New York-based Omnicom Group Inc. (OMC) offers advertising, marketing, and corporate communications services and provides a range of services across media and advertising, precision marketing, public relations, healthcare, branding and retail commerce, and more. The company has a market cap of $23.5 billion and is expected to release its Q1 2026 earnings soon.

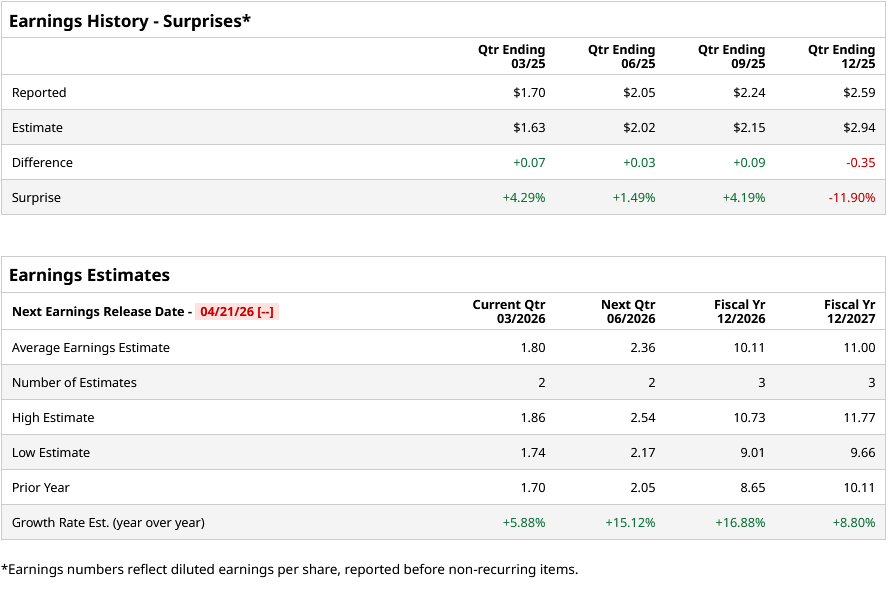

Ahead of this event, analysts anticipate the company to generate earnings of $1.80 per share, representing an increase of 5.9% from $1.70 per share reported in the same quarter last year. The company has surpassed the Street’s bottom-line estimates in three of the past four quarters, while missing on one occasion.

For fiscal 2026, analysts expect the company to report an EPS of $10.11, indicating a 16.9% rise from $8.65 reported in fiscal 2025. Moreover, its EPS is expected to rise nearly 8.8% year over year (YoY) to $11 in fiscal 2027.

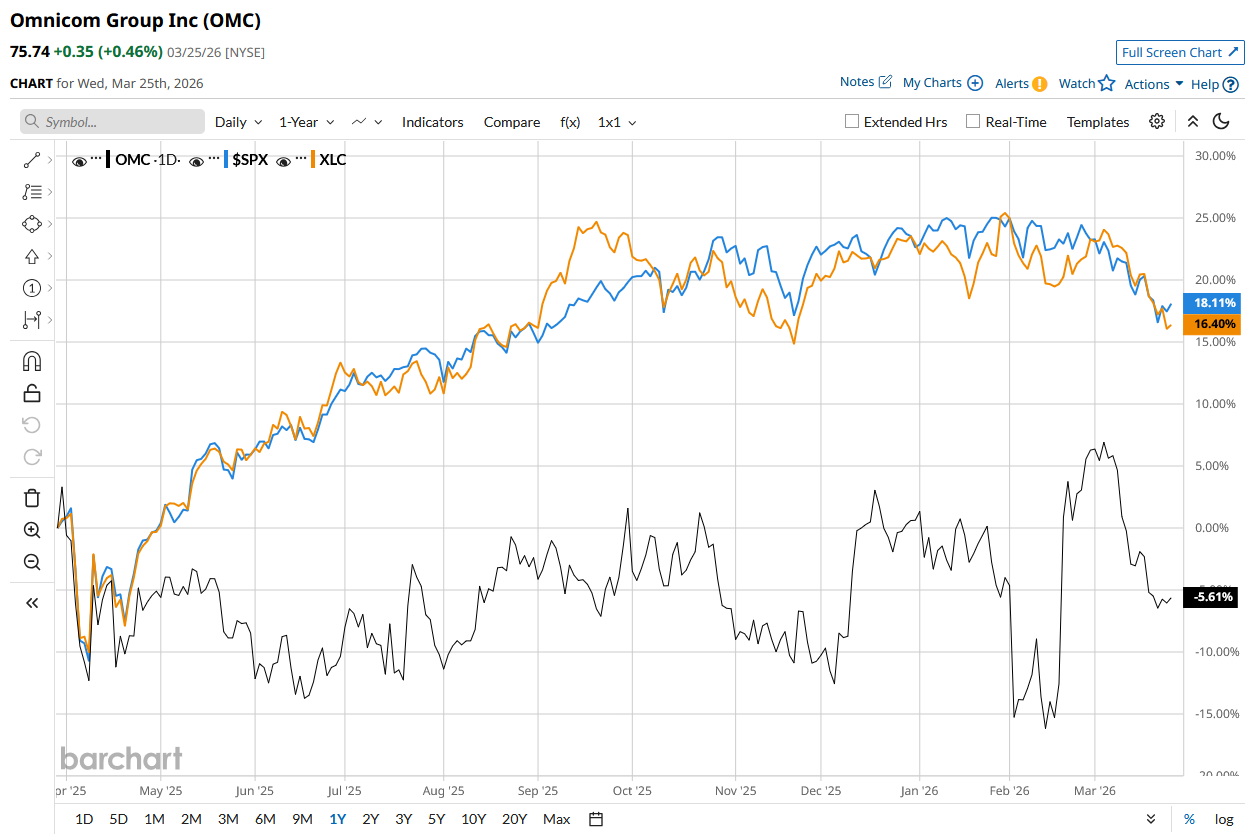

OMC stock has declined 5.8% over the past 52 weeks, underperforming the S&P 500 Index’s ($SPX) 14.1% rise and the State Street Communications Select Sector SPDR ETF’s (XLC) 11.5% rise during the same time frame.

On Feb. 19, OMC stock surged 15.4% following the release of its Q4 2025 earnings. The company’s revenue grew 27.9% from the prior year’s quarter to $5.5 billion, primarily driven by constant-currency revenue growth and the inclusion of one month of revenue attributable to its acquisition of The Interpublic Group of Companies, Inc. Moreover, the company’s adjusted EPS also grew 7.5% from its year-ago value to $2.59 as well.

Analysts’ consensus opinion on the stock is moderately bullish, with a “Moderate Buy” rating overall. Among the 10 analysts covering the stock, five are recommending a “Strong Buy,” four advise a “Hold,” and the remaining one analyst gives a “Moderate Sell” rating for the stock. OMC’s average analyst price target is $100, indicating an upside of 32% from the current levels.