For more than a century, Principal Financial Group, Inc. (PFG) has built its business around something most investors rarely think about until later in life – retirement, protection, and long-term wealth planning. Founded in 1879 and based in Des Moines, Iowa, the company today operates across retirement solutions, asset management, and insurance services for businesses, individuals, and institutional clients worldwide.

With a market cap of roughly $23.5 billion, Principal Financial has become one of the bigger names in the financial services space, managing retirement plans, pension solutions, mutual funds, life insurance products, and alternative investments through its diversified business model.

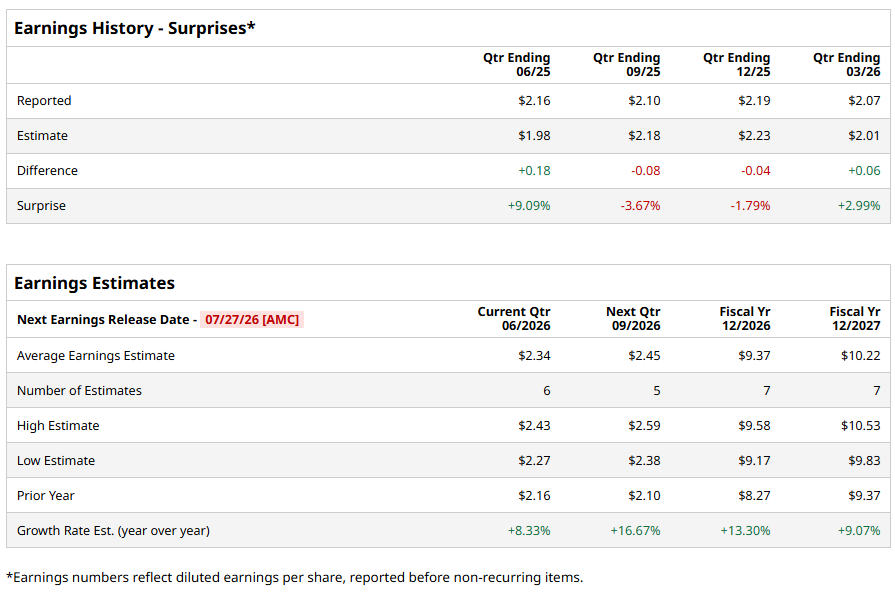

The company is expected to unveil its fiscal second quarter 2026 financial results on Monday, July 27, after the market closes. Ahead of the event, analysts tracking the company expect its profit to be around $2.34 per share on a diluted basis, up 8.3% from an EPS of $2.16 in the year-ago quarter. The company has a mixed history of earnings surprises, surpassing Wall Street’s EPS estimates in two of four quarterly reports and missing on two other occasions.

For the full year, analysts expect the company to report an EPS of $9.37, up 13.3% from $8.27 in fiscal 2025. Its EPS is expected to rise around 9.1% year over year (YOY) to $10.22 in fiscal 2027.

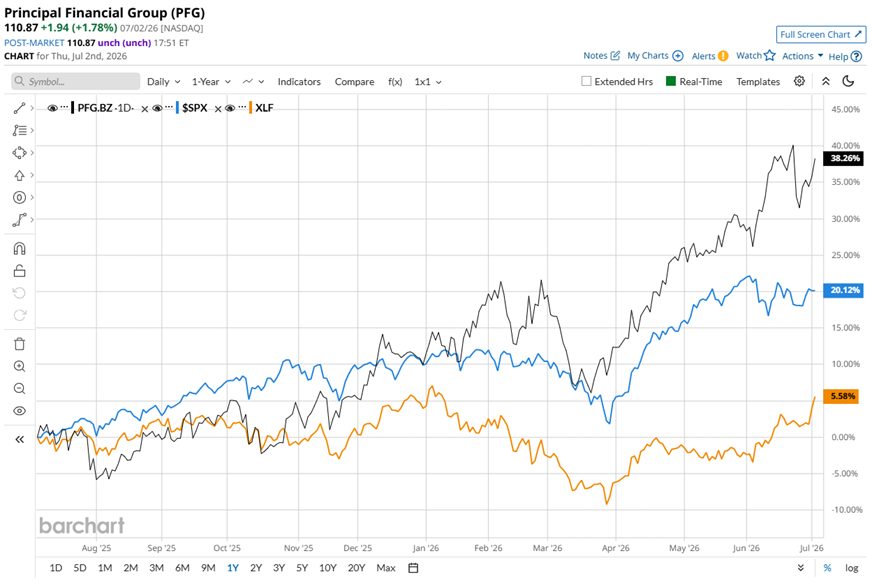

Principal Financial Group’s steady business setup has also translated into strong stock performance lately. Shares of the financial services company have gained 37.7% over the past 52 weeks, outperforming the S&P 500 Index’s ($SPX) 20.2% returns. Narrowing the focus, PFG has outperformed many of its own financial-sector peers too. The stock has surged past the returns of the State Street Financial Select Sector SPDR ETF (XLF), which gained just 5.7% over the past year.

Principal Financial’s strong stock performance has not been driven by excitement. Instead, investors have been rewarding a business that’s quietly delivering better earnings, growing its core operations, and returning more cash to shareholders. That combination has helped PFG comfortably outperform the broader market over the past year.

A key catalyst came after the company reported its first-quarter 2026 results on April 23. Investors liked what they saw, sending the stock 2.4% higher after the release. While total revenue slipped slightly to $3.5 billion, the bigger story was profitability. Adjusted EPS jumped 13% YOY to $2.17, comfortably beating Wall Street’s expectations as lower expenses, wider margins, stronger fee income, and improved underwriting all worked in the company’s favor.

The long-term growth story also remains intact. As of March 31, 2026, Principal Financial managed $770.2 billion in assets under management, while total assets under administration reached an impressive $1.8 trillion. Management also pointed to continued strength across retirement solutions, small and mid-sized business offerings, and global asset management, while improving mortality and underwriting trends added another tailwind for its insurance business.

Then there’s the dividend, which continues to attract long-term investors. Principal Financial raised its quarterly dividend by 8% to $0.82 per share and has now paid dividends for 23 consecutive years. That blend of earnings growth, disciplined execution, expanding assets, and dependable shareholder returns has been a major reason investors have continued rewarding PFG stock.

The overall consensus rating on PFG currently sits at “Hold.” Among 14 analysts covering the stock, one recommends a “Strong Buy,” one rates it a “Moderate Buy,” 10 suggest a “Hold,” one gives it a “Moderate Sell” rating, and one is outright skeptical, giving a “Strong Sell” rating.

As of writing, PFG stock trades above the average analyst price target of $103.23. The Street-high price target of $125 implies the stock could rise as much as 12.7% from the current price levels.