Qualcomm (QCOM) is a big player in wireless chips and mobile technology. For a few months now, the company has been in the spotlight as chip stocks ride an AI-driven rally. Investors have watched Qualcomm’s 5G phone business struggle, but bets on data-center and AI growth have spiked interest in the stock.

This background leads into today’s catalyst: JPMorgan recently put QCOM stock on a "Positive Catalyst Watch” ahead of the company's Investor Day on June 24. The bank even raised its price target to $265, expecting new data-center goals.

In short, chip stocks are hot, Qualcomm stock has bounced hard, and now analysts are eyeing Investor Day for new growth targets.

Qualcomm Rides the AI Wave Across Multiple Markets

Qualcomm designs wireless chips and tech for smartphones, cars, Internet of Things (IoT), and more. Its Snapdragon processors power many smartphones and laptops. Qualcomm also owns a big patent-licensing business, Qualcomm Technology Licensing (QTL).

At CES 2026, Qualcomm also deepened its automotive AI partnership with Alphabet's (GOOGL) Google, integrating Snapdragon chips with Google Cloud to power the next wave of “software-defined” cars. In March, Qualcomm entered a new 6G industry consortium at Mobile World Congress (MWC), teaming with Amazon (AMZN), Google, Samsung, and others to develop AI-native 6G networks aiming for 2029 commercialization. On the consumer front, recent reports that Qualcomm will partner with OpenAI on smartphone AI chips are highlighting how hot the AI theme is.

That AI momentum has also helped fuel investor enthusiasm for the stock. Over the last 12 months, QCOM stock has climbed roughly 25%. The rally really took off this spring on AI and data-center hopes. So far in 2026, the stock is also trading about 17% higher, despite a 6% drop on June 9 and a 7% decline on June 10.

Even after its run, Qualcomm’s valuation still looks reasonable. Qualcomm trades at 21.4 times trailing earnings and roughly 4.8 times sales, compared to much higher industry averages for the broader semiconductor sector. In other words, QCOM stock is not richly priced on these metrics.

Wall Street Turns More Bullish Ahead of Investor Day

Qualcomm got a bump from Wall Street buzz after JPMorgan put QCOM stock on “Positive Catalyst Watch” ahead of the company's June 24 Investor Day. In a note, analyst Samik Chatterjee raised the firm's price target to $265 from $160.

JPMorgan expects Qualcomm to set ambitious data-center revenue goals. Specifically, the firm believes that Qualcomm’s data-center sales could hit more than $3 billion by fiscal 2027 and $35 billion by fiscal 2031.

The implication? JPMorgan believes the investor day may reveal faster growth targets than expected. Investors have reacted positively, viewing the news as a bullish sign that Qualcomm’s new AI/data center strategy might finally pay off.

Qualcomm Tops Q2 Earnings Estimate

Qualcomm topped estimates for the second quarter on both the top and bottom lines. Revenue was $10.6 billion in Q2, down about 3% year-over-year (YOY). Chip sales (QCT) came in at $9.1 billion, down 4% YOY, while licensing revenue (QTL) was about $1.4 billion, up 5% YOY. Automotive and IoT chip sales grew, but handset-related chip sales remained soft.

Net income was $7.37 billion, a huge jump of 162% YOY, thanks to a significant tax benefit. On an adjusted basis, net income was approximately $2.84 billion, down about 10%, while adjusted EPS was $2.65, down roughly 7% YOY.

CEO Cristiano Amon noted the mixed backdrop. The CEO pointed out that the industry is in a “period of profound transformation” with AI driving change. In his words, Qualcomm is “on track” in new areas. “We are equally excited by our entry into the data center, where a leading hyperscaler custom silicon engagement is on track for initial shipments later this calendar year," said Amon. "We look forward to providing an update on our growth initiatives, including opportunities in Data Center and Physical AI, at our Investor Day on June 24.”

Free cash flow was very strong. Operating cash flow was $7.41 billion, while capital expenditures were about $1.08 billion, implying roughly $6.3 billion in free cash flow. Qualcomm ended the quarter with $5.43 billion in cash and equivalents on hand.

For guidance, Qualcomm forecast Q3 2026 revenue of $9.2 billion to $10 billion, with non-GAAP EPS of $2.10 to $2.30. Analysts estimate fiscal 2026 revenue will be around $41 billion to $45 billion, with EPS of roughly $8, followed by a slight decline next year. Consensus forecasts currently project fiscal 2027 EPS of approximately $7.91, indicating flat to modestly lower earnings growth.

What Do Analysts Think of QCOM Stock?

Analysts are torn on Qualcomm’s outlook. Goldman Sachs initiated coverage this year with a “Neutral” rating, warning that handset headwinds could offset new growth. By contrast, JPMorgan is more upbeat as it lifted its target to $265 and put QCOM stock on watch ahead of Investor Day, citing potential data-center upside. RBC Capital has a $175 target, saying the valuation looks fair but that it’s awaiting more signs of data-center progress.

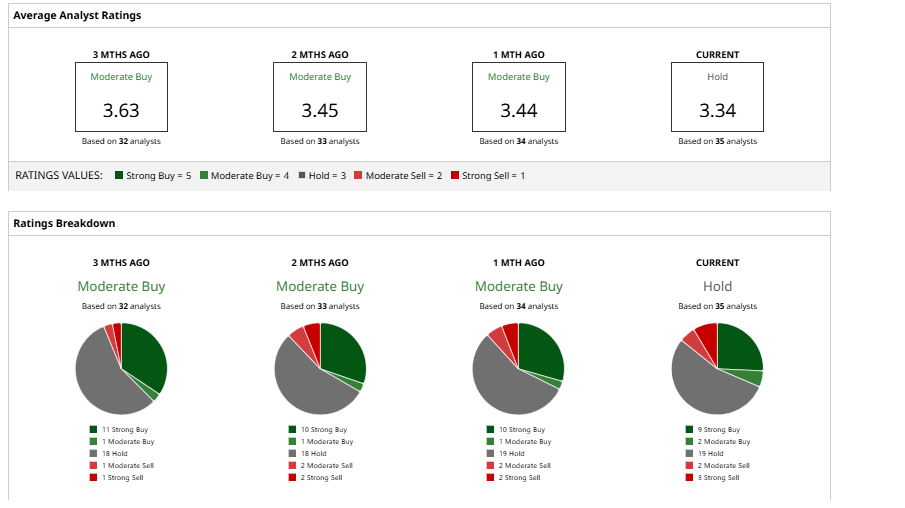

Overall, the consensus is a “Hold” rating based on 35 analysts. The average target of $184.83 implies around 8% potential downside risk from current levels.