/Amazon%20-%20Image%20by%20Tada%20Images%20via%20Shutterstock.jpg)

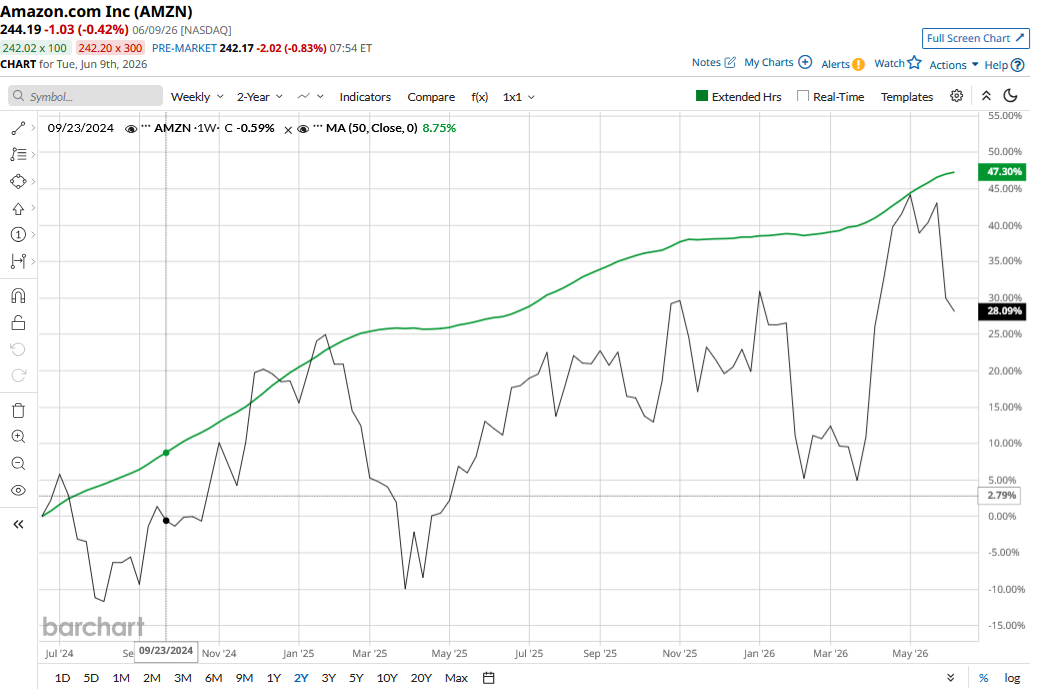

The artificial intelligence (AI) trade has cooled over the last few trading sessions, and high-flying names have seen a selloff. Specifically, Amazon (AMZN) stock is down by more than 10% over the last month and in correction territory.

Last month, I noted that I was on the sidelines on AMZN stock even as legendary fund manager and self-declared “Warren Buffett devotee” Bill Ackman doubled down on shares. With Amazon coming off its recent highs, let’s take a look at whether the stock is a buy now.

Why Has Amazon Stock Dropped?

There hasn’t been any specific company factor behind the recent correction in AMZN stock, and it has come amid the broad-based tech selloff. Notably, some investors might be liquidating their positions in tech names like Amazon to free up cash to buy the upcoming SpaceX initial public offering (IPO). Moreover, Amazon’s valuations did not leave much margin of safety, only adding fuel to the fire amid the tech selloff.

Amazon’s Valuations Look a Lot More Comfortable

Amazon’s forward price-to-earnings (P/E) ratio has since dipped to 31.6 times, which looks a lot more attractive even if it's not mouthwateringly cheap. AMZN stock does not have many near-term triggers apart from Prime Day later this month. Still, at these levels, long-term investors may want to consider adding shares.

There are a few reasons I believe Amazon is a reasonable buy at these levels, from growth in Amazon Web Services (AWS) and e-commerce to its chip business and margin expansion.

E-Commerce and AWS Growth

While the e-commerce industry’s growth in at least developed markets may have plateaued, there is still significant runway for Amazon's business to grow. Groceries and instant deliveries could be two key drivers for Amazon in the U.S., and the company has already become the second-biggest grocer in the country. In international markets, particularly in emerging economies, Amazon also has a lot of room to grow as consumers transition toward online shopping. Agentic AI — particularly Amazon’s in-house shopping assistant Rufus — should help accelerate the e-commerce platform’s growth as well. While there are lingering concerns over agentic AI threatening its lucrative digital advertisement business, Amazon has dismissed these concerns and is optimistic that the business will continue to do well in the new AI era.

Meanwhile, although AWS' growth in percentage terms has been trailing that of Microsoft (MSFT) and Alphabet (GOOGL), the business continues to add billions of dollars of incremental revenue every year. AWS is now a $150 billion annual revenue run-rate business with an order backlog of $364 billion, which does not include the $100 billion in commitments from Anthropic. Its AI business is also growing fast and running at an annualized pace of $15 billion. Amazon continues to look for new avenues to monetize its AI capex, and in a recent move, the company started selling its AI shopping tech to other retailers.

Amazon's Chip Business and Margin Expansion

While Alphabet has seen a rerating amid optimism over its chip business, Amazon's chip business is yet to see the same respect. However, this business continues to do well, and management has stressed that if it were a standalone company, its annual revenue would be $50 billion. Amazon’s Trainium3 chips, which it started shipping earlier this year, are almost fully subscribed. Much of the company's Trainium4 chips, which won’t be available broadly for 18 months, have also been reserved. In addition, Meta Platforms (META) has committed to using “tens of millions of Graviton cores."

Meanwhile, Amazon’s margins should expand over the next couple of years as the company uses AI to increase efficiencies and lower its cost base. During the first-quarter 2026 earnings call, Amazon said that at scale, Trainium chips would not only help the company cut down on its capex by “tens of billions of dollars” annually but also “provide several hundred basis points of operating margin advantage versus relying on others' chips for inference.”

Conclusion

Overall, I believe Amazon has built an enviable ecosystem that competitors would find hard to emulate. Prime is a case in point here; along with bringing subscription and ad revenues, it helps make the e-commerce platform even stickier. Prime members get extra discounts and no-cost shipping, and are more hooked to Amazon's ecosystem than other members, who are more likely to be lured by competitors. It's no wonder Prime members tend to spend a lot more than the average non-Prime member.

Amazon’s business is quite diversified, and while cloud accounts for the lion’s share of its operating profits, AMZN stock is a play on several other themes, including streaming and digital advertising. True, it is no longer the kind of growth engine it was a few years back. But the valuations also look commensurate with current realities, and I believe the stock can be nibbled at these levels.