(Please enjoy this updated version of my weekly commentary published August 8, 2022 from the POWR Growth newsletter).

As usual, we will start by reviewing the past 2 weeks…

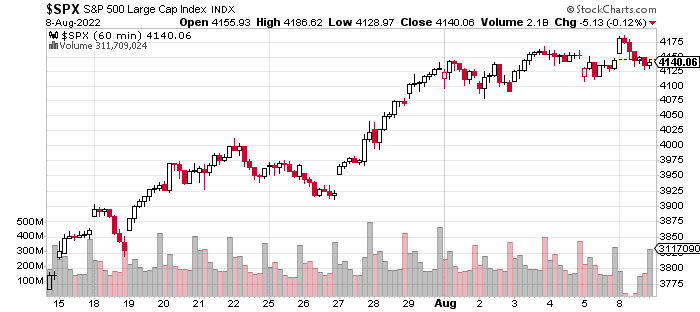

Here is an hourly, 3-week chart of the S&P 500:

Over the last 2 weeks, the S&P 500 (SPY) is up 4.4% as the bear market rally has continued. The gains have been pretty broad-based, but it’s fair to say that most of the strength is concentrated in the indices and what I call, ‘junk stocks’. This category includes GME, AMC, BBBY, etc, which are many of the most infamous meme stocks.

And, seeing these rocket higher proves that shorts are being squeezed as these are some of the most-shorted stocks in the market for the simple reason that they are some of the most egregiously overpriced stocks in the market.

Normally, I have more to add, because there is value to be derived from noting all the subtle developments under the surface that can often be at odds with the widely accepted market narratives.

This isn’t the case right now, because nothing has really changed from the last commentary 2 weeks ago. This is an explosive rally, marked by relentless buying. It’s either a short squeeze/bear market rally or the start of a new bull market. I believe this is the most important question at the moment.

Let me Make My Case for Why This is a Bear Market Rally…

First, let’s just note a couple of things: The market has done a 180 in terms of mood over the last 2 months. It’s yet another reminder that ‘sentiment follows price’.

At the lows, the prevailing narratives were sky-high inflation, a breakdown in growth stocks, a hawkish Fed, and a looming recession that was going to culminate in a significant decline in earnings.

After more than six months of triumph for the bears, they are on the retreat and rethinking their priors due to a nearly 20% rally for the Nasdaq and 15% gain for the S&P 500 (SPY) since the mid-June low. This is clearly the longest and most sustained rally in 2022 and is different in a qualitative and quantitative sense than previous advances in 2022.

This has also coincided with a better-than-expected earnings season and economic data which undermines the recession narrative and increases the odds of a ‘soft landing’. In addition, we had extreme levels of bearish sentiment, high levels of fund managers holding cash, and very low levels of stock ownership, specifically for tech stocks.

Given these developments, it’s a good time to delve into some individual issues to help us answer the million-dollar question.

Inflation

Possibly the most potent bearish threat facing the market in 2022 is inflation which kept creeping higher, reaching a level above 9% in the last month that hasn’t been seen in decades. High inflation means a hawkish Fed and higher short-term rates which is particularly negative for financial assets.

After all, why would investors take risks in terms of borrowing money or buying stocks if the risk-free rate of return is sufficiently attractive.

Adding to this risk were energy prices. These were climbing higher, entering 2022 but accelerated due to the Russia and Ukraine crisis. Nasty side effects have included soaring electricity prices and broad-based gains in oil, coal, natural gas, etc.

The issue is also conflated with national security and politics which means that the US and EU are willing to absorb these higher prices in order to oppose Russia’s incursion into Ukraine.

There doesn’t seem to be a resolution to the conflict between Russia and Ukraine, but there are some positive developments in terms of inflation. Leading indicators are pointing lower. Supply chain issues are being sorted out with retailers now discounting prices due to excessive inventories.

Auto production is returning to full capacity and the housing market has slowed in a major way. Most importantly, there is relief in terms of lower gasoline prices.

Growth Stocks

Growth stocks have been kind of a leading proxy for the market. Many of the frothiest, peaked in the spring of 2021, while others topped later in the year. This was well before the broader market which topped in January of this year.

