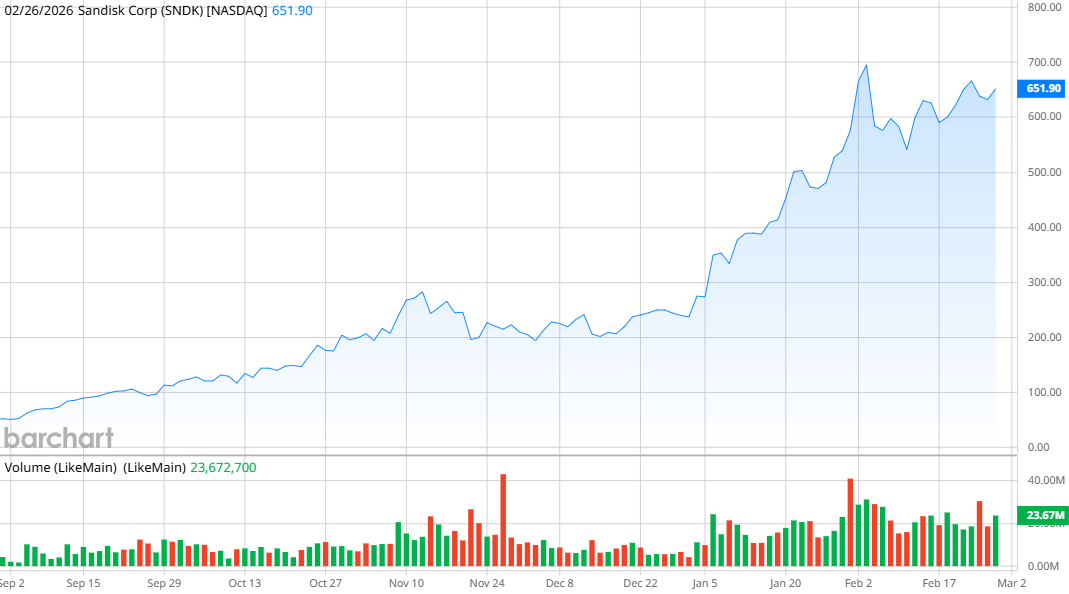

It has been a great 12 months for Sandisk (SNDK) and its investors. SNDK stock is up more than 1,100% in the past 52 weeks on strong optimism that the company’s NAND flash storage products and other computing memory devices will continue to be in high demand. Sandisk was the best-performing stock in all of the S&P 500 ($SPX) in 2025, and is continuing its strong performance with a 150% year-to-date (YTD) gain.

But a short report from Citron Research threatens to let some air out of Sandisk’s sails. Citron said Sandisk is vulnerable because it believes that NAND flash memory drive demand is cyclical rather than structural, and the company is ripe for a pullback.

"The market is pricing Sandisk like it's [Nvidia (NVDA)]," Citron said in a social media post. "There's one problem: Nvidia has a moat. Sandisk sells a commodity. We've seen this movie before [in] 2008, 2012, 2018. It's never different this time. Memory is a cycle, and cycles peak."

Citron also suggests that Samsung is the better computing storage stock. “Samsung has a 30-year history of choosing market share over margins," Citron said. "They wait for pure-plays like SanDisk to get comfortable at 50% gross margins, then flip the switch."

Is Citron right that Sandisk has run too high, too quickly?

About Sandisk Stock

Sandisk has an interesting history. The company was purchased by data storage company Western Digital (WDC) in 2016. But in 2023, Western Digital announced it would spin off Sandisk again into a new company that included Sandisk’s and Western Digital’s flash products, solid-state drives (SSDs), memory cards, and USB drives.

That has been a winning formula for Sandisk, which is based in Milpitas, California. With its dramatic rise in share price, the company now has a market capitalization of $83.4 billion.

Its products can be used in phones, laptops, cameras, and game systems. Sandisk also has a fast-growing edge computing segment, which supplies storage for smart devices that create data, such as cameras, drones, and motor vehicles.

Even with those gains in stock price, however, Sandisk is surprisingly affordable. SNDK stock’s forward price-to-earnings (P/E) ratio of 16 times compares favorably with Samsung. So, you’re paying a slight premium for Sandisk shares — but the stock’s performance over the last 12 months more than justifies the cost.

