Unless you have done zero work on retirement, you have a plan. It may be outdated, formal or informal, producing good results or not. But you have a plan.

Then you start to think about all that has happened in the world — and how your objectives may have changed — since you set up your “plan.” The holes probably loom large in your imagination, but there will be improvements that you can take advantage of, too, if you recognize them.

For one thing, the longer you live in your house, the more equity you have, barring emergencies. Current interest rates and inflation may seem alarming, but higher interest rates can also bring you more income from annuities. And keeping taxes lower in retirement is more likely when you employ the tools now at your disposal just because you’ve lived a little longer and saved a little bit more.

Designing the plan that best fits you

Start by thinking about your own wants and needs. There’s no reason to be intimidated. You know your objectives better than anyone. You also know your budget requirements, and also what your kids may need, and even whether you’re an “age-in-place” person.

Decide what’s most important to you. It could be tax reduction, the amount of guaranteed income or having liquid funds to pay for long-term care, a critical health crisis or another kind of emergency. You probably have in mind a number for starting income and whether you plan to leave a legacy to heirs. And perhaps you want to put off taking Social Security benefits as long as possible, or ensure continuity of income to your spouse. Finally, factor in your thoughts about the future of inflation and stock market performance.

The challenge is how to go from your current plan to one that meets your new thinking. Here’s a way to think about the process while at the same understanding more clearly what each step brings.

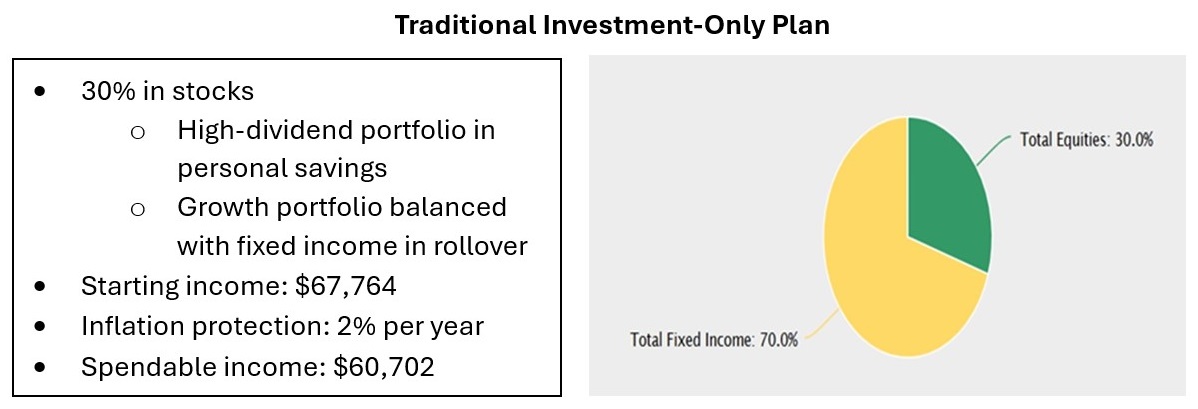

Starting with a traditional investment-only plan

Set out below is how a typical asset-focused plan might look. The plan is generating dividends and interest and using IRA withdrawals for current income and protects itself against large market losses by a low 30% allocation to stocks.

As you rethink your objectives, your new plan will begin to unfold. The order of steps above represents one set of personal objectives and just one way to implement that new plan.

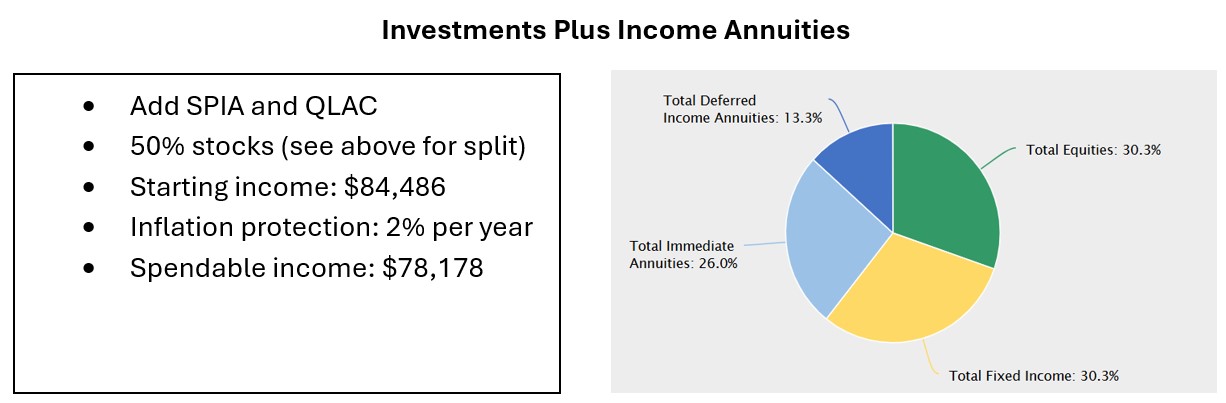

Adding income annuities to the mix

In considering the next stage, you will see that income annuities can provide more income, lower your taxes and reduce your income risk.

