With a market capitalization of approximately $13.3 billion, Align Technology, Inc. (ALGN) has established itself as one of the leading names in digital orthodontics. The Tempe, Arizona-based company develops and markets the Invisalign clear aligner system, Vivera retainers, and iTero intraoral scanning systems, providing advanced digital treatment solutions for both patients and dental professionals worldwide. Operating through its Clear Aligner and Imaging Systems segments, Align has helped reshape the orthodontic industry by replacing traditional braces with technology-driven alternatives.

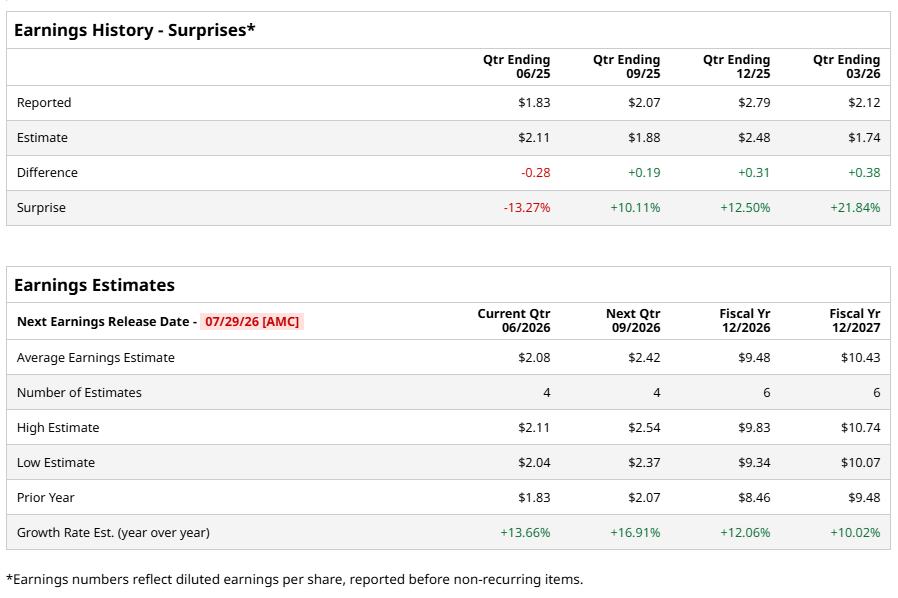

Investors are now turning their attention to the company’s next major catalyst. Align Technology is scheduled to report its fiscal second-quarter 2026 earnings after the closing bell on Wednesday, July 29. Ahead of the event, analysts forecast the company to deliver a profit of $2.08 per share, representing a growth of 13.7% from $1.83 per share in the same quarter last year. The company has generally maintained a solid earnings track record, beating analysts’ bottom-line expectations in three of the past four quarters while falling short on one occasion.

Looking beyond the upcoming quarter, analysts remain optimistic about Align’s long-term earnings trajectory. For fiscal 2026, Wall Street expects the Invisalign maker to generate EPS of $9.48 per share, reflecting a 12.1% increase from $8.46 in fiscal 2025. That momentum is projected to continue into fiscal 2027, with earnings expected to climb another 10% year over year (YOY) to $10.43 per share.

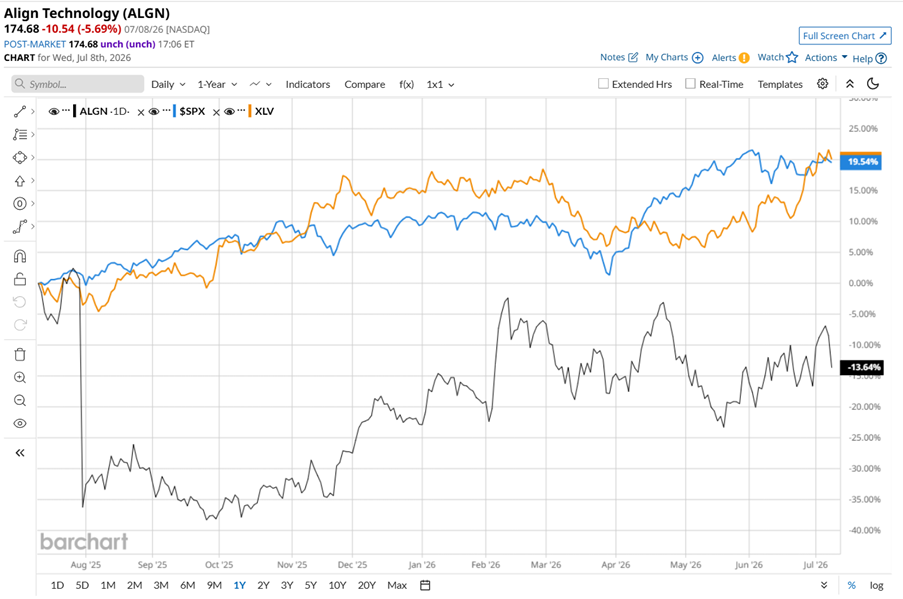

Despite those encouraging earnings forecasts, Align’s stock performance has told a different story. Shares have declined 10.6% over the past 52 weeks, sharply underperforming the broader S&P 500 Index’s ($SPX) 20.2% rise during the same period. The stock has also trailed the State Street Health Care Select Sector SPDR ETF’s (XLV) 20.3% return over the past year.

Align Technology has lagged the broader market not because its business is broken, but because the dental industry has been stuck in a slow recovery. Throughout 2025, patients continued delaying expensive elective procedures like clear aligners as inflation, economic uncertainty, and cautious consumer spending weighed on demand. Although dental visits and aligner sales have started showing early signs of improvement, the recovery has been gradual rather than convincing.

Analysts expect a more stable 2026, but stability alone is not enough to excite investors. Until discretionary dental spending meaningfully rebounds and growth accelerates, Wall Street is likely to remain cautious on Align Technology, leaving the stock trailing the broader market.

Even so, Wall Street has not lost confidence in Align’s longer-term prospects. ALGN stock currently carries a consensus “Moderate Buy” rating. Out of 15 analysts covering the stock, opinions include 10 “Strong Buys,” four “Holds,” and one “Moderate Sell.” The average analyst price target is $206.57, which suggests potential upside of 18.3% from current levels.