Chinese internet services provider Baidu (BIDU) shares fell 2.1% intraday on June 8, as the company’s name was added to the Department of Defense’s (DoD) list of Chinese military companies (CMC) operating in the U.S. Under the new criteria, which now include entities subject to the “direction or control of a greater number of Chinese administrative bodies and their affiliates,” the company is deemed to be indirectly linked to the State-Owned Assets Supervision and Administration Commission (SASAC) of the State Council of China.

This means Baidu could face procurement bans, supply chain exclusions, and investment restrictions. This heightened trade scrutiny might further spook investors, while the company goes through a slowdown in its legacy business. Beginning on June 30, the DoD will implement an "entity prohibition" that prohibits the department from directly contracting with any CMC or any organization controlled by a CMC.

About Baidu Stock

Baidu is a multinational Chinese technology company focused on internet services and artificial intelligence (AI). Headquartered in Beijing, China, the company operates primarily through its leading search engine, which enables users to find webpages, news, images, and multimedia content online. Also, Baidu provides a range of internet services, including mapping, cloud storage, and news aggregation platforms.

The company is a significant developer of AI technologies, creating advanced systems for autonomous driving and other intelligent applications. The company has a market capitalization of $40.52 billion.

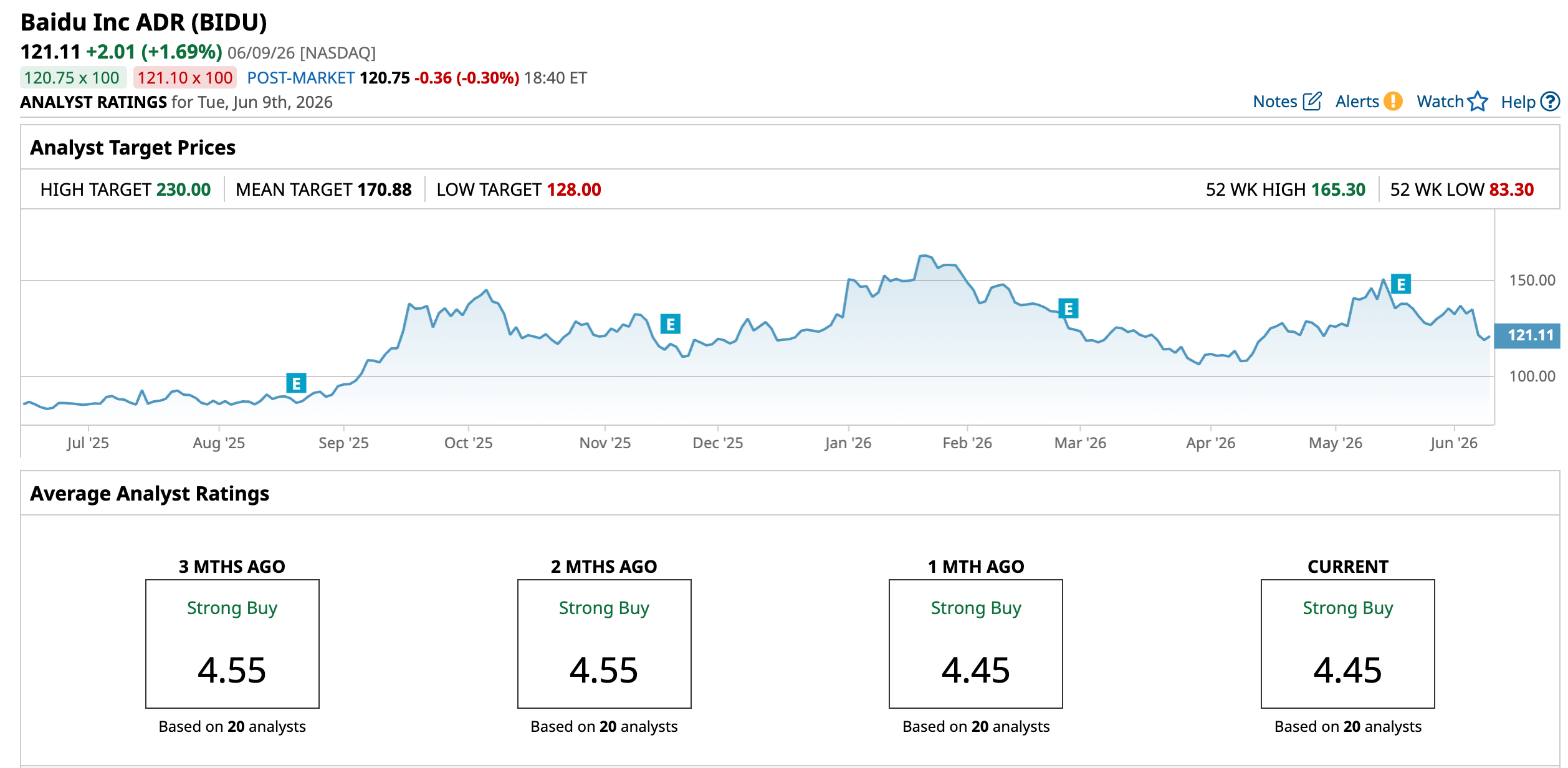

Investors have rewarded Baidu’s transformation from a legacy search company to an AI infrastructure leader. Over the past 52 weeks, the stock has gained 36.6%. However, due to some weakness in its legacy business, the stock is down 7.3% year-to-date (YTD). Baidu’s shares reached a 52-week high of $165.30 on Jan. 22, but are down 26.7% from that level.

On a forward-adjusted basis, Baidu’s price-to-earnings (non-GAAP) ratio of 15.29 times is modestly higher than the industry average of 12.87 times.

