Good-bye and have a good weekend. We’ll be back on Monday.

Closing summary

Disappointing industrial production and construction data have raised the prospect of slower economic growth in Britain, pushing the pound to five-year lows against the dollar. The currency is already under pressure amid concerns that the 7 May election will produce a hung parliament.

- The pound has lost more than a cent against the dollar to $1.4650, but is slightly down against the euro at €1.3791.

- The FTSE 100 index is on track for a new record closing high

- European shares have risen to their highest level since the millennium, helped by the weak euro which is benefiting exporters. The FTSEurofirst 300 index of top European shares is currently up 0.65% at 1640.14.

- French industrial output was flat in February while Spanish production rose 0.6%

FTSE 100 index near record high

The FTSE 100 index of leading shares is trading nearly 40 points higher at 7053.63, a 0.55% gain. It is inching closer to an intra-day record high of 7065.o8 points reached in March.

The FTSE is also on track to set a new all-time closing high, beating the 7,037.67 reached on 23 March. Last month the index finally broke through the 7,000 barrier – a level not seen since the dotcom boom of 1999.

Drugmaker Shire is still the biggest riser, up 5.2%, after positive news on its dry-disease treatment Liftegrast. Housebuilders Barratt and Taylor Wimpey were lifted by upgrades by broker Jefferies.

Meanwhile fellow pharmaceutical firm AstraZeneca is bucking the trend, with its shares down 2% at one stage, the top faller on the FTSE, after staff at the US top health regulator said its diabetes drug Onglyza appears to be associated with an increased rate of death. A clinical study in 2013 found that the drug might be linked to heart failure.

Updated

Some more thoughts on the slide in the pound. With inflation expected to be zero or negative in Tuesday’s data, and analysts expecting a prolonged undershoot of the 2% inflation target, a fall in sterling should be welcome from an inflation perspective.

It should also help exports, ease the pressure on Britain’s current account deficit and help rebalance the economy.

Some election pundits argue, however, that the fall in sterling is a bad thing, reflecting loss of faith in the UK. It’s also bad for holidaymakers, obviously.

Updated

GE sells bulk of $30bn property portfolio to Blackstone, Wells Fargo

Also on the corporate front, General Electric confirmed it plans to sell the bulk of its $30bn property portfolio over the next couple of years, as it returns to its industrial roots. GE shares jumped 7% in premarket trading after the company also unveiled a big share buyback plan.

GE is selling most of its property assets to private equity giant Blackstone and US bank Wells Fargo in a $23bn deal. It hopes to offload an additional $4bn of commercial real estate to unidentifed buyers.

Updated

On stock markets, the FTSE 100 index is about 24 points higher at 7039.44, a 0.3% rise. Germany’s Dax has climbed nearly 1.6% to 12,357.37 while France’s CAC is 0.4% ahead at 5232.

Drugmaker Shire has been leading shares higher in London all day, jumping more than 5% to £25.06, near all-time highs. The stock has been boosted by news that one of its drugs – Liftegrast for dry eye disease – would be fast-tracked by US regulators. The medicine has been granted a priority review to speed up the target time to market to eight months, rather than 12.

The pound has fallen even lower, hitting $1.4603 at one stage.

GBPUSD survives the first attempt on 1.4600 - http://t.co/xVtTk8qyNG

— ForexLive (@ForexLive) April 10, 2015

Updated

Looking ahead to next week, the European Central Bank will hold its first meeting on Thursday since its bond-purchase programme started.

Nick Kounis, head of macro and financial markets research, says:

President Draghi’s big challenge in the press conference will be to sound positive about the impact of QE and the outlook for the economy without sounding like it is going ‘too well’. He is likely to make it clear that the central bank plans to continue asset purchases to at least September 2016 and we think he is likely to successfully dismiss talk of tapering or exit. This task will become much more challenging later in the year, and certainly in 2016, as the economy continues to gain momentum.

Q1 GDP figures to show weaker growth, days before the general election?

The first-quarter GDP figures are out on 28 April, a week before the general election. Victoria Clarke, economist at Investec, has crunched today’s numbers.

