This article is intended to rebuke the Bank of Thailand (BoT) and those who believe Thailand's trade deficits are "transitory" and will return to a surplus once oil prices fall back to normal levels.

This article is intended to rebuke the Bank of Thailand (BoT) and those who believe Thailand’s trade deficits are “transitory” and will return to a surplus once oil prices fall back to normal levels.

Thailand used to take pride in its successful export economy. Over the past 20 years, there was not a single year in which the country recorded a trade deficit, even during the Russia–Ukraine war. Although the trade surplus was halved to $13.5 billion in 2022, it remained at an admirable level. At the peak of the oil price spike to $115 (3,839 baht) a barrel in June that year, Thailand’s trade balance briefly slipped into deficit for a couple of months at $1.3 billion per month before returning to a strong surplus, indicating the country’s solid export base.

Contrary to the central bank’s belief, however, a rebound to a trade surplus in 2026 (and beyond) is highly unlikely due to an eroding export base. Oil prices account for only 40% of the deficit problem, yet receive 100% of the blame.

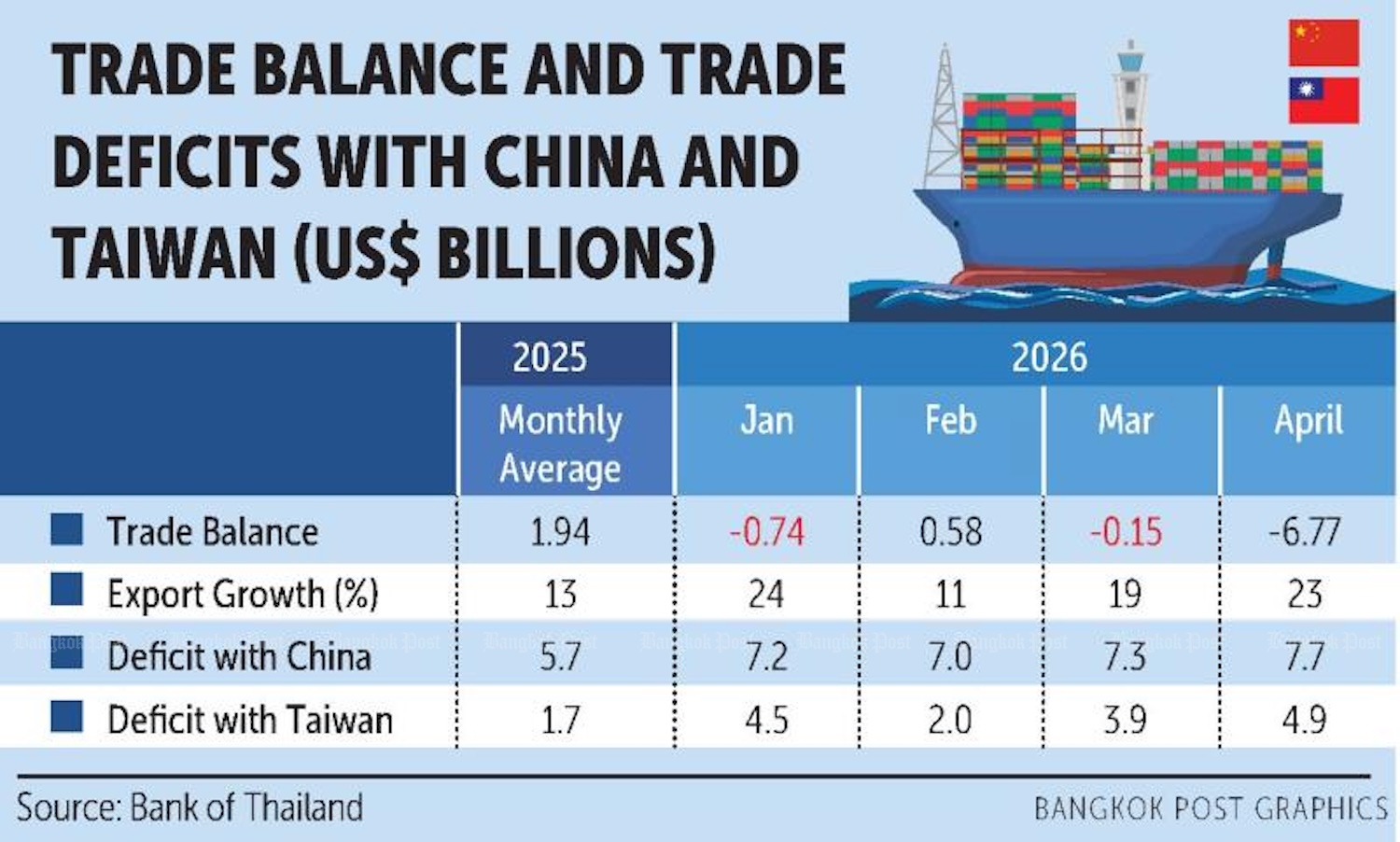

The trade deficit in April 2026 was $6.8 billion, the worst in 20 years. An observant economist such as myself would immediately question the figure. How could an oil price of $101 per barrel — roughly the same level as in April 2022 — have caused a historic trade deficit, particularly when the trade balance in the same month in 2022 showed a surplus of $386 million?

My suspicions led me to investigate the matter. I had previously estimated that rising oil prices of around $100 per barrel would lead to a trade deficit of $1–2 billion per month. There must therefore be other factors hidden within the $6.8-billion deficit figure.

After a careful examination of the sources of the deficit, I found 41% was driven by higher fuel import costs, 28% by increased imports from China, and 26% by higher imports from Taiwan. The first factor — rising oil prices — may be transitory, as the BoT has suggested. However, the other two factors are likely to be more structural. The evidence is presented in the attached table below.

Before explaining the essence of the table, has any reader noticed the significant drop in export growth in February? Can anyone guess the reason? The answer is Chinese New Year. When Chinese populations, both in mainland China and Taiwan, are on holiday, the Thai economy effectively slows as well, as though it is an extension of theirs. There was no comparable drop in export activity in April, as China does not observe Songkran holidays.

The unflattering implication is that Thailand has little control over its export sector and, by extension, its economic destiny. It may therefore be prudent to introduce Chinese language courses as a mandatory part of the school curriculum.

Incidentally, readers searching for trade balance data online — particularly on Trading Economics — will find that Thailand’s April 2026 trade deficit was reported at $10.2 billion (even more concerning). This is not incorrect, as the data is drawn from the Ministry of Commerce, which uses a different accounting method.

