Child labor violations are growing

More and more child labor violations are being reported nationwide, including instances of children working in hazardous occupations. What’s the data behind this trend? What penalties do companies face for violations? Get the facts in this article.

- Child labor violations have generally fallen since the early 2000s. However, from 2015 to 2022, the number of minors employed in violation of child labor laws rose by 283%, according to the Labor Department’s Wage and Hour Division.

- In 2022, 3,876 children were illegally employed, compared to 1,012 in 2015. The number of minors unlawfully employed in hazardous occupations increased by 94% over that same time.

- A recent Labor Department investigation found child labor violations across eight states with over 100 employees — some as young as 13 years old — working 13-hour overnight shifts in meat processing facilities.

- Under the Fair Labor Standards Act, employers caught violating child labor laws are subject to civil penalties. In 2022, employers paid $4.4 million in civil penalties for child labor violations, nearly $1 million more than the year prior. Fines collected from child labor cases rose by roughly 215% from 2015 to 2022.

Despite this recent uptick, more minors were involved in child labor violations in 2001 than in any other year in recent history. See the numbers on how things have changed.

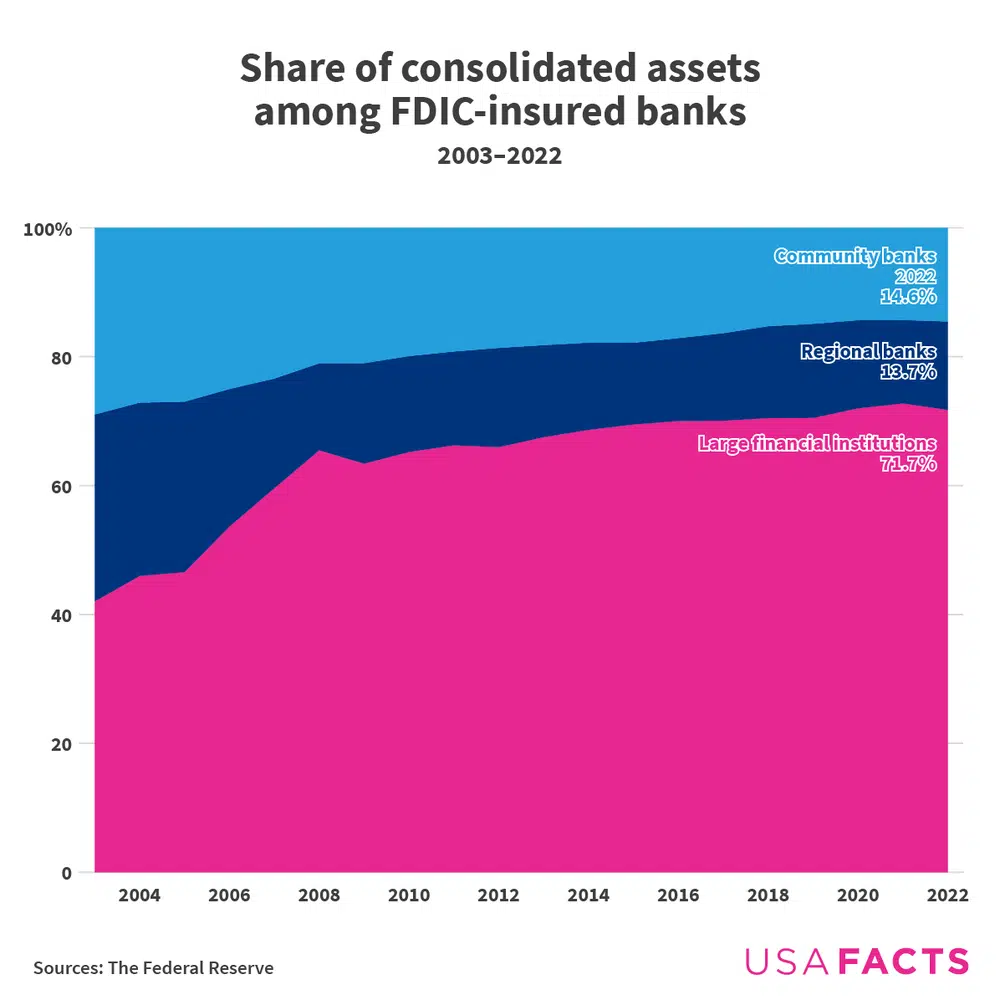

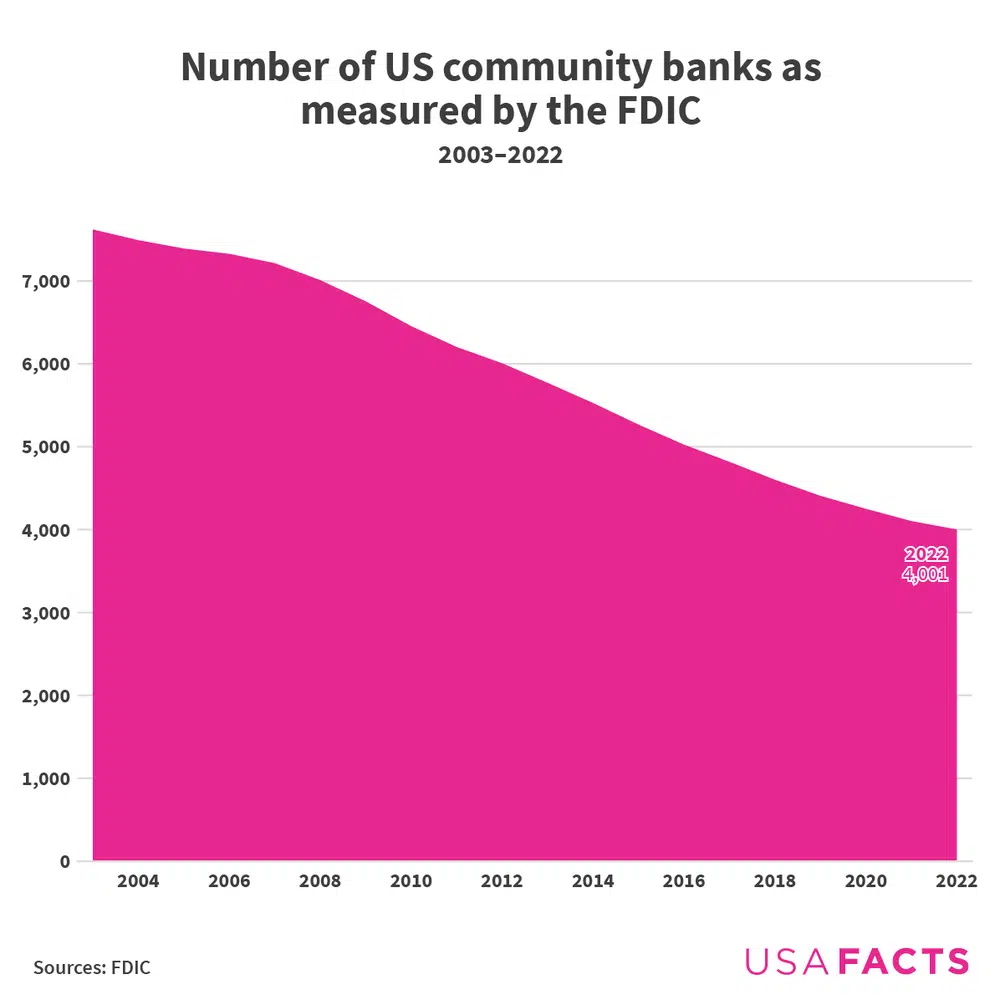

What community banks mean for the economy

Community and regional banks play a key role in the banking industry, serving local and interstate communities with financial services tailored to their specific needs. However, their market share has been declining while the share of large banks has grown. What are the reasons behind this? Here’s what the data says.