Interestingly, the inverse took place recently as many growth stocks bottomed in mid-May and made a higher low in mid-June, even though the indices and most stocks made lower lows in June.

Currently, growth stocks have been the strongest performers during this rally. One reason is that moderating inflation is leading to lower rates which puts a bid underneath growth stocks. The other is that these stocks were heavily shorted which means that shorts are being squeezed.

It’s also worth noting that ‘junk’ growth stocks with no earnings and high valuations are leading the rally, while higher-quality growth stocks are lagging. This could be interpreted as a lack of institutional participation in the rally.

Recession + the Fed

In May and June, the calculus seemed simple. The Fed’s hawkishness and determination to crush inflation were going to result in a recession.

This scenario could still prove to be correct, but it’s clear that the economy is much more resilient than expected. This is evident in the recent jobs report which showed the US economy adding more than 500,000 jobs.

Additionally, the services segment of the economy expanded in July contrary to expectations. Finally, the hospitality & leisure segment of the economy continues to boom as indicated by earnings and economic data.

Earnings

Earnings are also inconsistent with an economy that is on the verge of a recession. Although, bears might counter by saying that Fed tightening is just beginning to impact the economy.

As Q2 earnings season nears an end, analysts are now expecting that S&P 500 (SPY) earnings will increase by 4.8%. This is better than the initial 4% estimate. It is true that the bulk of this earnings growth is coming from the energy sector as ex-energy earnings are set to decline by 1%.

Conclusion

I started off writing this almost 100% convinced that this is a bear market rally that will inevitably lead to lower lows. However, in putting this together and taking an objective view of the situation, I do think the bull case should be respected, but it hinges on one crucial development.

Basically, if inflation starts plummeting, but the economy stays resilient. In that case, this could be the nadir for earnings, and we could have a market with earnings growth and falling rates which would send stocks to new highs.

I think the possibility of this has gone from ‘implausible’ to ‘pretty unlikely’ over the last 2 months based on leading indicators of inflation rolling over, while earnings have remained stable despite six months of tighter policy. Another way to say this is that the economy is much less interest-rate sensitive than the market and most investors think.

However, just like the economy has proven to be more resilient than expected, something similar could happen with inflation.

This would mean the Fed keeps hiking and economic growth would be choked off, leading to a more significant contraction in earnings. This combination of higher rates and lower earnings would recreate the same dynamic that led to plummeting prices in the first half of the year.

So, I remain in the bear market rally camp. Mostly, because I see growth rolling over and more damage to earnings.

At the same time, we have caught the bulk of this move and our portfolio is up more than 10% since the market bottom despite an above-average cash position and some defensive picks which have underperformed.

Portfolio Strategy

We’re in pretty good shape, but I remain wary of what’s next. I’m also aware that profits on the long side in bear markets can quickly evaporate and stocks can easily plummet to new lows.

This was the thinking behind today’s trade alert. Further, our previous alerts have been about gradually increasing exposure. Now, I think it’s appropriate to slowly reduce exposure and increase our allocation to more defensive picks.

What To Do Next?

The POWR Growth portfolio was launched in April last year and since then has greatly outperformed just about every comparable index…including the S&P 500, Russell 2000 and Cathie Wood’s Ark Innovation ETF.

What is the secret to success?

The portfolio gets most of its fresh picks from the Top 10 Growth Stocks strategy which has stellar +49.10% annual returns. I then take the very best stocks from this strategy and tell you exactly what to buy & when to sell, so you can maximize your gains.

If you would like to see the current portfolio of growth stocks, and be alerted to our next timely trades, then consider starting a 30 day trial by clicking the link below.

About POWR Growth newsletter & 30 Day Trial

SPY shares were trading at $411.70 per share on Tuesday morning, down $1.29 (-0.31%). Year-to-date, SPY has declined -12.67%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Jaimini Desai

Jaimini Desai has been a financial writer and reporter for nearly a decade. His goal is to help readers identify risks and opportunities in the markets. He is the Chief Growth Strategist for StockNews.com and the editor of the POWR Growth and POWR Stocks Under $10 newsletters. Learn more about Jaimini’s background, along with links to his most recent articles.

After the Bear Market Rally What Comes Next? StockNews.com