Tyson Foods (NYSE: TSN) is no headline-making growth story, but it is a quality consumer staple whose stock price is setting up for big gains. Consumer trends and commodity prices underpin its business and outlook, indicating steady growth and cash flow, which is the operational detail. Cash flow enables a capital return, which, alongside the value proposition, points to a rising share price. The technical action aligns with this outlook, as it reflects a bottom and a market on track for a reversal.

Tyson Foods’ Stock Value and Yield Are Accumulated in 2026

Tyson Foods isn’t the highest-yielding consumer staple, but its dividend yields a competitive 3.2% as of early May. The payment is reliably safe at approximately 50% of current-year earnings forecasts and is expected to increase, based on the company’s history.

Distributions have increased for nearly 15 consecutive years, and earnings growth is expected to support further increases. Repurchases are also in the picture. The company does not aggressively reduce its count but instead offsets share-based compensation and other dilutive factors through share buybacks.

The 2026 earnings results are expected to be weak relative to the prior year, but the company's most recent fiscal Q2 earnings report outpaced consensus estimates. Looking ahead, analysts forecast a return to growth next fiscal year, with earnings advancing by double-digits and then accelerating in the following year. In this scenario, the 16X forward earnings at which the stock trades in mid-Q2 2026 presents some value, and the 11X relative to 2028’s consensus forecast even more. Assuming the company can grow in line with its forecasts, the stock price could rise as much as 50% over the next 18 months to two years, and more if it outperforms.

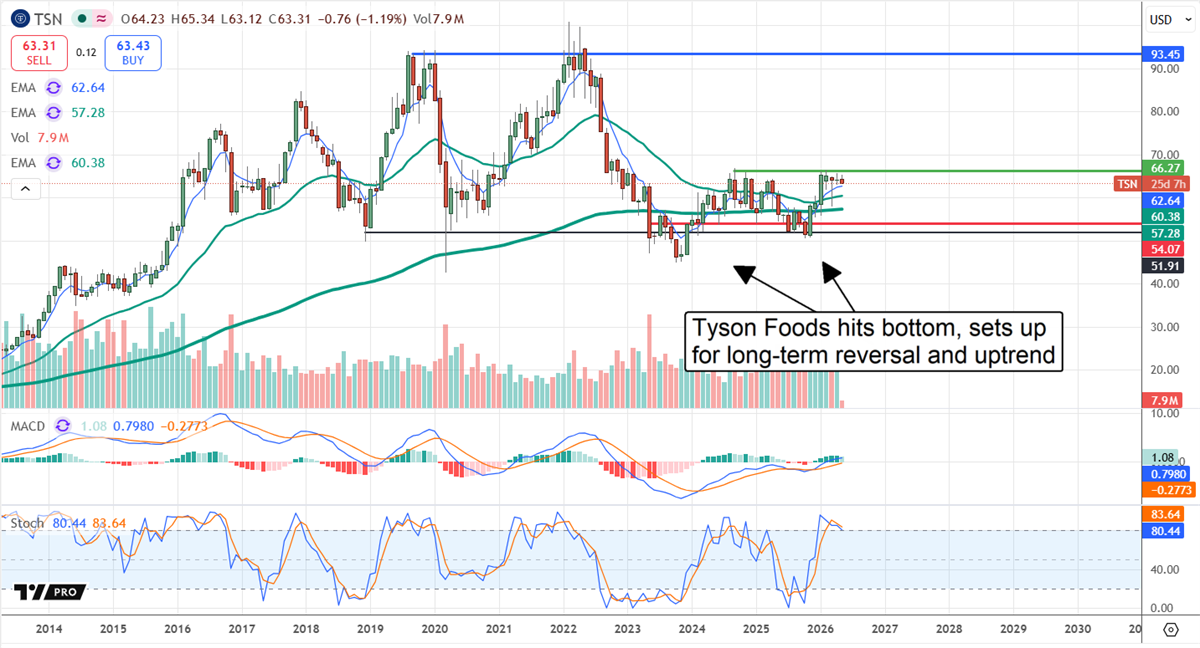

Technical Setup Points to 50% Upside

A 50% upside aligns with the technical outlook. The stock price bottomed in 2024 and 2025, showing a solid Double Bottom, and is on track to break the baseline in May.

The baseline is near $66.25 and is significant because it serves as a trigger for bullish behavior and confirms a full market reversal. The pattern itself suggests a $12 to $15 move is possible in the near term, but longer-term projections are more robust, with the all-time highs as an obvious target.

Analyst and Institutional Support Reinforce the Bull Case

Analysts and institutions are driving forces for this market. The 15 analysts tracked by MarketBeat rate the stock as a consensus Hold, with bullish bias in the internals. There are no Sell ratings, firming sentiment, a 35% Buy-side bias, and an uptrend in the price target, with recent revisions pointing to a price well above the critical resistance level.

Institutions are following the analysts’ lead, owning more than 65% of the stock and accumulating aggressively. The group bought on balance for five consecutive quarters, including early Q2 2026, with a $2-to-$1 over the trailing 12 months, and provided strong support. Their support is not expected to evaporate as the quarter progresses; it is expected to strengthen. Short sellers may also strengthen the rally, as they have been selling into it and short interest is approaching long-term highs; the move above $66.25 is likely to trigger short-covering.

Tyson’s Diversified Protein Portfolio Has It Positioned for Growth

Tyson had a solid quarter, with Beef its main weakness. However, while volume fell by double digits, the price increase nearly offset the decline, helping drive systemwide strength. The company reported $13.65 in net revenue, up 4.4% as-reported and 1.8% adjusted, outpacing the consensus by a narrow margin. Strengths included Chicken, Pork, and Prepared Foods, all of which grew in volume and pricing and are expected to remain solid in upcoming quarters. Beef production is expected to decline, and high prices are expected to persist in the upcoming year, helping drive protein-hungry consumers toward lower-priced options.

Margin is a mixed bag, but one that favors investors. GAAP earnings grew by triple digits; however, adjusted earnings fell compared to last year. The good news is that adjusted earnings came in well-above forecasts, more than 1,000 basis points, and support the healthy capital return outlook.

Tyson’s biggest risks are in execution. Commodity prices threaten to undermine margins, and the pressures will mount as the year progresses. The Iran war has oil prices up, and that is reflected in the cost of fertilizers and, soon, in the cost of feed. As it stands, the company is offsetting the impacts. Catalysts include the focus on free cash flow. Management is working to reduce leverage, servicing costs, and working capital to free up cash flow, strengthen the balance sheet, and support capital return growth.

Where Should You Invest $1,000 Right Now?

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

The article "Tyson Foods' Total Returns: Tasty Treats for Income Investors?" first appeared on MarketBeat.