/Technology%20by%20Alexandre%20Debieve%20via%20Unsplash-2.jpg)

STMicroelectronics (STM) is a Geneva-headquartered global semiconductor leader serving customers across automotive, industrial, personal electronics, and cloud computing markets. Born from the merger of Italian and French semiconductor firms, STM designs and manufactures a broad portfolio spanning analog ICs, MEMS sensors, microcontrollers, power discretes, and advanced connectivity solutions.

What makes STM an increasingly compelling AI candidate is its expanded multi-year, multi-billion-dollar strategic collaboration with Amazon (AMZN) Web Services (AWS), positioning STM as a key supplier of high-bandwidth connectivity, mixed-signal processing, and energy-efficient power ICs that directly power next-generation hyperscale AI and cloud computing infrastructure. For investors seeking a differentiated, less-crowded entry into the AI semiconductor supply chain, STM presents a unique value proposition.

STMicroelectronics Stock Surges

STM's 52-week return is approximately 165%, while its YTD return is around 159%, reflecting a recovery in auto chip demand, normalizing distributor inventories, and an expansion into the AI infrastructure market that boosted the stock's price. STM surged over 33% in just 30 days following its Q1 2026 earnings beat, driven by AI data center momentum and improving bookings.

Against the S&P 500 Information Technology Index ($SRIT), which has returned about 29%, STM has significantly over performed over the past year. Its accelerating revenue recovery, AWS partnership, and growing AI infrastructure exposure position it as a high-conviction stock within the broader semiconductor sector.

STMicroelectronics Shines on Results

STMicroelectronics reported Q1 2026 net revenues of $3.10 billion, up 23% year-over-year and beating consensus estimates of approximately $3.05 billion. The revenue beat was fueled by strong momentum in personal electronics and cloud-edge computing products. Non-GAAP diluted EPS came in at $0.13, up 85.7% year-over-year but slightly below analyst expectations of around $0.18, as unused manufacturing capacity charges weighed on near-term profitability.

GAAP gross margin for Q1 came in at 33.8%, while non-GAAP gross margin reached 34.1%, both above the midpoint of the company's guidance range, driven by a favorable product mix. Net cash from operating activities was $534 million, down slightly from $574 million a year ago, primarily due to approximately $45 million in restructuring costs tied to the company's ongoing manufacturing footprint optimization program. Operating income on a non-GAAP basis stood at $171 million, with operating margins recovering meaningfully year-over-year.

Management guided Q2 2026 revenues to $3.45 billion at the midpoint, implying 11.6% sequential growth and 24.9% year-over-year growth, with non-GAAP gross margins expected at approximately 35.2%. Most notably, CEO Jean-Marc Chery confirmed that ST is now positioned to capture upside from new AI-driven programs, with data center revenues expected to exceed $500 million for 2026 and surpass $1 billion for 2027, a clear signal that this oft-overlooked chipmaker is becoming a meaningful player in the global AI infrastructure buildout.

Mizuho Bullish on STM

Mizuho analyst Vijay Rakesh has raised his price target on STMicroelectronics to $68 from $56, maintaining an “Outperform” rating, citing accelerating artificial intelligence tailwinds benefiting the analog semiconductor market. In a note to clients, Rakesh highlighted that analog chipmakers, including STM, are seeing growing content wins within high-power AI server architectures, with improving lead times and pricing dynamics, particularly within data center products. While near-term headwinds persist in the automotive segment, with light vehicle production now estimated down 2.3% year-over-year, the analyst views AI data center demand as a meaningful and durable offset.

The price target hike reflects growing conviction that STM's specialized analog and power semiconductor portfolio is increasingly mission-critical to the AI infrastructure buildout, reinforcing the bull case for this under-the-radar semiconductor name.

How to Play STM?

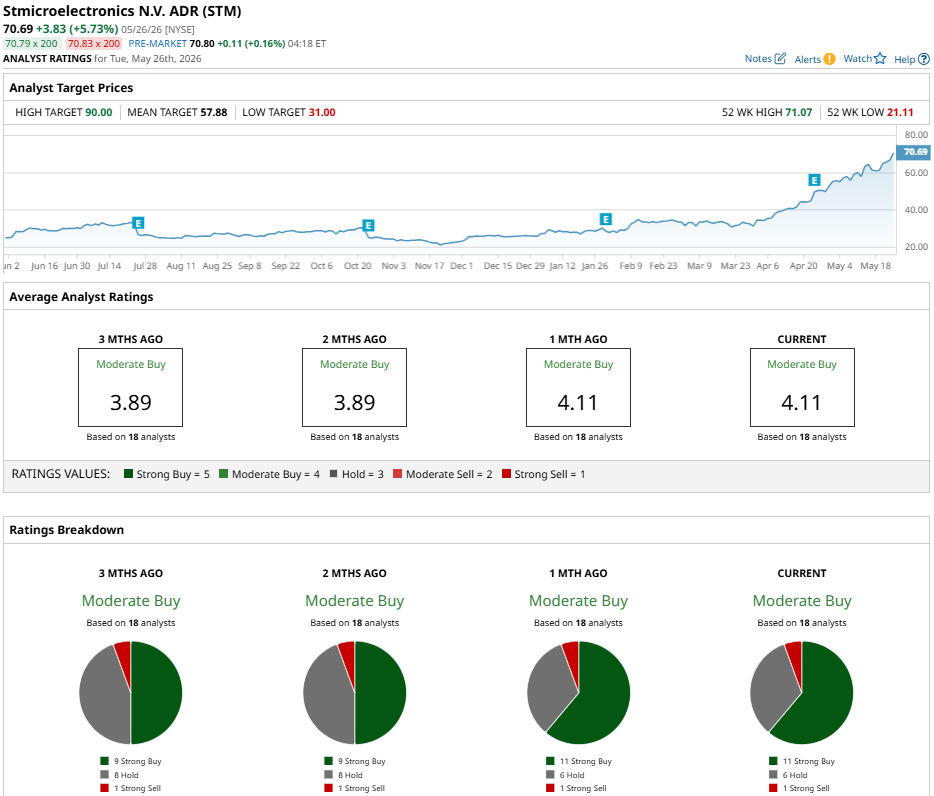

With Mizuho's upgraded price target of $68 reinforcing the AI data center tailwind narrative, STMicroelectronics is gaining institutional attention as a differentiated analog semiconductor play. However, broader Wall Street consensus remains cautious, with STM carrying a "Moderate Buy" rating across 18 analyst ratings, comprising 11 "Strong Buy," six "Hold," and one "Strong Sell," with a mean price target of $57.88, implying approximately 15% downside from current levels.

For investors, STM represents a higher-risk, higher-reward opportunity, best suited for those with conviction in its AI infrastructure pivot and willingness to look past near-term margin pressures.