/Facebook%20headquarters%20sign%20by%20Greg%20Bulla%20via%20Unsplash.jpg)

Meta Platforms (META) is one of the world’s largest technology conglomerates, headquartered in Menlo Park, California, and founded in 2004 by Mark Zuckerberg. The company operates through two segments: Family of Apps, encompassing Facebook, Instagram, WhatsApp, Messenger, and Threads, and Reality Labs, its augmented and virtual reality division.

With over 3.56 billion daily active users across its app ecosystem as of Q1 2026, Meta has evolved from a social networking pioneer into a full-stack artificial intelligence powerhouse, leveraging its massive data moat to drive AI-powered advertising monetization, agentic AI product development, and next-generation computing through its Meta Superintelligence Labs initiative.

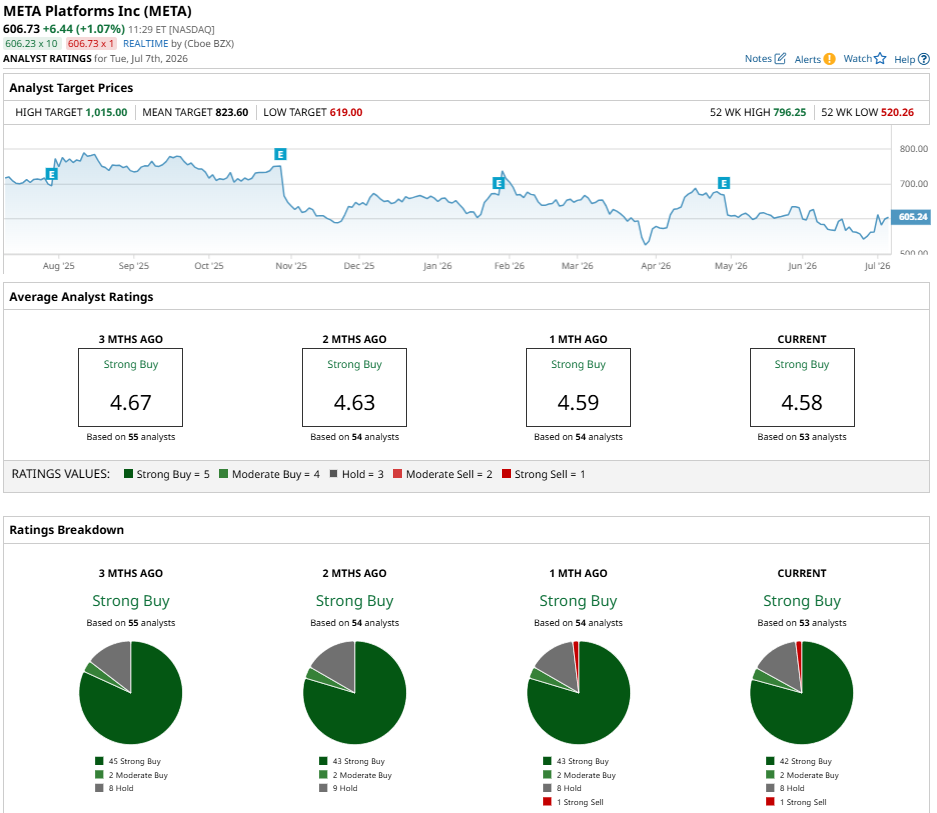

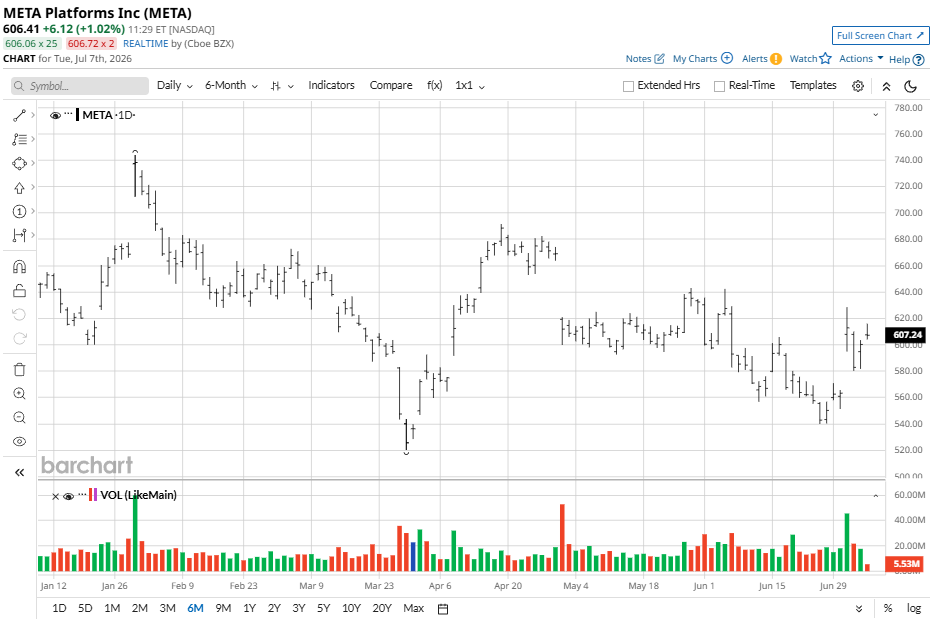

Meta Stock Lags in 2026

META shares were trading around $600 as of early July 2026, well below their 52-week high of $796.25 reached in August 2025, with a 52-week low of $520.26 recorded on March 27, 2026. The stock is down approximately 8.3% year-to-date.

Compared to the S&P 500 Communication Services ($SRTS) Index, which has broadly held up through 2026 on streaming and digital advertising tailwinds, META has meaningfully lagged despite posting its fastest revenue growth since 2021, a stark disconnect between price and fundamentals that has left the stock trading roughly 25% below its all-time high even as earnings surged.

Meta Earnings Beat Estimates

Meta reported Q1 2026 revenue of $56.31 billion, up 33% year-over-year, beating analyst expectations of $55.52 billion. GAAP EPS came in at $10.44, which included an $8.03 billion one-time income tax benefit. Excluding this, adjusted EPS was $7.31, beating the $6.79 analyst consensus. Advertising revenue reached $55.02 billion, with ad impressions growing 19% and average price per ad rising 12% year-over-year, underscoring the durable monetization strength of Meta’s AI-optimized ad platform.

Income from operations jumped 30.3% year-over-year to $22.87 billion, while operating margin came in at 40.6%. Gross margin held steady at 82%, consistent with the prior-year range, indicating no meaningful deterioration in core platform economics despite accelerating infrastructure investment. Family daily active people rose 4% to 3.56 billion, while net income surged 61% to $26.77 billion. Capital expenditures totaled $19.84 billion in the quarter alone, reflecting Meta's aggressive bet on AI compute infrastructure.

