Semiconductor stocks have dominated headlines lately as enterprises pour money into data center infrastructure. After a record-breaking 2025, Nvidia (NVDA) remains the poster child of this frenzy, and its latest outlook suggests the growth story may be far from over. At its GPU Technology Conference (GTC) 2026, CEO Jensen Huang said he expects at least $1 trillion in cumulative GPU demand through 2027, up sharply from the $500 billion estimate discussed just a year ago, noting that demand is “off the charts” as AI shifts into a new phase of real-time inference and agentic computing.

With a rapidly expanding CUDA ecosystem, deepening partnerships with cloud giants like Amazon (AMZN), Microsoft (MSFT), and Alphabet (GOOG) (GOOGL), and innovations such as its Vera CPU platform, Nvidia appears well-positioned to capture a significant share of this trillion-dollar opportunity.

AI Dominance Continues to Drive Nvidia’s Growth

Nvidia is best known as the world leader in AI accelerators and GPUs. It specialized in the CUDA programming platform that made its graphics processors the standard for AI computing. While it still serves gamers, its Gaming GPUs division grew 47% last quarter, and about 90% of sales now come from its Data Center unit, selling chips and networking gear to hyperscale cloud and enterprise customers. Its market value has swelled to the multi-trillion-dollar range, which proves its dominance in the AI boom.

The company recently unveiled its next-generation Vera Rubin AI superchip, which is expected to ship in the second half of the year and promises up to 10 times the performance of current systems. Nvidia also secured a major multiyear strategic partnership with Meta (META) to deploy millions of GPUs, helping keep one of the world’s largest AI labs firmly inside its ecosystem.

Beyond AI data centers, Nvidia is also pushing into telecom and cloud software. It has teamed up with telecom companies to explore 6G networks on its AI-native chips while also investing $2 billion in AI cloud startup Nebius (NBIS) and backing the new AI supercomputing firm Thinking Machines to expand Nvidia GPU deployments.

Over the past two years, NVDA stock has roughly doubled as AI demand surged, rallying from the low $100s in 2024 to a peak above $210 last fall. After a brief cooldown into early 2026, NVDA shares are down 5% year-to-date (YTD), but the long-term growth story remains firmly intact.

Even after this run, valuation doesn't feel that lofty. The shares trade around 22× forward earnings, right in line with traditional tech and chip peers. When you consider that earnings are expected to grow by nearly 50% this year, that forward P/E starts to look like a pretty reasonable entry point for a company that is generating cash like this. But relative to the S&P 500, and given uncertainty around how much AI spending can be sustained, the stock looks richly valued on other classic metrics like the P/S ratio.

Huang Unveils a $1 Trillion AI Chip Bonanza

At Nvidia’s annual GTC, which happened between March 16 and 19, CEO Jensen Huang stunned the market. He announced that Nvidia has already booked $500 billion in AI chip orders for 2025-26, and he expects at least $1 trillion in demand through 2027. That includes new “Blackwell” and upcoming “Vera Rubin” GPUs for AI inference. Huang told investors he’s “certain computing demand will be much higher than that,” as enterprises race to deploy AI agents and inference workloads.

Investors greeted the forecast positively but pragmatically. NVDA stock ticked up about 1.6% on the day. Traders see the $1 trillion number as evidence that the AI runway is still expanding. Wedbush analyst Dan Ives called it a “confidence boost,” noting Nvidia is “alone at the top of the AI mountain” with a full-stack strategy.

Nvidia has Sizzling Financials

Nvidia's Q4 was nothing short of spectacular. Revenue soared 73% year-over-year (YoY) to $68.13 billion, another record. That beat Wall Street estimates and easily eclipsed last year’s $39.33 billion in Q4. Data Center revenue was the engine: at $62.3 billion, it jumped 75% YoY and made up over 90% of sales. The networking sector pulled in about $11 billion, more than triple year-ago levels, as cloud customers clamor for higher bandwidth.

