/Global%20Network.jpg)

Thomson Reuters (TRI) is a global leader in providing trusted news, data, and intelligence solutions for professionals in legal, tax, accounting, compliance, government, and corporate sectors. It offers essential tools like Westlaw for legal research, ONESOURCE for tax management, and Reuters news services, helping over 40,000 customers worldwide make informed decisions. Known for accuracy and innovation, the company combines AI-driven analytics with deep expertise to streamline workflows and boost efficiency.

Formed in 2008 through the merger of Thomson Corporation (founded in 1934) and Reuters Group (founded in 1851), it is headquartered in Toronto, Canada.

Thomson Reuters Stock

Thomson Reuters' stock has done quite poorly amid market volatility. Over the past five days, it rose about 18%, following a 17% slide-off in a month. The stock’s six-month performance shows a downfall of 44%, while year-to-date (YTD) reports reflect a 26% loss for investors. TRI stock trades around 55% below its 52-week high of $218, set in July 2025, while giving a 44% negative return in 52 weeks’ time.

Compared to the Nasdaq Composite ($NASX), TRI has underperformed heavily. The index gained close to 5% in 6 months’ time while the stock crashed 44%, and further in 52 weeks the index had a 22% return versus Reuters’s 44% slip-off. In the short term, the stock has the edge, with the index declining 1% in the last five days against the stock’s 18% surge.

Thomson's Earnings Results

Thomson Reuters released Q4 2025 results on Feb. 5, 2026, posting revenue of $2.01 billion, up 5% year-over-year (YoY) and in line with analyst estimates. Adjusted EPS was $1.07, edging past the $1.06 consensus forecast. Full-year organic revenue grew 7%, meeting the company's outlook.

Adjusted EBITDA rose 8% to $777 million with a 38.7% margin (up 110 basis points). Net cash from operations jumped 35% to $756 million, free cash flow climbed 38% to $581 million, and cash reserves stood at $511 million with a low 0.6x leverage. "Big 3" segments (Legal, Corporates, and Tax) each grew 9-11% organically.

For Q1 2026, the company expects 7% organic revenue growth and a 42% adjusted EBITDA margin. Full-year 2026 guidance targets 7.5%-8% organic revenue growth and 100 bps EBITDA margin expansion from 39.2%.

Software Stocks Rally on Anthropic Partnerships

Software stocks bounced back Tuesday after AI firm Anthropic unveiled Claude Cowork updates, partnering with enterprise giants like Salesforce's (CRM) Slack, Intuit (INTU), DocuSign (DOCU), LegalZoom (LZ), FactSet (FDS), and Alphabet's (GOOG) (GOOGL) Google Gmail. Custom plugins target finance, engineering, and HR, easing fears of AI disrupting the sector. Wedbush called the prior selloff "overblown."

Thomson Reuters led with an 11%+ surge, as Anthropic noted the company already uses Claude-powered AI agents. FactSet jumped nearly 6%, Salesforce 4%, while DocuSign and LegalZoom gained over 2% each, signaling collaboration over replacement in enterprise AI.

Should You Buy TRI Stock?

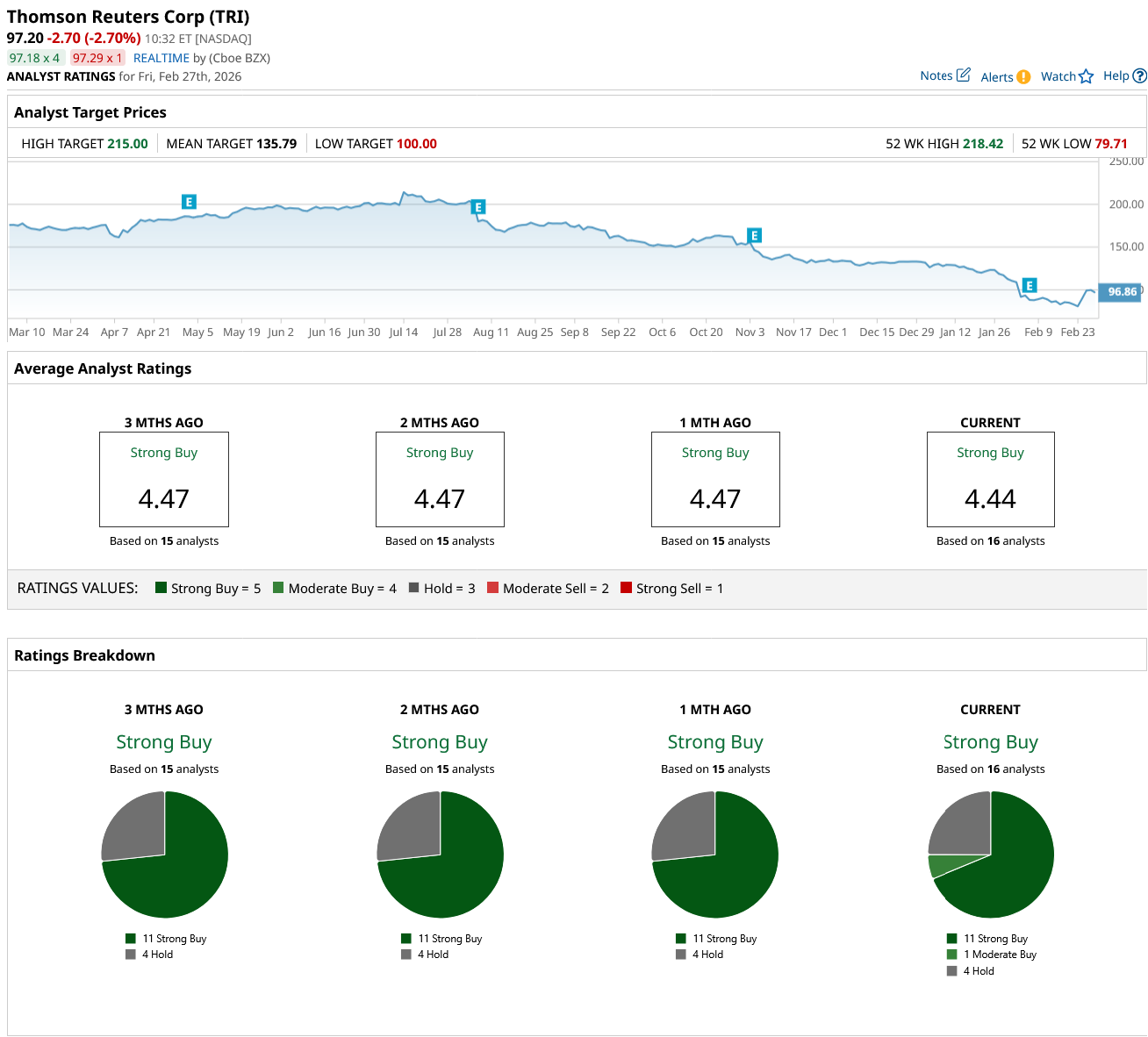

Now, despite its struggles in the market, TRI stock has plenty of supporters on Wall Street as it receives a consensus “Strong Buy” rating with a mean price target of $135.79, reflecting an upside potential of 40% from the market price.

The stock has been rated by 16 analysts so far, with 11 “Strong Buy” ratings, one “Moderate Buy” rating, and four “Hold” ratings.