Editor's note: This is the second article in a five-part series about all-asset retirement planning that is covering such topics as using annuities and housing wealth, making the most of tax benefits and establishing an investment strategy. Article one is It's Time to Redefine Retirement for Retirees With $500,000 to $5 Million: Here's How.

With the benefit of Social Security, almost all retirees are guaranteed some level of lifetime income. So, the question isn't "Will I run out of money?" Instead, it's, "How much income is enough to cover my living expenses, after covering my late-in-life health and long-term care expenses?"

I've said in previous articles that lifetime annuities are an obvious choice for retirees' retirement plans, particularly with the near-extinction of employer-provided pensions and especially with pressures on Social Security.

If Congress fails to act by 2033, Social Security benefits could be cut by 23%, according to the Social Security Administration's 2025 Trustees Report.

If lawmakers do act, however, part of their solution could be to increase the age at which full benefits can be claimed, which would effectively be a cut in benefits for future retirees.

As I said in the first article of this series, I'm writing for the group of retirees known as "mass affluent," or the large cohort that, although reasonably well-off, cannot rely on their savings to produce enough interest or dividends to pay all expenses.

Types of lifetime annuities

Throughout this series, we will offer a guide to retirement planning that relies on easily understood and basic financial products that, in addition to protecting income and liquid savings, are designed to provide peace of mind.

There are two basic types of lifetime annuities that are used in retirement planning:

Immediate annuities start paying within the first year after purchase, often at the start of retirement, to provide a guaranteed lifetime income stream.

They can be customized to provide protection for a beneficiary and to continue income to a surviving spouse.

A qualified longevity annuity contract (QLAC) is a type of deferred income annuity that can be purchased with funds from a rollover IRA, and at the retiree's election, annuity payouts start no later than age 85.

Congress and the IRS created the QLAC to provide longevity protection as a partial substitute for pensions. To encourage the election of QLACs by retirees, they provided significant tax benefits. (More on that below.)

A QLAC can be used alone, but later in this article, I dive into ways to combine the benefits of a QLAC with a home equity conversion mortgage (HECM) to provide not only lifetime income, but also a source of liquidity to pay for unplanned expenses.

One word of caution about the term "annuities": I like to remind readers that annuities come in many different flavors, including "accumulation annuities" with income usually deferred and often with complex return formulas.

These annuity forms are quite popular, and in our planning, we treat them as part of our investment asset class, not like a QLAC that provides guaranteed lifetime income and valuable tax benefits.

Examples of lifetime annuity payouts

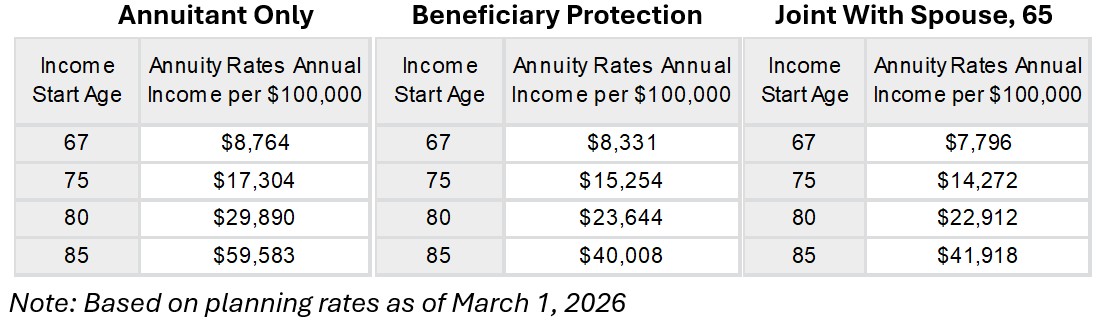

As discussed above, lifetime annuities come in different flavors depending on when payments start, whether there's beneficiary protection and whether income continues for one life or two.

Let's use a sample male retiree, age 67, with $100,000 in his IRA account allocated to lifetime annuities and compare the lifetime annual income each can purchase.

In all cases:

- The income is guaranteed to continue for life after the income start age

- The beneficiary protection guarantees the payments continue to the named beneficiary until a total of $100,000 is paid out

- The joint annuity continues to the surviving spouse

While both types of lifetime annuities are used as part of our planning, what's new on the scene is that a QLAC enjoys some special tax benefits.

Favorable tax treatment of lifetime annuities

The tax authorities and Congress believe in the value of lifetime annuities. Here are some key examples:

Up to $210,000 of a rollover IRA for each retiree can be used to purchase a QLAC without any taxable event until payments are received. That deferral can be as late as to age 85, and with the most recent tax enhancement, there's no additional limit on the percentage of the rollover IRA account used to purchase a QLAC.

From the table above, a 67-year-old man uses $100,000 of his rollover IRA to purchase about $60,000 of lifetime income starting at age 85, which can be used by the retiree to meet all kinds of expenses.

When an immediate annuity is purchased out of personal savings (no limit), a portion of the annuity payment is considered a return of investment and is not taxed.