Sandisk Beats on Earnings

Sandisk continued its winning ways when reporting earnings for the fiscal second quarter of 2026. Revenue of $3.02 billion was up 61% from a year ago and 31% on a sequential basis. Net income was $803 million, up from $104 million in the same period last year, while EPS of $6.20 was much higher than the $3.49 EPS that analysts had projected.

Sandisk received most of its money from its edge computing segment, which generated $1.67 billion in revenue, up 21% sequentially. However, its data center segment grew even faster, up 64% sequentially to $440 million, while its consumer segment jumped 39% sequentially to $907 million.

“This quarter’s performance underscores our agility in capitalizing on better product mix, accelerating enterprise SSD deployments, and strengthening market demand dynamics, all at a time when the critical role that our products play in powering AI and the world’s technology is being recognized,” said CEO David Goeckeler.

Management issued Q3 guidance for revenue in a range from $4.4 billion to $4.8 billion, and net income per share between $12 and $14. If those projections hold, Sandisk is looking at a sequential revenue increase of 45% to 59%.

What Do Analysts Expect for SNDK Stock?

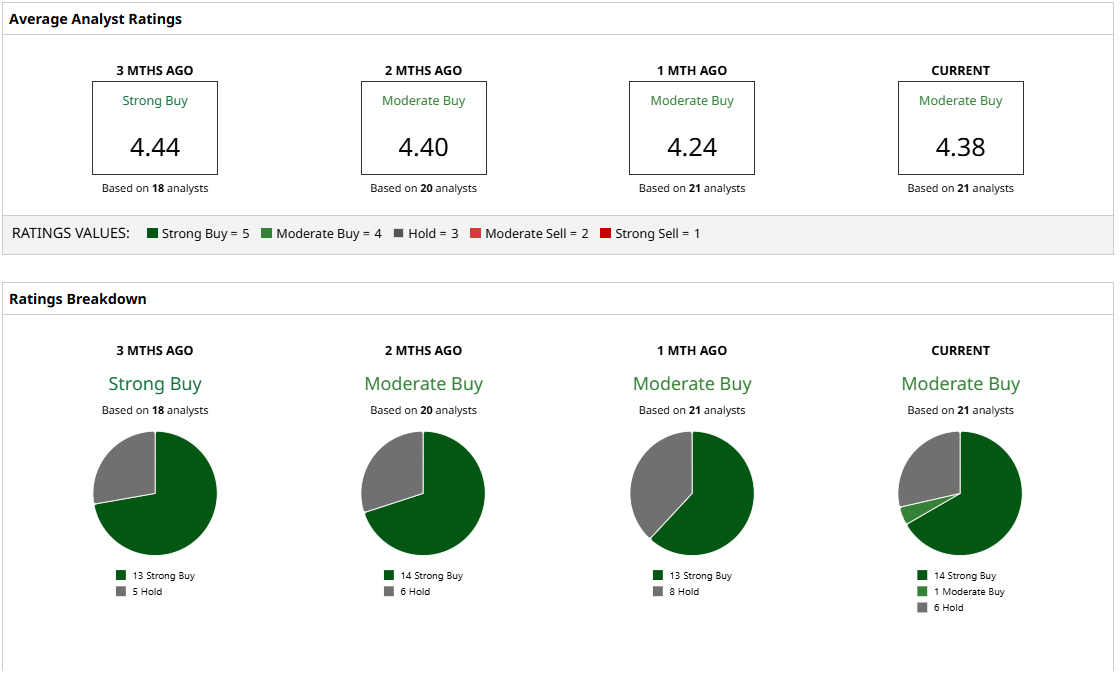

Citron is certainly an outlier when it comes to Sandisk. Despite the short report, the 21 analysts covering SNDK stock are overwhelmingly bullish, with 14 “Strong Buy” ratings, one “Moderate Buy,” and six “Hold” ratings.

The mean price target of $700.94 suggests a 17% potential gain from here. Meanwhile, the high target of $1,000 hints that a 67% increase could be possible, and the low $235 price target hints toward a possible 60% loss.

The big swing in price targets isn’t a huge surprise, considering how quickly SNDK stock has risen in 2026 alone. However, Sandisk is certainly riding the wave of data-center spending, as it is increasingly supplying storage systems to companies that are building out AI computing capacity around the world.

The Citron short report is worth noting, but for now, I’m still bullish on Sandisk. It’s a buy for me.