The sogginess of construction sector output remains an ongoing puzzle. It has clearly been at odds with the PMI survey data. Furthermore, there is no one weak sector with the ONS numbers pointing to relatively broad based weakness... Hence we are left scratching our heads as to whether this is reflective of the true output of the sector. Even so, clearly it is these numbers which provide the construction sector’s contribution to first quarter output; even if construction output rebounds by 2½% in March, we would still be looking at a 2.5% decline over Q1 altogether, following on from the hefty 2.2% Q4 drop.

The ‘official’ story for the UK industrial sector is similarly disappointing news for the prospects for first quarter output. Indeed, allowing for a ½% rise in industrial output in March, we would still only see output of the sector standing around flat over Q1 overall. Note however that this is not due to weakness across the industrial sector overall but is led by a 3.8% m/m drop in oil and gas output. Indeed, the ONS points to the reduction in oil and gas output at some North Sea terminals compared to a year ago, with the contribution of crude/petroleum and natural gas to the February industrial sector figures at some -0.37ppts (i.e. sizeable drag). The picture for the UK’s manufacturing sector was a better one, with output meeting consensus expectations and recording growth of +0.4% month to month (Investec forecast +0.6%). With the UK manufacturing PMI having firmed into March, this leaves us optimistic that, oil and gas aside, the prospects for the UK’s manufacturing sector are far from grim.

What this all means, we suspect, is that whilst a softer Q1 GDP print than Q4’s +0.6% looks to be firmly on the cards now, short of some very heavy lifting from the UK’s dominant services sector in February and March, this isn’t necessarily a story of a UK recovery coming off the tracks. Indeed, the underlying position of UK manufacturers looks respectable and survey data on the strength of UK services output suggests the sector’s prospects have firmed as we have headed through the quarter.

For Mr Cameron however this may be of little comfort, with the first quarter UK GDP figures due just over a week before the general election; with a key strand of the Conservative’s policy case built on their economic performance the 28 April figures could prove to be important.

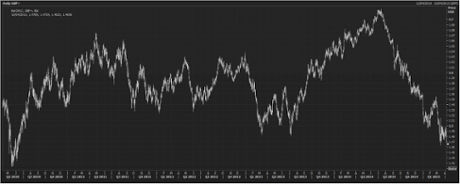

Here’s a chart showing the pound’s movements against the dollar over the last five years.

More reaction to today’s UK factory and industrial output data from the British Chambers of Commerce. David Kern, the lobby group’s chief economist, says:

February figures showed a modest improvement after last month’s declines but underlying industrial growth remains weak and so manufacturers will continue to face serious challenges. However, in the face of these difficult conditions our manufacturing sector has coped well with the rise in the pound against the euro over the past year and the sector has largely succeeded in maintaining its skills base during the recession. It is a credit to their strength and resilience.

While UK growth is likely to remain dependent on the healthy and dynamic services sector for the foreseeable future, there is no room for despondency. The manufacturing sector is in a good position to move forward when world circumstances improve, but only if low interest rates are maintained.

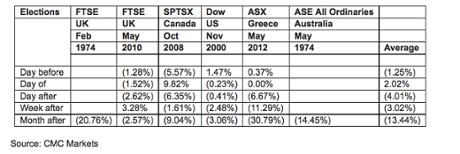

Could a hung Parliament leave UK markets swinging?

Ahead of the tightly fought UK general election on 7 May, Colin Cieszynski and Michael Hewson from CMC Markets look at how a hung parliament result could affect the markets.

The race to win the election looks like it could go right to the wire with both the Conservative and Labour party neck and neck in the polls, convincing just 35% of the electorate each.

Stock markets hate uncertainty, and the potential for an unstable government following a close race could impact the FTSE and the pound in the days and weeks following a close race until a workable solution is found, if indeed there is one. A scenario where one of Labour or the Conservatives wins the popular vote and one wins the most seats could add to the potential mess and uncertainty.

To get an idea of what a hung parliament could mean for the FTSE and the pound, the market strategists have taken a look at several previous close elections from around the world which ended up creating more questions than they answered.

Stock Market Performance following selected elections with contested results

For each of the elections in this century daily returns for the main local stock market index around the election date were analysed while for the two from the 1970s daily data was unavailable so monthly numbers around the election were used to approximate instead.