Baidu Branching Out

Over the years, Baidu has diversified its business significantly. Last year, the company introduced AI text and image generation capabilities, among others, to the mobile app’s search bar, powered by its Ernie AI models and other third-party AI agents. Its chip business is growing, as its chip unit, Kunlunxin Technology, is expected to be listed separately in Hong Kong and Shanghai. However, its automotive business seems to have hit a wall. In April, China suspended the issuance of new licenses for autonomous vehicles after Baidu’s Apollo Go robotaxis abruptly stopped in Wuhan.

Baidu Q1 Earnings AI Growth Offsets Ad Weakness, Net Income Falls

In the first quarter, AI emerged as Baidu's core revenue driver. The company’s revenue dropped modestly year-over-year (YOY) to RMB 32.08 billion ($4.74 billion). Its core AI-powered business’s revenue increased by 49% from the prior-year period to RMB 13.60 billion ($2.01 billion).

Also, this segment accounted for 52% of Baidu’s general business, which was considerably higher than the 36% weightage a year prior. Revenue from AI-native marketing services reached RMB 2.30 billion ($339.55 million), up 36% YOY, while Baidu App’s MAUs reached 655 million in March. On the other hand, its legacy business revenue dropped by 29% YOY to RMB 10.20 billion ($1.51 billion). Net income attributable to Baidu dropped 55% YOY to RMB 3.45 billion ($508.59 million).

Street analysts are robustly optimistic about Baidu’s bottom-line trajectory. For the current fiscal year, EPS is projected to surge 5.4% annually to $6.80, followed by a 28.4% increase to $8.73 in the next fiscal year.

What Do Analysts Think About Baidu’s Stock?

Last month, Susquehanna analysts maintained a “Neutral” rating on the stock, but raised the price target from $120 to $140. The price target increase follows the company’s Q1 results, in which it reported AI cloud momentum. However, a neutral stance was maintained due to a slowdown in its advertising business.

In the same month, Benchmark analysts reiterated a “Buy” rating and a $215 price target, as the company’s general business returned to growth in the first quarter, a trend the analysts expect to continue in fiscal year 2026, supported by accelerating industry-wide AI adoption and Baidu’s positioning as a full-stack service provider.

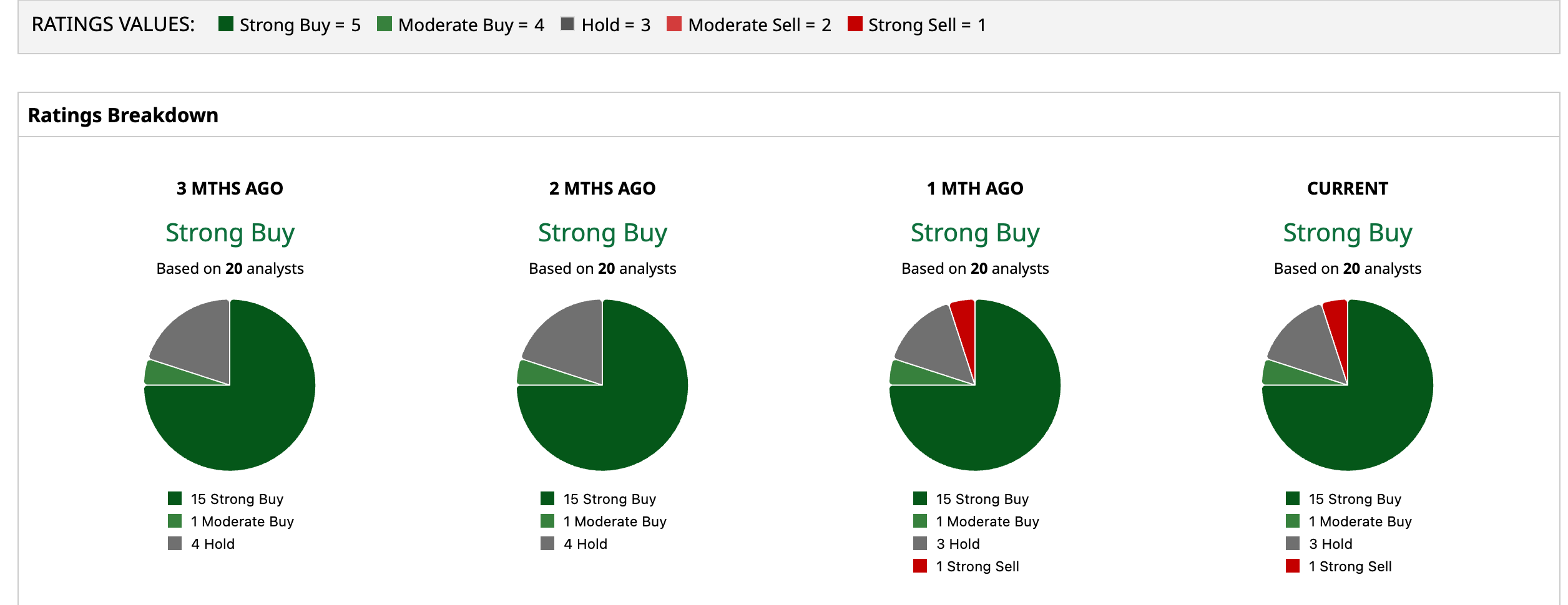

Wall Street analysts are strongly bullish on Baidu’s stock, with a consensus “Strong Buy” rating. Of the 20 analysts rating the stock, a majority of 15 analysts have given it a “Strong Buy” rating, one analyst suggested “Moderate Buy,” while three analysts are playing it safe with a “Hold” rating, and one gave a “Strong Sell” rating. The consensus price target of $170.88 represents 41.1% upside from current levels. Moreover, the Street-high price target of $230 reflects a 90% upside.