For a 67-year-old man who uses $100,000 from personal savings to purchase $8,700 per year in lifetime income, nearly two-thirds of that payment is excluded from tax during the first 17 years.

Under an inherited IRA, a surviving spouse can apply the inherited funds to purchase a lifetime annuity, which both secures lifetime retirement income and spreads the tax bill.

Combining a QLAC with housing wealth

Longtime readers know that I like QLACs, not only for the longevity protection and tax benefits above, but also for their ability to complement other parts of retirement plans, particularly HECM, which accesses housing wealth, the single largest amount of savings for most retirees.

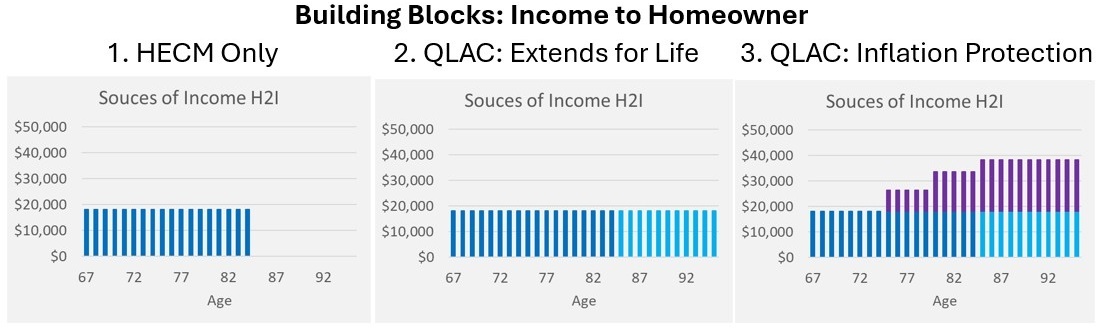

Here are three examples of QLAC utilization that we use in our planning:

- Continue HECM drawdowns from 85 and for life

- Provide guaranteed lifetime inflation protection

- Make all or part of HECM interest payments with a QLAC's reserve income

The charts below show examples for our sample homeowner with a home worth $1 million.

The first chart shows HECM payments of $18,000 a year from age 67 to 84. In the second chart, QLAC payments kick in at age 85. Chart three demonstrates how a laddered progression of QLAC payments provides growing income and protection against inflation.

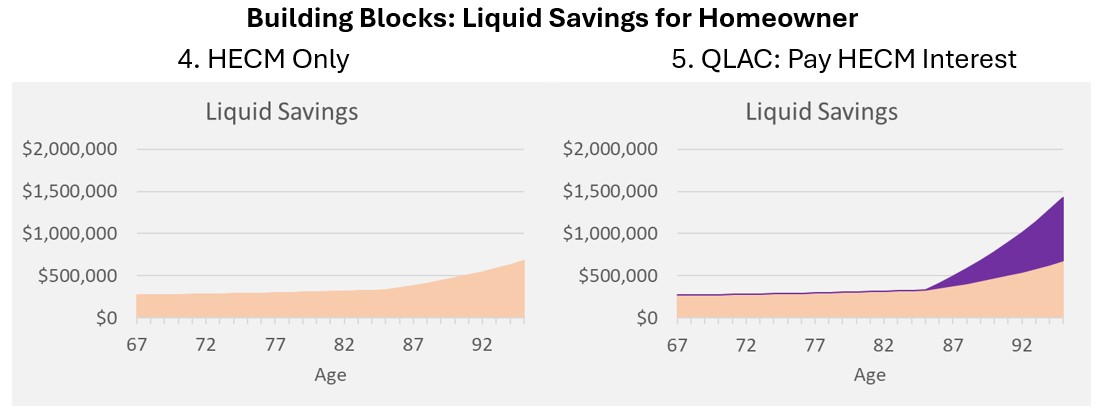

In addition, in our HomeEquity2Income, or H2I, planning component, HECM provides liquid savings through a line of credit (see graph four below).

Although substantial, it may not be large enough to cover long-term care and other large expenses later in retirement.

To grow that liquid savings after age 85, the retiree can direct a portion of QLAC payments to pay HECM interest.

Graph five below shows the impact on liquid savings from these HECM interest payments. Because interest is paid, there is a tax deduction that offsets all or part of payments using annuities.

To describe it all another way, retirees have options beyond spending down the money they have saved in their 401(k) or IRA. Combining the strengths of various financial instruments, like a QLAC and a HECM, can make savings do more.

My next articles will discuss other aspects of H2I, but you can visit Go2Income now, answer a few questions about current income and future needs and start creating your own H2I plan to build retirement income and liquidity.

Related Content

- An Expert Guide to How All-Assets Planning Offers a Better Retirement

- This HECM-QLAC Power Move Can Unlock Guaranteed Retirement Income

- For a Richer Retirement, Follow These Five Golden Rules

- Transform Your Retirement Plan With This Powerful Combo

- How Combining Your Home Equity and IRA Can Supercharge Your Retirement

This article was written by and presents the views of our contributing adviser, not the Kiplinger editorial staff. You can check adviser records with the SEC or with FINRA.

.png?w=600)