Footwear stocks do not always grab headlines, but when consumer demand stays strong and a brand owns a clear niche, investors tend to pay attention. In a retail market that has been choppy at times, companies tied to comfort and everyday spending have shown surprising staying power.

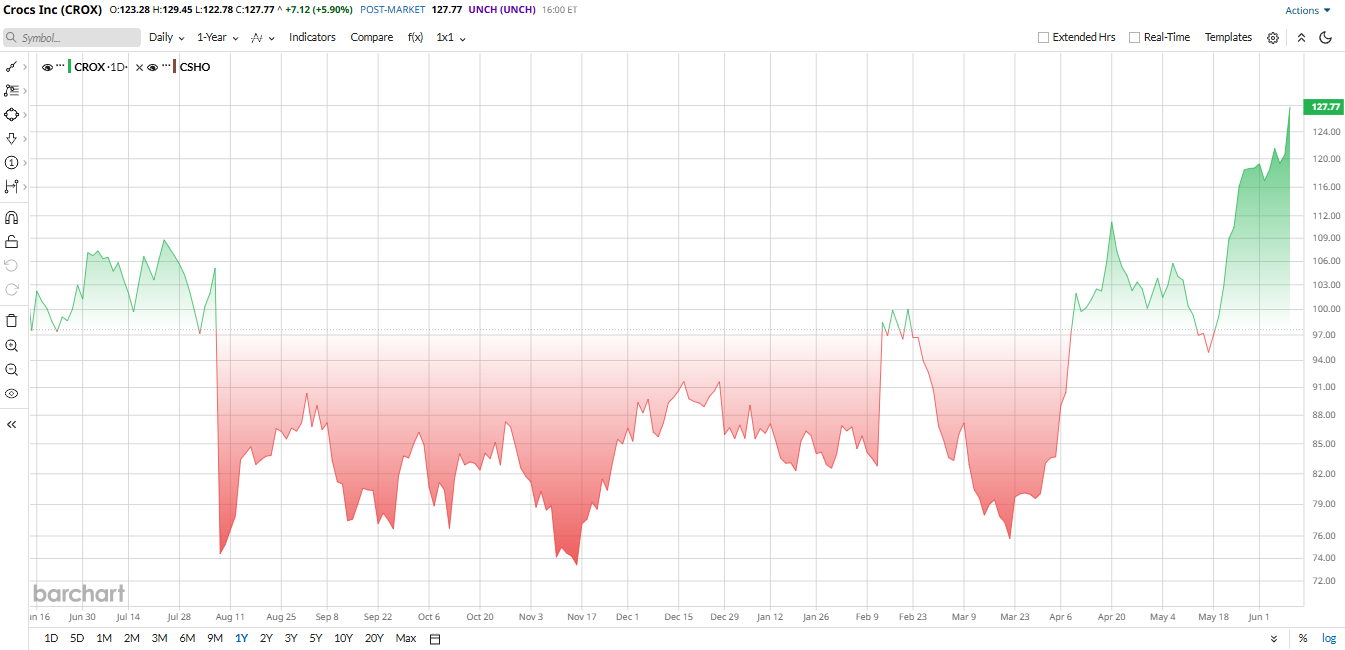

Crocs (CROX) has turned into one of the sharper comeback stories in consumer stocks. CROX stock has already surged more than 45% in 2026, yet Baird believes the rally is not over. With Crocs still trading at a reasonable valuation, its latest quarterly results holding up better than expected, and its international business still expanding, the bull case is starting to look harder to ignore.

What is driving the move, and why does Baird still see more upside after such a strong run? Here is a closer look at Crocs stock.

A Rally Driven by Better Visibility

The latest leg higher is not just about sentiment. Baird sees a more sustainable setup in Crocs North America and HEYDUDE, along with a return to healthier total revenue growth in the second half of 2026.

That improving outlook also supports the firm's view that earnings power could strengthen further over the next several years. Baird pointed to disciplined cost controls and solid cash-return potential, arguing that the stock could climb into the $170 to $200 range if 2027 profit expectations continue to improve.

Even after its strong rally, CROX stock exhibits a challenging valuation scenario. The price-to-sales (P/S) ratio of 1.5 times is notably higher than the sector median of 0.9 times, indicating a costly stock. However, the forward price-to-earnings (P/E) multiple of 9.3 times is significantly cheaper compared to the sector median of about 15 times, suggesting some level of underpricing.

Financial Results Still Support the Bull Case

Crocs’ first-quarter 2026 results gave the bulls fresh fuel. Revenue came in at $921 million, down 1.7% year-over-year (YOY), but adjusted diluted EPS was $2.99, roughly flat YOY and ahead of expectations. The Crocs brand posted $767 million in sales, up almost 1%, with direct-to-consumer revenue rising almost 13% to $322 million. Crocs brand international sales also climbed more than 7% to $421 million, even as overall HEYDUDE revenue fell more than 12% to $154 million.

CEO Andrew Rees sounded upbeat on the earnings call. “We had a strong start to the year as consumers responded positively to product newness across all categories,” he said. Rees also suggested that the international story still has a long runway, with Crocs “continuing to gain market share across the world.”

The company is not relying on North America alone. Crocs sells products in more than 85 countries, and its international Crocs revenue rose in the latest quarter even as wholesale softened.

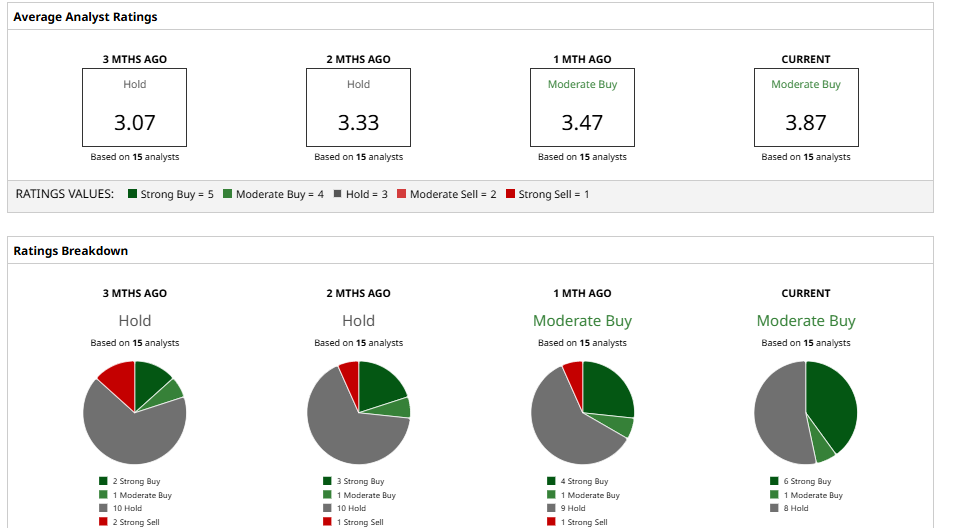

What Do Analysts Think of CROX Stock?

The Street is paying closer attention to Crocs again. Baird’s upgrade to an “Outperform” rating and $150 target was the clearest bullish call, but it is not the only firm leaning positive. BofA Securities raised its target to $145 from $125, while UBS has a “Neutral” rating with a $107 target.

Overall, the consensus from 15 analysts is a “Moderate Buy” rating with a mean price target of $122.27, which the stock has already surpassed. The Street-high $150 target implies potential upside of 19% from current levels.

In other words, analysts are not fully aligned on CROX stock, but recent data gives the bulls a stronger case than they had a few months ago.