This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

AT-A-GLANCE

- The futures oil curve is in backwardation

- OPEC is sticking with its slow pace of rebuilding production

The European Union has decided not to accept any oil imports from Russia via ship, which allows Hungary to still receive Russian oil via pipelines.

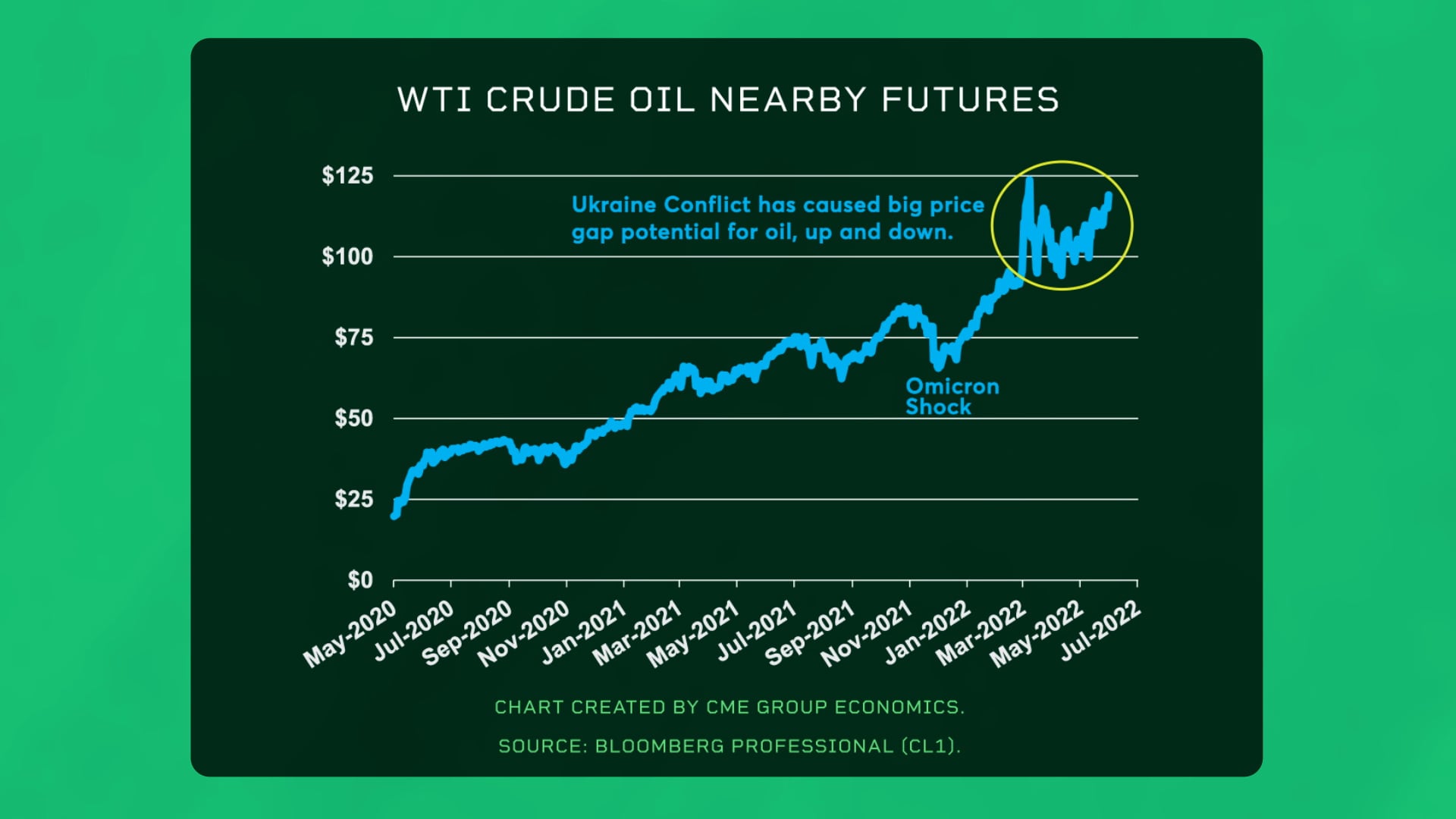

One might wonder, with crude oil trading around $120 per barrel, why production is not growing faster.

While not at full capacity, OPEC does not have that much more room to increase supply, so it is sticking with its slow pace of rebuilding production.

Scan the above QR code for more expert analysis of market events and trends driving opportunities today!

That leaves the U.S. shale oil sector as the potential primary swing producer. U.S. oil production is growing but more slowly than many would have anticipated. What’s behind the slow growth in U.S. oil production?

First, hedging is challenged. The futures oil curve is in backwardation, where the two-year-out price is trading at about a 30% discount to the spot price. And while backwardation should not be interpreted to mean that market participants do not think the oil price can go higher, it does mean that the oil produced from a shale oil well drilled today may command a much lower price than today’s spot price. This makes getting financing and risk managing the revenue flow more complex and challenging.

Second, input costs are much higher than they were pre-pandemic. Sand and related materials are more expensive, steel casing for pipes cost more, and skilled crews are in short supply.

The bottom line is that it will take considerable time for the oil supply to increase, but the danger of oil surging ever higher from further European restrictions on Russian oil has diminished because they have already been implemented.