The Dallas, Texas-based Southwest Airlines Co. (LUV) is a major passenger carrier, offering scheduled domestic and select international flights. The company runs an all-Boeing 737 fleet and builds its service model around efficiency and frequency. Its ecosystem extends beyond tickets, with offerings such as Rapid Rewards, SWABIZ corporate booking, in-flight entertainment, and ancillary services.

With a market cap of approximately $20.2 billion, the company occupies the “large-cap” territory, a space reserved for firms valued above $10 billion. The scale signals a durable network, high-frequency routes, and an operating rhythm that has long set Southwest apart in a fiercely competitive industry.

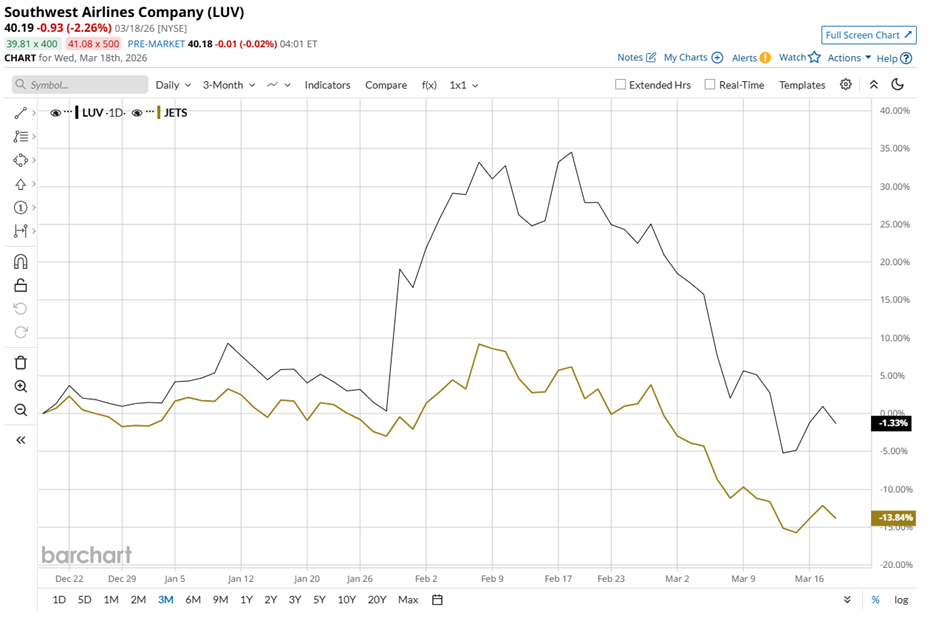

Southwest Airlines’ shares are trading 27.1% below their 52-week high of $55.11 reached in February. Over the past three months, the stock has edged down 1.3%, a modest decline that stands in sharp contrast to the 13.8% drop in the U.S. Global Jets ETF (JETS), highlighting relative strength.

The longer-term picture reinforces the trend. Over the past 52 weeks, LUV stock has gained 24.1%, comfortably outpacing the ETF’s 13.6% return. In 2026, the stock is down 2.8% YTD, while the ETF has fallen 12.4%, suggesting that even in a softer tape, the company continues to hold its footing better than the broader airline basket.

From a technical standpoint, the stock has remained below its 50-day moving average of $46.39 since the start of the month, signaling near-term caution. Yet, it continues to hold above its 200-day moving average of $36.89 since November 2025.

On Jan. 28, Southwest Airlines reported its Q4 fiscal 2025 results, setting off a sharp market reaction as the stock jumped 18.7% in the next trading session. Revenue reached $7.44 billion, falling short of the $7.52 billion Street estimate, yet it grew 7.4% year over year. Meanwhile, adjusted EPS came in at $0.58, ahead of expectations of $0.56 and up 3.6% from the prior year’s quarter.

Management’s outlook adds weight to the momentum. They guide for full-year adjusted EPS of at least $4, setting a conservative baseline that leaves room for upside if trends hold. For Q1 fiscal 2026, the company expects adjusted EPS of at least $0.45, marking a turnaround from a loss of $0.13 per share in Q1 fiscal 2025.

To put performance into perspective, Alaska Air Group, Inc. (ALK) has declined 27.6% over the past 52 weeks and remains down 24.7% YTD, a sharp divergence that underscores the relative resilience in Southwest Airlines’ trajectory.

Wall Street’s stance reflects that underlying confidence. Among 24 analysts, the consensus rating stands at “Moderate Buy,” pointing to a cautiously constructive outlook. To that end, the average price target of $47.64 suggests potential upside of 18.5% from current levels.