/Bank%20Of%20America%20Corp_%20sign-%20by%20J_%20Michael%20Jones%20via%20iStock.jpg)

Bank of America Corporation (BAC), headquartered in Charlotte, North Carolina, provides banking and financial products and services. With a market cap of $379.9 billion, the company offers saving accounts, deposits, mortgage and construction loans, cash and wealth management, certificates of deposit, investment funds, credit and debit cards, insurance, mobile, and online banking services.

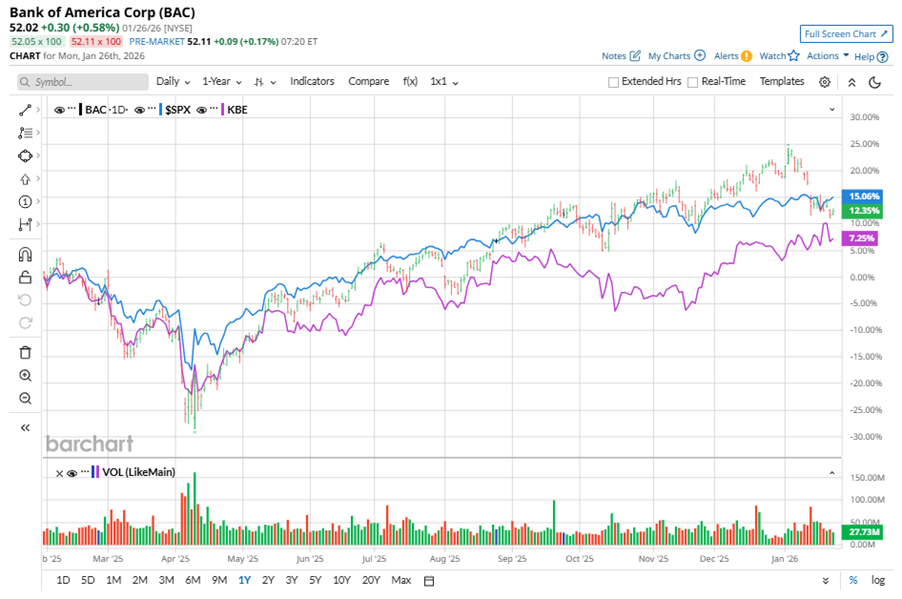

Shares of this banking giant have underperformed the broader market over the past year. BAC has gained 11.8% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 13.9%. In 2026, BAC’s stock fell 5.4%, compared to the SPX’s 1.5% rise on a YTD basis.

Narrowing the focus, BAC’s outperformance is apparent compared to SPDR S&P Bank ETF (KBE). The exchange-traded fund has gained about 8.7% over the past year. However, the ETF’s 4% returns on a YTD basis outshine the stock’s losses over the same time frame.

BAC's underperformance is due to sector-wide pressure triggered by reports of a proposed 10% cap on credit card interest rates, raising concerns about squeezed profitability for consumer banks and sparking a sell-off in financial stocks.

On Jan. 14, BAC shares closed down by 3.8% after reporting its Q4 results. Its EPS of $0.98 beat Wall Street expectations of $0.96. The company’s revenue was $28.4 billion, topping Wall Street forecasts of $27.5 billion.

For the current fiscal year, ending in December, analysts expect BAC’s EPS to grow 13.1% to $4.31 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

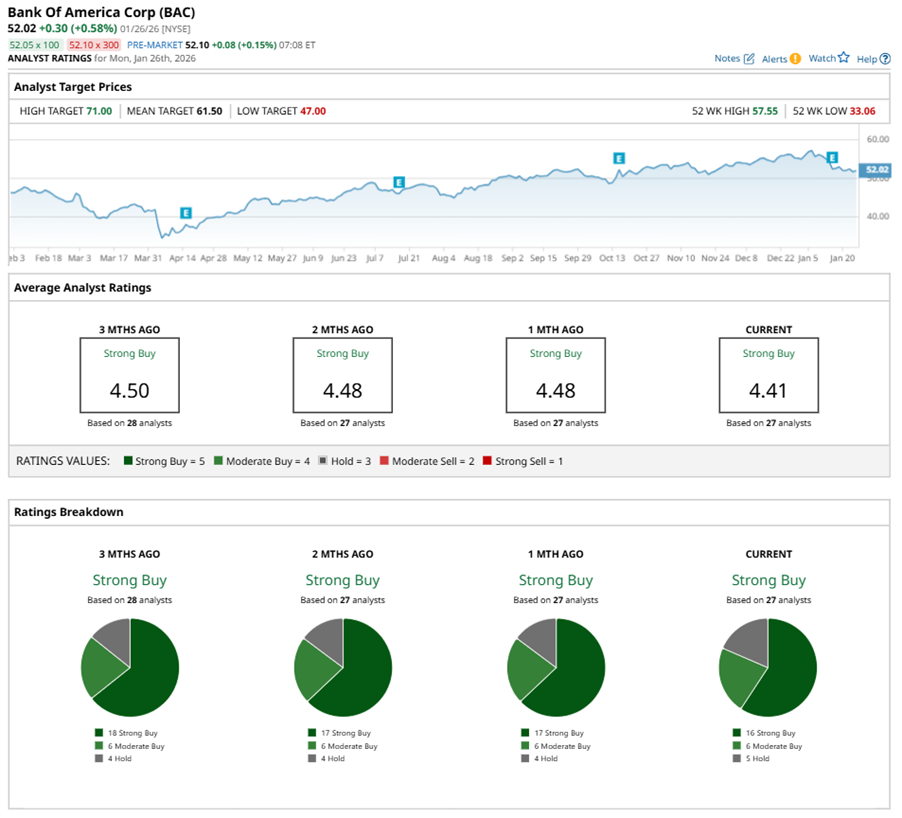

Among the 27 analysts covering BAC stock, the consensus is a “Strong Buy.” That’s based on 16 “Strong Buy” ratings, six “Moderate Buys,” and five “Holds.”

This configuration is less bullish than a month ago, with 17 analysts suggesting a “Strong Buy.”

On Jan. 15, Morgan Stanley (MS) kept an “Overweight” rating on BAC and lowered the price target to $64, implying a potential upside of 23% from current levels.

The mean price target of $61.50 represents an 18.2% premium to BAC’s current price levels. The Street-high price target of $71 suggests an upside potential of 36.5%.