Spirit Aviation Holdings (FLYYQ) has once again found its way onto investors' radar screens — this time under rather unusual circumstances. Reports that President Donald Trump's administration has been mulling over a possible plan for rescuing the bankrupt ultra-low-cost airline have led to an increase in trading activity. It is hardly surprising that such news has sparked speculation in FLYYQ stock, which is already in deep trouble.

Nevertheless, investors should remember the bigger picture. The airline sector has recently been dealing with a combination of rising oil prices and uneven passenger demand recovery. It is also becoming increasingly hard for smaller airlines to compete in this challenging market. As for Spirit's case, the focus lies not on the company's recovery ability, but rather on survival. The only interesting question is whether this is yet another story of failed bankruptcy restructuring in which shareholders will be left holding the bag.

About Spirit Airlines Stock

Spirit is an ultra-low-cost airline headquartered in Dania Beach, Florida. Currently, the firm's market capitalization amounts to approximately $48.7 million amid the ongoing bankruptcy restructuring procedures.

FLYYQ stock is extremely unstable. Over the course of the past year, the share price has plummeted more than 98% from a high of $9.44 to a 52-week low of $0.16 per share. However, since hitting rock bottom, FLYYQ stock has seen a sharp rebound, climbing to around $1.56 at current levels. Still, shares have underperformed the broader S&P 500 Index ($SPX) over the past 52 weeks.

As for Spirit's traditional valuation multiples, they are basically meaningless here. Without any earnings, negative margins, and lacking any guidance for profitability in the future, ratios like price-to-earnings (P/E) and price-to-sales (P/S) become useless. In other words, shares are trading based on restructuring speculations.

Spirit Airlines Misses on Earnings

The company's latest financial performance shows how serious its problems have become. Full-year revenue for 2025 fell 23% year-over-year (YOY) to $3.8 billion, while the company posted a net loss of $2.76 billion. Despite some improvements in operating losses to -$768.7 million, the company still finds itself in a rather tough position.

Management's guidance suggests that, for the first quarter of 2026, operating margins are set to be -5.6%, which represents an improvement versus last year's -27.1%. Clearly, the situation shows some signs of getting better. However, it should be stressed that this improvement has been mainly caused by cost-cutting measures.

One of the company's most notable initiatives to overcome current difficulties is called "Project Soar," which in part aims to reduce Spirit's size. By the end of 2026, the company is projected to have 76 to 80 aircraft. This may improve the outlook for the firm somewhat, but investors should bear in mind that drastic changes will be required to help Spirit survive.

Another challenge comes from external factors — namely, rising jet fuel prices. Given the current geopolitical climate, this trend may persist, thus offsetting the recent improvements in margins. Under the most adverse scenario, margins might fall to -20% again.

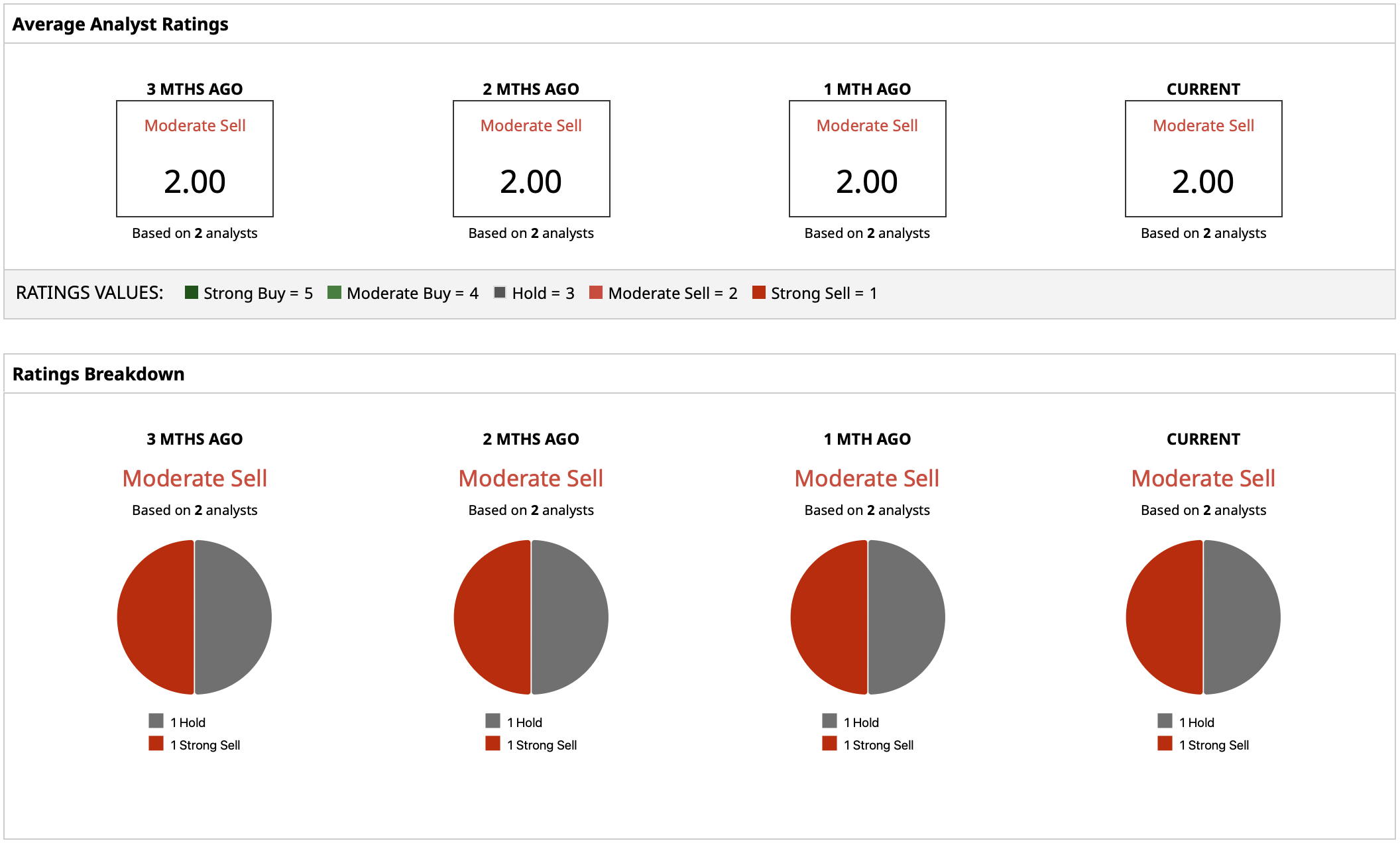

What Do Analysts Expect for Spirit Airlines Stock?

FLYYQ stock does not have any price targets from analysts, which is common among firms that have filed for bankruptcy. The stock currently has a consensus “Moderate Sell” rating. The lack of target prices says a lot about the state of the company's valuations. Without knowing what will happen after the restructuring, analysts are not in any position to set any targets since Spirit's valuation is purely speculative and tied up in how the restructuring pans out.