Regardless, the results speak for themselves. Elections from five different countries that ended in a muddle were followed by immediate selloffs that only deepened as it became clear that there was no easy or quick resolution to the problems. In all six cases, the local market was down a month later, and in half of them, the local market was down more than 10%.

The analysts conclude:

This suggests that should the UK election end in an indecisive result and wrangling over a coalition government drags, the FTSE and sterling could become increasingly vulnerable through May.

In Britain’s construction industry, activity slowed across all areas with the exception of new projects in the public housing sector, according to the ONS, which indicated that housing associations were among the few organisations to expand their output in February. The broader measure of ongoing activity showed that all parts of the construction industry declined, including public housebuilding , private housebuilding, civil engineering and infrastructure work.

More encouragingly, factory output improved, but mainly in the car industry, which recently reported its best production output this century. Nevertheless, factory output in the first quarter is so far running 0.2% below the fourth quarter of last year.

US Treasury warns of hung parliament

The BBC’s economics editor Robert Peston writes:

So the US Treasury has noticed there is a general election happening in Britain. This is what a report sent yesterday to Congress said about us:

“The potential for difficult coalition talks, and subsequently the design and implementation of economic policy, is broadly perceived as a material downside risk for businesses and investors.”

Or as I mentioned earlier this week, sterling will continue to take the strain (the pound will fall) if investors become more concerned that weak and directionless government will be the consequence of the poll on 7 May.

Broadly, however, the US Treasury paints a positive picture of trends in the British economy - except for the widening to a record level in the current account deficit, the huge imbalance between the money we make from the rest of the world and what we pay the rest of the world (which I’ve been banging on about for many months).

Updated

Chris Williamson, chief economist at economic survey compiler Markit, concurs.

Weaker than expected construction sector and industrial production numbers point to the economy having slowed at the start of the year. The data provide further evidence to support the case of interest rates to remain on hold, and will add to chatter that policy may even need to be loosened further.

However, more up-to-date survey data suggest the economy is showing signs of reviving again, which suggests that the next move in interest rates will be a rise, but that there’s little likelihood of rates being hiked this year.

UK GDP growth likely to have slowed in first quarter

Alan Clarke, head of European fixed income strategy at Scotiabank, says GDP growth in the first quarter, between January and March, is looking weak after the disappointing industrial and construction data.

This morning’s UK data were disappointing again, with construction and industrial production both weaker than expected.

January saw all 3 components of GDP by output shrinking. So we were looking for a rebound in February to get things back on track for a respectable Q1 GDP…

…but we didn’t get the rebound

There has been no growth in industrial production so far in Q1 and construction has shrunk by 3.5%.

Unless we get big revisions to these data, or a massive jump in services output in February and March, then GDP growth of just 0.4% q/q (down from 0.6% q/q in Q4) is looking like the most likely outcome.

Yesterday’s weak trade data would seem to back this up from the expenditure side too.

This is not going to make pleasant reading for the coalition government in the final days of the election campaign.

Updated

The pound has fallen to a five-year low of $1.4623.

Against the euro, sterling is flat at €1.3805.

Updated

Construction output down 0.9% in February

Britain’s construction industry fared even worse, with output down 0.9% in February, wrongfooting City economists who had pencilled in 2% growth. In January, output slid 2.5%.

The pound is heading towards a five-year low of $1.4635 after disappointing industrial production data, which do not bode well for overall economic growth. A sharp fall in oil and gas output in February is to blame for the small (0.1%) rise in industrial output.

The ONS said the 12% annual decline in oil and gas production in February was the biggest fall since August 2013.

Updated

However, markets are taking a dim view of the data. Sterling has dipped to $1.4669 from around $1.4685 before the figures were released.

Updated

Here is some instant reaction to the UK data. David Richardson, head of manufacturing at Lloyds Bank Commercial Banking, says:

After an unsure start, it looks like manufacturers are getting back on track and helping to push industrial production back into positive growth. On the ground we see that boardroom confidence and the appetite to invest is high and it appears that this is now translating into healthy pipelines of activity. Management teams must stay this course and focus on expansion if they are to capitalise on the longer term growth prospects that the economy will no doubt present.

