The window for making the most of your savings this tax year is closing. As the final day of the 2022-23 tax year, April 5 is your last chance to make full use of this year’s tax allowances.

You can pay as much as £20,000 into a tax-free individual savings account (ISA) before this date. This annual limit has been frozen since 2017 and, unlike some other forms of tax relief, you cannot carry forward any unused ISA allowance.

So, it’s a case of use it or lose it, but why the rush to make the end of tax year deadline?

ISAs were introduced in April 1999. If you’d saved the maximum allowed each year since then you would have paid in over a quarter of a million pounds by now. And when you put your money in an ISA it grows free of income and capital gains tax, and can be withdrawn without any tax charges. If you were to add in the tax-free interest and investment growth you can get with an ISA, maybe you could even have become one of an estimated 1,480 ISA millionaires.

If you have missed that chance, there’s no reason why you can’t catch up on some tax-free savings now. And by opening an account before the April 5 deadline, you could still make use of this year’s allowance and then continue contributing afterwards under next year’s. So what do you need to know?

The different types of ISA

There are several types of ISA, and you can choose to pay into just one type each year, or open a mixture and spread your annual allowance among them. The most popular are cash ISAs, where your money goes into a savings account with a bank, building society or the government-backed National Savings & Investments (NS&I).

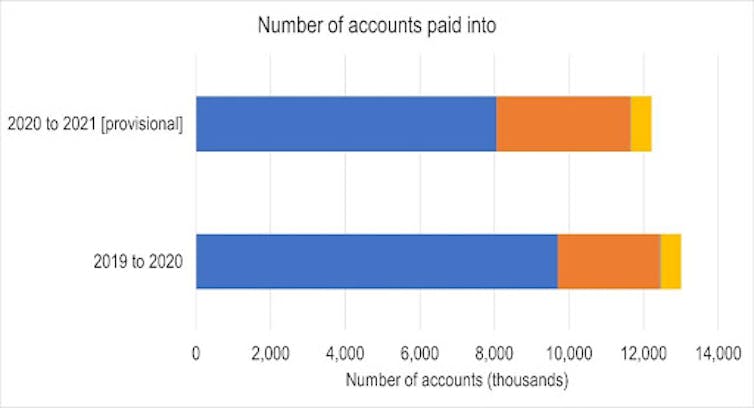

As the charts below show, in 2020-21 (the most recent tax year for which data is available), cash ISAs accounted for two-thirds of the 12 million ISA accounts people paid into, and half of the value of the money they paid in.

How many ISAs are being used?

How much is going into ISAs?

If you are comfortable taking a bit more risk – with the potential to make more of a return – a stocks and shares ISA allows you to invest your tax-free savings in the stock market. These kinds of accounts are offered by fund managers and investment platforms, for example. They are usually set up as an “empty box” that you fill up with funds, company shares, corporate and government bonds, and similar investments from the selection offered by your ISA provider. Unlike cash ISAs, you will have to pay various fees to the provider.

Innovative finance ISAs also involve risk. These accounts offer a way to access the “peer-to-peer lending” market. This is where you lend your savings directly to individuals or businesses through an online platform. While this can seem like an interesting alternative to a bank or building society deposit, it carries a higher risk of losing your money and there is no protection against losses as there would be with a savings account.

In 2017, the government also introduced lifetime ISAs (LISAs) as a way for people aged 18 to 39 to build up savings. Unlike other types of ISA, the government adds an annual 25% bonus to the amount you have saved over the year in a LISA. You can save up to £4,000 annually in these accounts, so with the extra £1,000 from the government you could sock away up to £5,000 every year until age 50.

The money you pay in to a LISA forms part of your overall £20,000 ISA allowance and you can only withdraw your money tax-free from age 60, although you can take it out early to buy your first home. This makes LISAs useful for retirement planning or for first-time buyers. You can still withdraw your money for other reasons, but there is a 25% withdrawal charge – which claws back the government bonuses and includes a 5% penalty charge on top.

Should I open an ISA?

If you don’t mind locking up your money until at least your mid-50s, saving through a pension plan could be a better choice because the tax reliefs for pensions are more generous than those for most ISAs. However, LISAs can be just as tax-efficient if you pay income tax at no more than the basic rate.

And ISAs are just one of several government tax concessions for savers and investors. In fact, you may have questioned whether they were worth opening given that some other allowances seemingly do the same job:

- a personal savings allowance lets you have up to £1,000 a year (for basic-rate taxpayers) or £500 (for higher-rate taxpayers) of interest tax-free

- a dividend allowance allows you up to £2,000 of share dividends tax-free

- the capital gains tax allowance stands at £12,300 for 2022-23.

But while your ISA will be forever, these tax concessions only apply on a year-by-year basis; they can – and do – change.

In the government’s 2022 autumn statement, UK chancellor Jeremy Hunt announced that the dividend allowance will be halved from £2,000 to £1,000 from 6 April 2023, and cut again to £500 from April 2024. Similarly, from this April the capital gains tax allowance will be reduced to £6,000 and then fixed at £3,000 from April 2024 onwards.

Read more: Autumn statement 2022: experts react

In contrast, once you have paid money into an ISA, the returns remain tax-free indefinitely. That makes a strong case for getting your skates on and using your 2022-23 ISA allowance before it runs out on April 5.

Jonquil Lowe is affiliated with the Women's Budget Group.

This article was originally published on The Conversation. Read the original article.