The Bank of Russia, the country’s central bank, has surprisingly announced a fixed price for buying gold with roubles. With a price of RUB5,000 (£45.12) for a gram of gold, to my knowledge it’s the first time that a nation’s currency has been expressed in “gold parity” since Switzerland decided to stop doing so in 1999.

Enacting gold parity was common practice by the world’s major powers for facilitating international trade payments in the era of the gold standard in the 19th and early 20th centuries. The same was true in a slightly different way during the Bretton Woods era from 1944 until 1971, which was when US President Nixon decided to end the system by removing the link between gold and the US dollar.

Putin’s new arrangement is envisaged, initially, to hold from March 28 to June 30. It is the latest in a series of rouble-related moves by the Russians, starting with the announcement on March 23 that they would only accept roubles for European gas instead of euros and US dollars. I predicted that Russia would at least extend this policy to oil, but it has gone further and signalled an intention to make it apply to all the commodities it exports (others include wheat, nickel, aluminium, enriched uranium and neon).

The main goal of these moves is to try to ensure the credibility of the rouble by making it more desirable in the forex market, though it also fits into longstanding attempts by Russia and China to weaken the US dollar’s dominance as global reserve currency (meaning it’s the currency in which most international goods are priced and which most central banks hold in their foreign reserves).

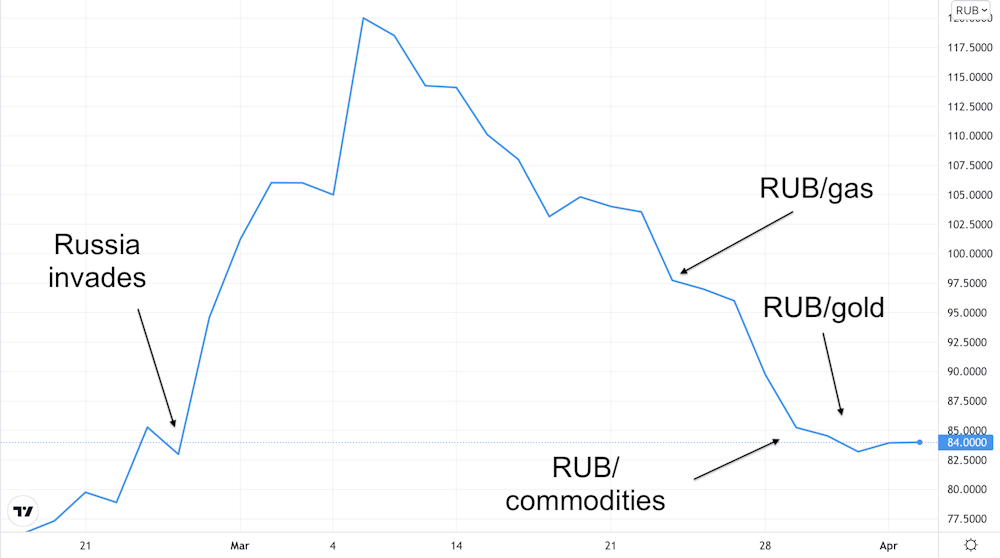

As one can see in the chart below, the rouble collapsed by more than 70% in late February and early March when western sanctions were imposed in response to Russia’s invasion of Ukraine (the collapse looks like a rise in the chart because it’s showing the number of roubles to the US dollar rather than the other way around).

Rouble/USD chart

After the big drop, the rouble recovered somewhat, which is typical in such situations (known in the literature as “exchange-rate overshooting”). However, the currency strengthened further after the roubles-for-gas announcement (no matter how serious or implementable the plan actually is – so far, there has been resistance to Putin’s new rules).

On the back of the gold announcement, the currency has continued to strengthen to about RUB83 to the dollar. As precious metals analyst Ronan Manly has said, this makes sense if you reflect that the market price of a gram of gold is currently about US$62 (£47.20). That’s fairly close to Putin’s announcement that 1 gram of gold equals RUB5,000, which effectively creates a gold-based exchange rate of RUB81 to US$1.

Previous gold-based systems

To give a sense of the similarities with the gold standard and the Bretton Woods system, let me draw a historical parallel. The UK’s Coinage Act of 1816 fixed the value of the pound sterling to 113 grains of pure gold, while the US Gold Standard Act of 1900 determined that the dollar should maintain a value of 23.22 grains of pure gold. Taken together, the two acts implied an official gold parity exchange rate of £1 = US$4.87.

It was similar during the post-war Bretton Woods era: 1 ounce of gold was said to be worth US$35, and all other currencies were fixed to and convertible into the US dollar. Gold was at the centre of the system as a way of making money credible.

Of course, attaching the rouble to a gold standard comes with certain “rules of the game” that Russia will have to abide by. It should be willing to exchange gold for roubles with anyone who wants to do so.

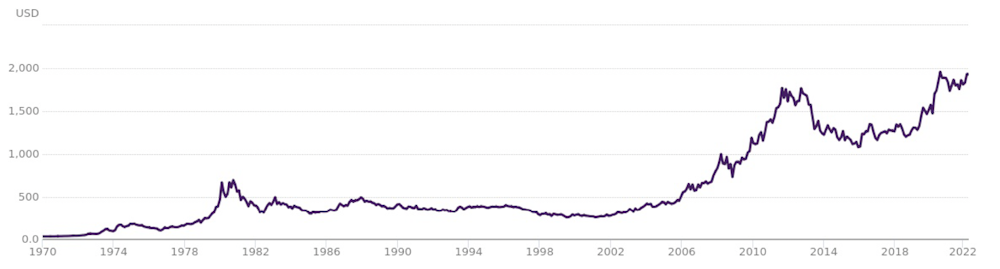

This was what the US did during the Bretton Woods era, and it led to the system’s demise: with US expenditure rising to wage the Vietnam war, dollar holders became increasingly nervous about the dollar’s value and sought to exchange it for gold.

Nixon’s unilateral decision to end convertibility was for fear that the US would run out of gold, which would have destroyed the credibility of the dollar. Since that decision, the world has moved to a system of floating exchange rates and the price of gold has steadily risen as world currencies have become weaker in relation to it. The system has effectively been supported by a deal that the Americans struck in the early 1970s to buy oil from the Saudis and give them military support in exchange for the Saudis using the dollars to buy US government bonds.

Gold price (US$/ounce)

The problem for Russia is that if it is willing to exchange roubles for gold, it could soon end up in a similar situation to the US circa 1971. Wars are an abnormal state of affairs which come with huge uncertainty: no reliable forecasts are possible, and markets are liable to overreact to new developments – particularly in the short term. If confidence in the rouble falls again, many investors might decide to withdraw gold from the central bank, which could be extremely destabilising for Moscow.

The viability of Russia maintaining a fixed rate of roubles for gold is closely related to what happens to demand for Russian energy. If the west can only slowly substitute away from its dependence on Russia’s oil and gas, then demand for roubles will help to keep the currency propped up (especially if the west does end up paying in roubles).

But if politicians listen to economists and immediately stop importing Russian gas, oil and other commodities, the rouble could fall dramatically – along with the whole Russian economy. As much as this would cause a further spike in prices and pain all round, it may be the most efficient and perhaps even safest way to induce Russia to stop the war.

Alexander Mihailov does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

This article was originally published on The Conversation. Read the original article.