In the 3 months to February, industrial production and manufacturing were 10.4% and 4.9% respectively below their figures reached in the pre-downturn GDP peak in the first quarter of 2008, the ONS says.

UK industrial output weaker than expected

UK industrial output is weaker than expected: it edged up 0.1% in February, vs expectations of a 0.4% gain, while manufacturing met City forecasts with a 0.4% rise. Industrial production is the wider measure, which comprises manufacturing, mining and utilities.

You can find out more on the data on the Office for National Statistics’ website here.

Updated

“One more turn of the financial screw and Greece would be in capital controls; a terrible symptom of political failure of a six-year attempt to restore sustainability,” writes Gabriel Sterne, economist at Oxford Economics.

Conditional on capital controls, we suggest probabilities for (1) a quick exit; (2) a slow exit; (3) recovery, drawing on lessons from Cyprus. €-exit would be our baseline, but is not inevitable.

A detailed comparison with Cyprus establishes why the Greek case would likely be far more severe. Politics is key. In Cyprus, a new centre-right government implemented painful capital controls in the face of remarkably weak political opposition, and was able to pass on a big chunk of recapitalisation costs to foreign depositors. There was strong domestic support for deep fiscal and structural reforms. Within months the programme came to be seen as a credible path towards banking solvency, liquidity and fiscal sustainability; controls were removed after two years.

We stress three possible scenarios:

(1) Political breakthrough and path towards euro re-integration (30% probability). In spite of the gloomy narrative, a long path back to normality is only a change in political direction away. Capital controls could, if deposit freezes are avoided, trigger political change, programme adherence, and eventual normalisation.

(2) Period of extended brinksmanship and crisis, which ultimately ends in exit (30% probability). Brinksmanship gives way to euro-rationing, and probably default. A parallel currency could emerge, which could last a while in spite of being very inefficient in allocating scarce euros. There is a referendum, which, if pro-euro, could prolong euro afterlife, but ultimately too much damage would be done and exit would follow.

(3) Negotiated exit from the euro, probably announced within a month (40% probability). The Eurozone runs out of patience and an exit deal is negotiated. The deal involves staying in the EU.

Capital controls are a symptom of a deeper political malaise – the same one that has failed to restore Greek debt sustainability though prolonged crisis. The solution, like the blame, lies on both sides. Since 2009, the Troika have never offered Greece an adjustment path that is sustainable given the political context. Syriza or not, there is little support in Greece for the necessary adjustment to push debt towards sustainability.

The next couple of months represent last chance saloon. Capital controls in themselves would impose a considerable deadweight cost on Greece, making debt metrics much worse and agreement even more difficult.

And they would impact on public opinion. On the one hand desperation to keep the euro could push Greeks to accept more austerity; and the immediacy of massive default costs may push Eurozone politicians towards a last ditch agreement. On the other hand, it is feasible that mutual frustration is based on such fundamentally misaligned incentives that capital controls turn out to be a point of no return.

Athens faces another key week next week, when the Greek government will need to roll over €2.4bn worth of 3 and 6 month T-bills in bond auctions, as well as paying out over €1.5bn of social security payments.

The ECB once again raised its Emergency liquidity assistance (ELA) facility yesterday by €1.2bn to just over €73bn, as capital continues to leak out of Greek banks.

Kuenzel at Daiwa believes Athens needs to “start dancing to the Eurogroup’s tune”. The group of eurozone finance ministers meets in Riga, Latvia, on 24 April.

So, by 24 April, when the Eurogroup meets in Riga, the Greek reform plans need to be better specified, realistically costed and purged of counterproductive labour market and pension measures. Certainly, euro area finance ministers are probably at the end of their tether after ten weeks of the new government’s foot-dragging and game-playing, and any sympathy for the Greek position has long disappeared.

And notwithstanding Tsipras’ comments in Moscow that the EU had more to lose than Greece if the rescue failed, it is clear that the Greek government’s bargaining position is exceedingly weak. Unlocking the existing bailout funds is Greece’s only option to avoid default and euro exit and the Eurogroup has been resolute in its message on what is required of Greece. So if the country is to receive further bailout money to save it from default in May, the Tsipras administration is going to have to start dancing to the Eurogroup’s tune.