For instance, IRS rules allow you to take $200,000 from a rollover IRA account and purchase a QLAC, a type of deferred income annuity that is designed to begin producing payments as late as age 85.

Income for today comes with a single-premium immediate annuity (SPIA), purchased with already-taxed savings to create a larger income stream without large additional taxes.

This is a logical and straightforward decision, replacing some of the fixed-income investments with income annuities.

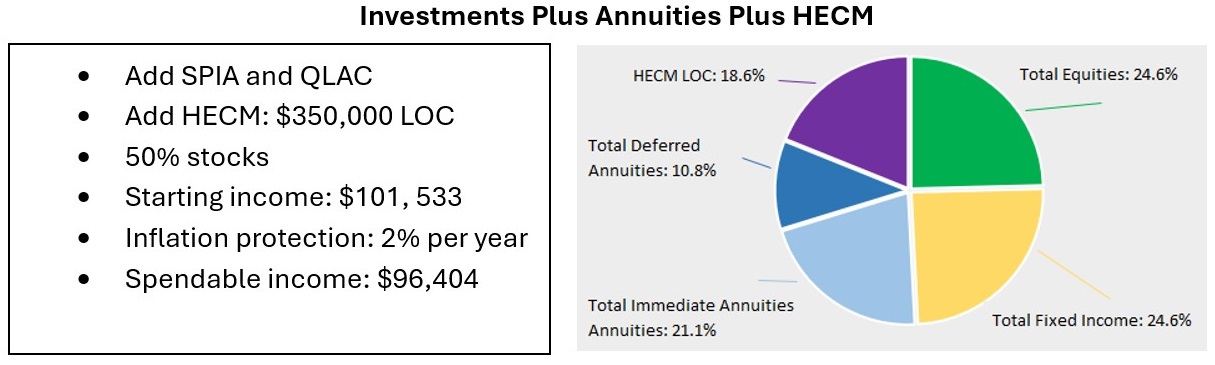

Adding HECM to provide more income and liquidity

The next step: Add a home equity conversion mortgage, or HECM, to provide more income and, most important, a line of credit that grows over time. Under IRS rules, both sources of cash are considered loans and are not subject to federal income tax. If you end up needing money to pay for health care costs not covered by insurance, your HECM line of credit should cover it or give you a good start.

Under HomeEquity2Income, or H2I, HECM and QLAC are combined so that QLAC payments will pay for the HECM interest as well as provide income after age 85.

Now we have a plan that has attractive income and liquidity.

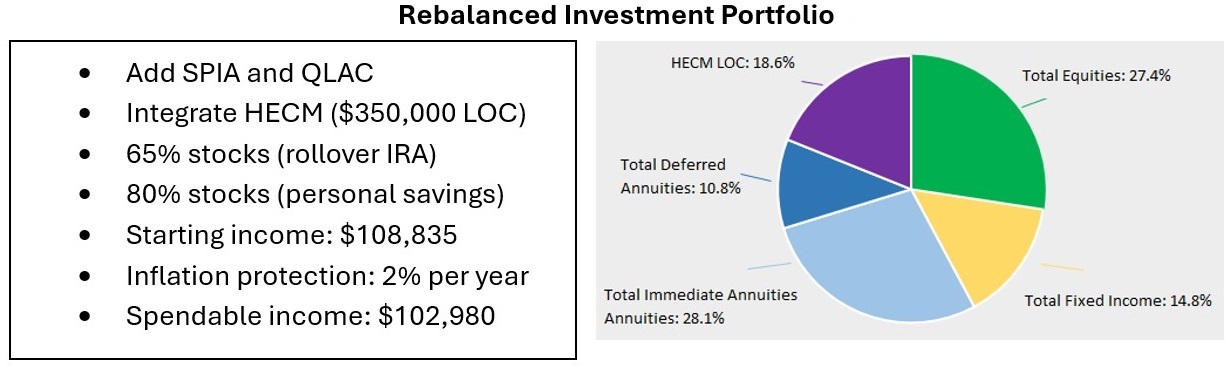

Final adjustments to balance market risk

Final step: With these two new asset classes in place, consider what level of risk you might assume in your split between fixed income and stock investment portfolios. With your greater security of income and lower taxes, you can increase the allocation of the stock portfolio in personal savings to high-dividend stocks, providing yet more income. The growth portfolio in your rollover IRA will provide potential for higher withdrawals.

Note that while this plan is apparently more aggressive, there is a lower-percentage allocation to stocks.

Other steps to consider

When you have more spendable money, you have additional options. You may decide to allocate a portion of your IRA withdrawals to a Roth IRA for tax purposes. If you have grandkids, a 529 plan awaits for funding college educations. You will have other options, too.

When you’re done, the new plan may still have some elements of the old plan, but the updates will allow you to more easily meet your goals for retirement income, liquidity, legacy and taxes.

Get started at Go2Income

Take the first step with a visit to Go2Income and start building a plan that considers income, taxes and long-term goals. The exercise is flexible, and when you have questions, schedule time with a Go2Specialist, who can answer all your questions.

.png?w=600)