- The Federal Reserve defines community banks as those with less than $10 billion in assets. Regional banks have total assets between $10 billion and $100 billion. Any bank with combined assets of $100 billion or more is considered a large financial institution.

The nation has 4,001 community banks with 27,511 branches and 134 regional banks with 13,109 branches. In contrast, 31 large financial institutions have 30,570 branches nationwide.

- While regional banks have grown by about 50% over the last two decades, community banks declined by nearly half over the same period. This decline is attributed to mergers and acquisitions, bank failures, and higher regulatory costs.

- Community banks tend to outperform larger banks during periods of economic stress, such as the 2008 financial crisis and the pandemic. They often specialize in small business lending and are associated with local development.

Learn more about the role community banks play in American society. Plus, here’s an explanation of bank failures and how often they happen.

Data behind the news

- The US Supreme Court recently struck down a Biden administration plan to wipe out billions in student loan debt. But how much do Americans owe in student loans?

-

USAFacts is now on Threads! Join us for real-time conversations about data that matters to you.

- Up to date on USAFacts’ newest articles? Test your knowledge of them here.

One last fact

The federal government defines poverty based on family size and income. In 2021, a family of four was considered impoverished if its annual household income was $26,500 or less before taxes. (The median household income for a family of four was $90,657 for 2020–2021.) The government annually adjusts the official poverty measure to account for inflation.