without any mortgage). She understands that with income annuities added to her plans, she can be a little more aggressive and wants starting income of $96,000 a year — translating to 6.4% of her retirement savings, or 60% higher than the 4% rule. (Together with her $62,000 in Social Security benefits and pension, she’s up to $158,000 in starting income.)

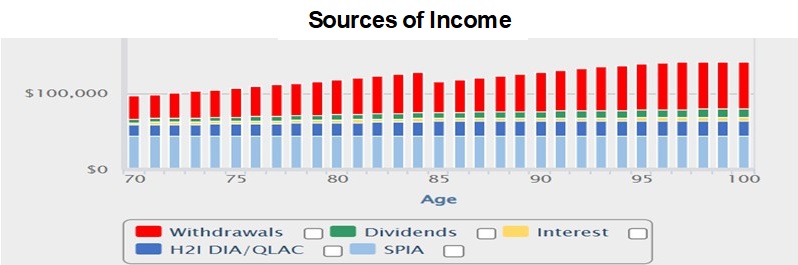

The following charts tell her story.

The first is her sources of income chart with Go2Income split into three sources:

- Investment portfolios: Dividends and interest from personal (after-tax) savings, RMDs and withdrawals from her rollover IRA account

- Annuities: Single-premium immediate annuity that provides lifetime annuity payments generated from personal (after-tax) savings for tax efficiency

- Home Equity2Income (H2I): HECM drawdowns until 85; QLAC lifetime annuity payments less HECM interest after 85

The product elements are allocated to accounts based in part on tax efficiency, and for Sally’s plan, less than 40% of the first-year income is taxable, with over $92,500 of the $96,000 becoming her spendable income. Also, a very large percentage of income is safe, meaning she doesn’t have to liquidate securities to realize the cash flow. Nearly 60% is safe over her lifetime.

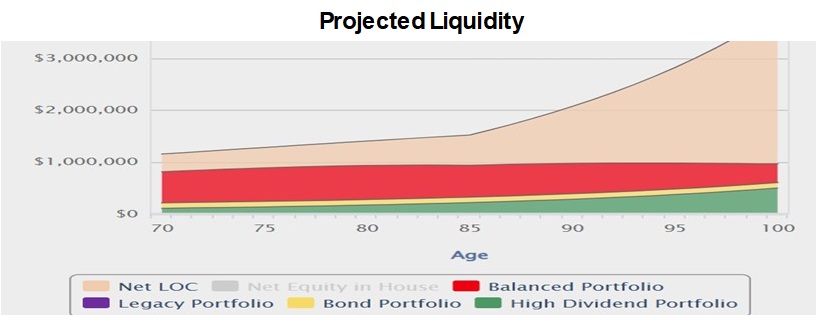

The second chart is her projected liquidity, which may be the biggest surprise, with liquid funds to cover planned and unplanned expenses, like long-term care, modifying the house for aging-in-place necessities, etc. These funds are made up of the following:

- Investment portfolios: High-dividend portfolio (personal savings), fixed income portfolio (personal savings) and balanced portfolio (rollover IRA account)

- Home Equity2Income: HECM net line of credit

This plan meets Sally’s objectives for lifetime income, but also provides substantial liquidity for late-in-life spending — both planned and unplanned.

A reminder of the world before the evolution of retirement

It wasn’t so long ago when almost all retirees could be comfortable with income from Social Security benefits, savings and perhaps a pension or an IRA.

For most of us, pensions are now unattainable. Happily, Social Security is designed to be lifetime income, and if you worked 40 years and paid into the program, it will provide a good chunk of safe income. Your savings also might provide significant income, but investments in stocks and bonds can vary from year to year. In our prior article, we showed how each product element improved the results, in terms of income, liquidity, taxes and safety.

Another application of H2I

It doesn’t appear that we will ever go back to the days when we could retire without thinking too much about the income that we knew would flow in each month from a pension and Social Security. The (R)evolution of Retirement article, however, provides the information to help you make the decisions required by today’s environment.

When I was running the product area of a life insurance company, I knew that customers liked the lifetime protection of annuities. But some didn’t want to give up access to their funds. Back then, I got a patent on something called the Income Manager, which enabled the annuitant to cash in future payments and get access to some funds. While I can’t violate the patent, there is a need there that might be fulfilled somewhat differently:

By combining an HECM with annuities in different proportions, consumers get lifetime income (although at lower levels than Sally chose) and still maintain a large portion of savings as liquid. The available line of credit from HECM nearly matches the premium for the annuity and thus maintains most of your liquidity while gaining the annuity’s lifetime protection. We’ll explain in more detail in the next article.

Visit Go2Income Personal Planning to start a plan risk-free. You can ask one of our analysts to help you make adjustments. And then decide whether you want the peace of mind that lifetime income and greater liquidity can provide.

.png?w=600)