When Americans move abroad, their financial lives become significantly more complex. From navigating foreign tax systems to understanding how U.S. retirement accounts are treated overseas, the stakes rise even as the margin for error narrows.

That's why choosing the right cross-border financial planner is so important. High-earning and high-net-worth U.S. taxpayers must find someone who understands the full scope of cross-border financial planning and is committed to a long-term relationship.

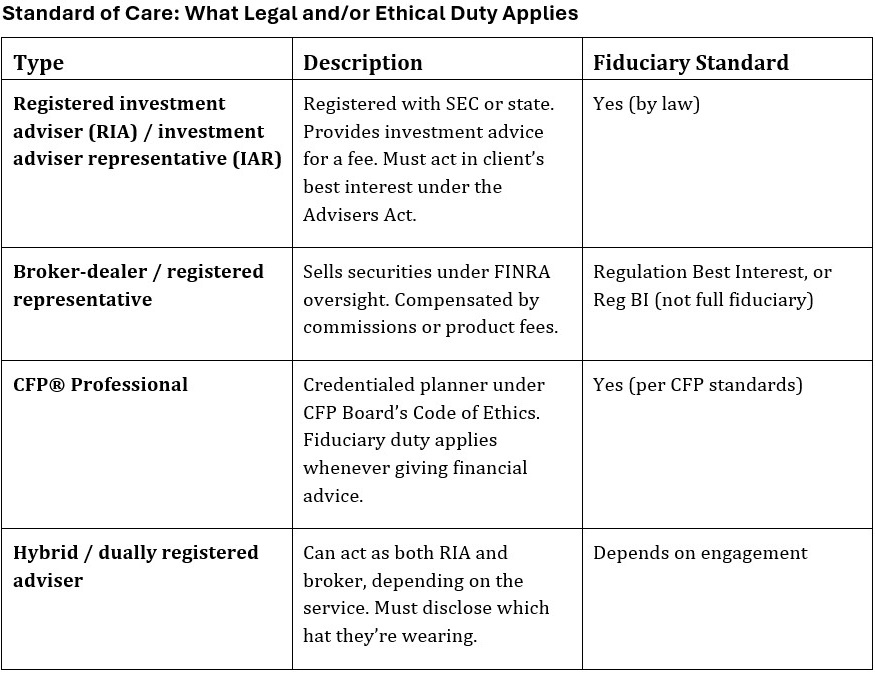

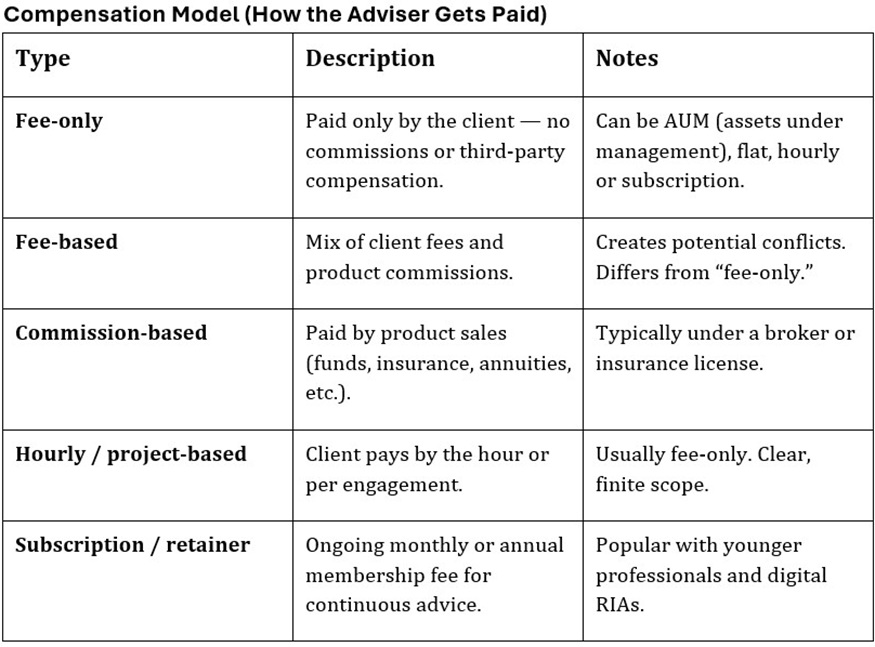

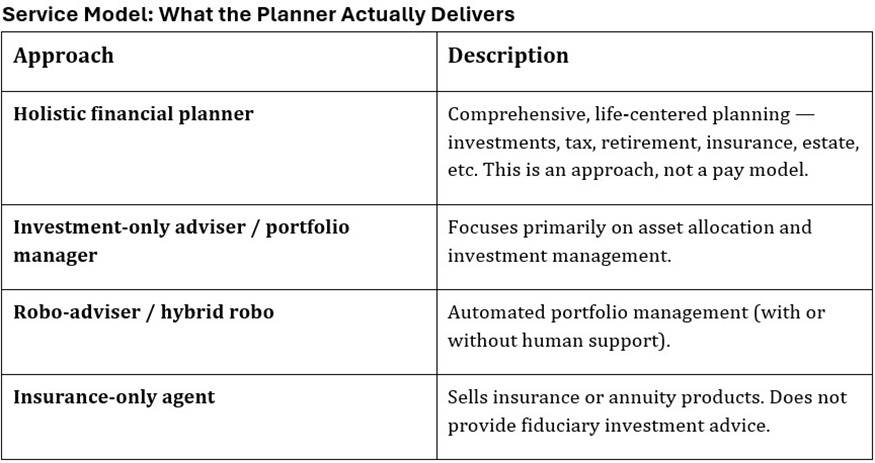

A brief review: Types of financial planners

When we talk about different "types" of financial planners, they can be differentiated across three spectrums:

For Americans living in the U.S., these distinctions help guide their choice of professional financial planning service. But for those moving abroad, the meaning of these categories takes on new importance.