The $6.8-billion figure is based on the Bank of Thailand’s methodology, which follows IMF guidelines. The BoT does not include shipping and insurance costs in import figures under the trade account, instead recording them under the services account.

Returning to the essence of the table, it highlights two alarming issues. The BoT and the government may not be alarmed, but as a Thai citizen, I am.

The first is “transfer pricing” involving Taiwan, as shown in the final row of the table. It is notable that Taiwan, a much smaller economy than China, records a trade imbalance with Thailand second only to China. Moreover, the shift from an average monthly deficit of $1.7 billion a year ago to $4.9 billion in April 2026 is striking.

This unusually large deficit with Taiwan would not occur without transfer pricing practices. Taiwanese firms may sell intermediate goods for assembly in Thailand at prices higher than the export price of the finished products shipped onward to end markets.

For example, integrated circuits from Taiwan may be exported to Thailand for assembly at $100 per set. After assembly in Thailand, the finished product — which should, in theory, be exported at $110 to reflect a $10 assembly cost — is instead exported to the United States at $80, because US customers will not pay more. In this case, Thailand pays Taiwan $100 for intermediate goods but receives only $80 from the US for the finished product.

The incentive behind such practices is to boost the profitability of the parent company in Taiwan, thereby potentially supporting its stock valuation. This is not a new phenomenon. According to a study by the Thailand Development Research Institute (TDRI), similar transfer pricing practices have been observed in durian exports. Chinese intermediaries reportedly purchase durians from Thai farmers at 100 baht per kilogramme and then export them to parent companies in China at 60 baht per kilogramme.

I am not concerned with stock price manipulation. The real question for Thailand is: what benefits does it derive from exporting other countries’ products? The table shows that the more Thailand exports, the larger the trade deficit becomes. The best month for the trade balance is February, when exports are at their lowest.

The second alarming issue highlighted by the table is the “China shock”. Owing to excess supply in China, Chinese producers are dumping goods into global markets, including Thailand. Compared with the average monthly deficit in 2025, Thailand’s trade deficit with China in 2026 has increased by 35%. One only has to consider the local industries being displaced by cheap Chinese imports.

Thailand should stop deceiving itself with export-growth illusions. The top-line export figures are meaningless; the bottom line of the trade deficit is what truly matters.

As for the familiar argument that trade deficits arise from imports of new machinery, I would simply note that these are “their” machines, designed specifically to produce “their” products, which may later become obsolete.

A simple comparison of the size of the trade deficit against increases in GDP investment would suggest that this argument is not particularly convincing.