Updated

EU draws up secret plans to kick Greece out of eurozone, Times reports

For those who thought it was going to be a “Greece-free day” (it is Good Friday in Greece today): according to the Times, eurozone countries are secretly drawing up plans to kick Greece out of the currency bloc as they prepare for the country to be declared bankrupt next month.

The story cites a memo drawn up by the finance ministry in Finland, which is closely allied to Germany.

Greece has until next Friday to come up with a new list of economic reforms that must then be agreed by its three international creditors – the European Central Bank, European Union and International Monetary Fund – to unlock €7.2bn of aid.

Robert Kuenzel, director of euro area economic research at Daiwa Capital Markets, says:

After Greece’s repayment of €460m to the IMF yesterday and the ECB’s decision to grant a further €1.2bn in Emergency Liquidity Assistance to Greek banks, the flow of crisis-related news is likely to die down during the Orthodox Easter weekend beginning today and running until Tuesday.

But with only five working days remaining for the Greek administration to substantively improve on its reform offerings to the Eurogroup, the Greek government faces the Herculean task of developing - and legislating - a reform programme sufficient to unlock the remaining €7.2bn of bailout funds before the Eurogroup meets on 24 April.

Back to the pound. Analysts are warning that sterling could slide further ahead of the 7 May general election in the UK – the closest for more than 20 years. It’s fallen to $1.4681 this morning.

Hewson at online trader CMC Markets says:

The pound has started to come under some pressure in recent days as the prospect of political gridlock in a few weeks’ time starts to become a real possibility, at a time when some of the economic data is starting to show some signs of weakness.

In London, the FTSE 100 index has gained more than 30 points to 7047.70, a 0.5% rise. The Dax in Frankfurt is nearly 70 points ahead at 12235.11, a 0.6% gain, while the CAC in Paris has risen over 12 points, or 0.2%, to 5221.58.

European shares hit 15-year high

European shares are rising again, as fears over Greece have eased somewhat following yesterday’s €450m debt repayment to the IMF.

The pan-European FTSEurofirst 300 share index has powered ahead to hit is highest level since 2000, while the euro continued its slide, dropping to its lowest level since 19 March. The weak euro is good news for exporters.

The FTSEurofirst 300 index of top European shares is up 0.4% at 1637.19.

Spain fared better, with a 0.6% rise in industrial production in February.

CHART: Industrial production continues to rise in Spain. Still some upward potential to catch up with strong PMIs. pic.twitter.com/shikfE2M9m

— Maxime Sbaihi (@MxSba) April 10, 2015

Manufacturing in France was also unchanged in February, missing estimates of a 0.6% gain, after January’s revised decline of 0.3%.

Industrial output in France was flat in February.

Contrast this with Greece, where production unexpectedly jumped by 1.9%.

CHART: France industrial production stagnated in February, pausing upward trend. Still 15% below pre-crisis levels. pic.twitter.com/kida4dM0fA

— Maxime Sbaihi (@MxSba) April 10, 2015

Updated

European stock markets are expected to finish the week on a high, with the weak euro boosting exporters.

Updated

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

After another crunch day for Greece yesterday – Athens had to (and did) repay a €450m loan tranche to the International Monetary Fund – the focus is on the rest of Europe today, with industrial production data out for France, Spain and the UK.

In the UK, manufacturing output is expected to bounced back in February from the previous month’s weak reading. Philip Shaw, chief economist at Investec, is predicting a 0.6% gain following January’s 0.5% drop. He has pencilled in a slightly smaller rise of 0.4% for industrial production which also includes mining and utilities, following January’s 0.1% decline. This reflects uncertainty around oil output, which he assumes was flat on the month.

The figures are out at 9.30am BST, along with construction output.

The pound has fallen to $1.4694 this morning. Any disappointment in the numbers is likely to put further pressure on sterling.

Michael Hewson, chief market analyst at CMC Markets, says the pound’s weakness in recent days suggests

the potential for a return to the March lows of $1.4630, and possibly even lower, as we head towards the election next month, with the 2010 lows at $1.4230 now in play. To stabilise we need to move beyond the $1.5000 area, which has capped every rally for the last week.