Why cross-border planning changes everything

Let's say you're working with a U.S.-based investment manager who doesn't offer planning services. That might work fine while you're stateside; many people feel more comfortable steering their own financial planning ship and personally checking that their compass is pointing due north.

But moving abroad without the support of cross-border expertise to guide the revision and implementation of your financial planning framework can lead to costly mistakes.

Take France, for example. It's often considered one of the "easier" Western European countries for Americans to retire to, thanks to a favorable tax treaty and a relatively straightforward long-stay visitor visa.

But even there, there are common tripwires. One of the most overlooked is the cotisation subsidiaire maladie, more commonly known as the PUMa tax.

The PUMa tax was introduced to help fund France's universal health care system and applies to residents who receive significant passive income, such as dividends, rental income or investment gains, but have little or no earned income.

Here's how it works:

- If your earned income is below 20% of the French social security threshold (PASS), which is €9,273.60 in 2024 (the most recent tax year), and

- Your passive income exceeds 50% of the PASS, or €23,184 in 2024, then

- You may be subject to a 6.5% tax on the portion of your passive income above that threshold.

This tax does not apply if you receive replacement income such as pensions, disability payments or unemployment benefits.

It also doesn't apply if your spouse or civil partnership (PACS) partner earns above the threshold or receives qualifying replacement income.

The formula used to calculate the tax is nuanced, adjusting the rate based on how much earned income you have.

For example, Jean and Marie, both U.S. citizens, move to France and become French tax residents. They draw no earned income in France (well below the €9,273 threshold for 2024) and instead live off €120,000 of U.S. investment dividends.

Because their passive income easily exceeds the €23,184 "50% of PASS" threshold for 2024 and their earned income is minimal, they could face about €6,375 in tax (6.5% of the amount above €23,184) — a surprise many couples who retire abroad don't budget for.

This example illustrates a broader point: Even in jurisdictions considered expat-friendly, the financial landscape requires U.S. financial planners to have a certain familiarity with the local system in order to offer the highest-quality service.

Without a planner who understands both U.S. and local systems, you may be exposed to unexpected liabilities that at best are vaguely annoying, but at worst could derail your retirement plans.

The value of holistic financial planning for expats

When you take a holistic approach to cross-border financial planning, you're able to integrate the following when building a cross-border financial plan:

- Thoughtful relationship-building time in the initial meetings

- Tax planning across jurisdictions, i.e., cross-border tax planning

- Visa and immigration considerations

- Estate planning under foreign laws

- Currency and banking logistics

- Retirement account treatment abroad

A holistic approach ultimately allows the planner to structure the client's portfolio in a way that avoids triggering unexpected taxes or compliance issues.

And, depending on where your cross-border planner is based, they may be equipped to help you navigate the cultural and bureaucratic differences that come with living in another country.

Common pitfalls

1. Continuing with a U.S.-based planner without cross-border experience

Americans understandably want to maintain their existing financial planning relationships when they move abroad.

But, as Arielle Tucker, CFP® and founder of Connected Financial Planning, notes, "Unless your planner has experience with cross-border clients, and ideally specializes in your destination country, they may not be equipped to serve you effectively."

2. Working with EU advisory firms

On the other hand, some expats choose to work with a foreign firm, thinking that working with a local firm in their adopted country is a logical or even savvy financial move. However, this can present challenges.

"Foreign firms typically have higher fees and transaction costs than the U.S., and foreign mutual funds and ETFs are considered PFICs (Passive Foreign Investment Companies for American investors," says Ricardo Jesus, financial adviser at Liberty Atlantic Advisors (also an Adviser Intel contributor).

"This causes additional reporting and tax complications. Plus, client service expectations differ radically between the U.S. and Europe. As an example, execution timelines are often much slower."

Final thoughts

Candidly, moving abroad can feel like you've turned your life upside down and changed the operating language. So, it's completely understandable to seek familiarity among the chaos.

But, speaking as someone who has moved to different countries nearly half a dozen times, I can attest that prioritizing familiarity can come at the expense of long-term stability, particularly when we're talking about financial planning.

Moving abroad is a major life change, and your financial plan needs to reflect that. That said, it doesn't need to be an overwhelmingly frightening change.

Working with a cross-border planner or firm that takes a holistic approach outsources the challenging task of finding the optimal financial through-line in your life abroad, allowing you to be fully present in the new day-to-day of living your life abroad.

Related Content

- I'm a Cross-Border Financial Adviser: 5 Things I Wish Americans Knew About Taxes Before Moving to Portugal

- How to Manage Retirement Savings When Living Abroad

- Where to Retire: Living in the Dominican Republic

- Want to Move to Portugal? What to Consider Financially

- The Pros and Cons of Retiring Abroad

This article was written by and presents the views of our contributing adviser, not the Kiplinger editorial staff. You can check adviser records with the SEC or with FINRA.