The single biggest talking point from the Q1 earnings call was Meta’s decision to raise its full-year 2026 capital expenditure guidance from between $115 billion to $135 billion to between $125 billion to $145 billion, citing higher component pricing, particularly for Nvidia (NVDA) GPUs and custom chips, as well as additional data center construction costs. Despite the capex increase, management reaffirmed that 2026 operating income will exceed 2025’s $83.28 billion, underscoring a strong commitment to profitability. Q2 2026 revenue guidance of between $58 billion and $61 billion came in above analyst expectations, implying continued strong growth of approximately 25% year-over-year at the midpoint.

Meta Partners With Samsung

Meta is reportedly in advanced talks with Samsung Electronics’ foundry division to design and manufacture its next-generation MTIA AI chips in a deal valued at over $6.5 billion, according to South Korean financial publication Sedaily.

The chips are expected to leverage Samsung’s cutting-edge 2nm process node, marking a significant strategic shift away from Taiwan Semi (TSM), which produced Meta’s first- and second-generation in-house AI accelerators. The potential deal aligns with Meta’s broader ambition to achieve 5GW of data center capacity by 2030, with the company targeting an aggressive six-month chip development and release cycle and planning to launch its third- and fifth-generation AI chips next year.

Meta is also collaborating with Samsung’s System LSI division on chip architecture, underscoring the depth of the partnership. The move reflects Meta’s accelerating push to reduce dependence on third-party processors like Nvidia GPUs and build a fully vertically integrated AI infrastructure stack.

What Does It Mean for Meta Investors?

Meta’s reported $6.5 billion Samsung chip deal signals a bold push toward AI infrastructure self-sufficiency, reinforcing the long-term bull case for a company already firing on all cylinders operationally.

Wall Street firmly agrees with a consensus “Strong Buy” rating across 53 analyst ratings, including 42 “Strong Buy,” 2 “Moderate Buy,” 8 “Hold,” and just 1 “Strong Sell” recommendation. The mean price target of $823.60 implies 35% upside from current levels, a striking premium that suggests analysts believe the market is significantly underpricing Meta’s AI-driven advertising dominance and vertical integration ambitions.