Profitability exploded alongside sales. Nvidia reported net income of $42.96 billion for the quarter, up 94% YoY, and EPS was $1.57, nearly doubling last year’s $0.89. Gross margins ticked up to about 75%, helped by sales mix and high leverage on fixed costs. Operating cash flow was $36.2 billion, and free cash flow hit roughly $34.9 billion for the quarter. Nvidia ended the quarter with about $10.6 billion in cash on the balance sheet.

Colette Kress, Nvidia’s finance chief, called it “another outstanding quarter, with record revenue, operating income, and free cash flow.” She noted the growth was broad: cloud providers, enterprises, and even governments are all buying Nvidia’s AI infrastructure. As Huang himself put it, “Our customers are racing to invest in AI compute, the factories powering the AI industrial revolution and their future growth.” In other words, Nvidia claims it’s the inference leader with products achieving up to 50× better energy efficiency for AI workloads.

Looking ahead, management gave a bullish handoff. Nvidia guided Q1 FY2027 revenue around $78 billion, far above the roughly $72-73 billion analysts had expected. That implies another sequential jump, driven by continued AI rollout. The firm did not give EPS guidance but emphasized its supply chain and inventory commitments cover demand well into 2027.

What Wall Street Thinks of NVDA Stock?

Wall Street is firmly in Nvidia's corner following the GTC news. Morgan Stanley’s Joseph Moore, a top-ranked analyst, reiterated Nvidia as a "top pick" with a $260 price target, noting that the shift to AI inference is accelerating and Nvidia’s lead in "cost per token" is widening. He believes the $1 trillion demand projection could actually be conservative.

Over at J.P. Morgan, analyst Harlan Sur reiterated an "Overweight" rating with a $265 target. He pointed out that the $1 trillion figure is likely just the "lower bound" since it excludes several upcoming product categories, and he highlighted management's strong defense of their gross margins.

Bank of America chimed in positively, suggesting that Huang’s forecast implies a massive multiplier effect across the entire AI supply chain, from servers to networking. Even the skeptics are hard to find.

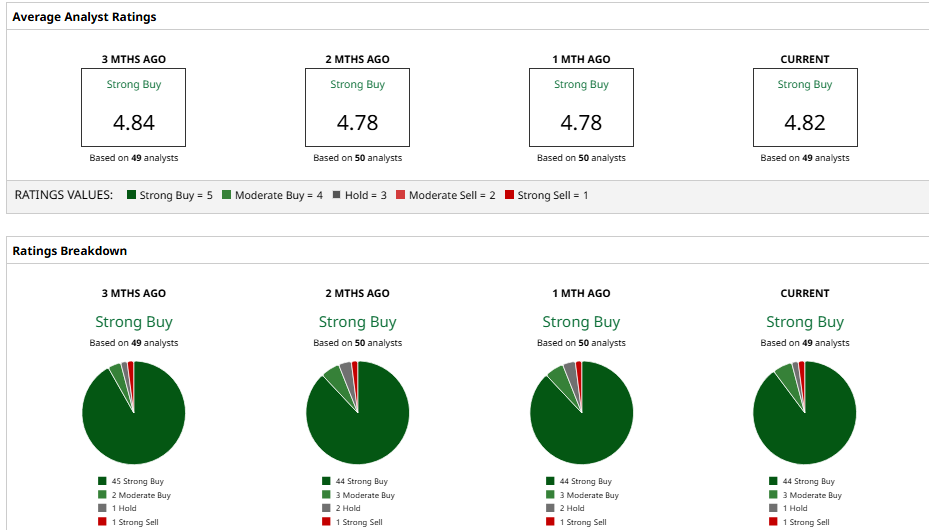

Overall, according to data from Barchart, the consensus rating is a "Strong Buy," with 40 out of 49 analysts recommending the stock. The average price target sits at $268.80, which implies a hefty 54% upside from recent trading levels.

In my opinion, for investors looking to capitalize on the next leg of the AI supercycle, NVDA stock could still offer compelling upside.